17 Dec 2020 | 22:06 UTC — Denver

US working natural gas volumes in underground storage declines 122 Bcf: EIA

By Brandon Evans and Kent Berthoud

Highlights

Survey expected 127 Bcf withdrawal

Henry Hub futures dip despite large pull

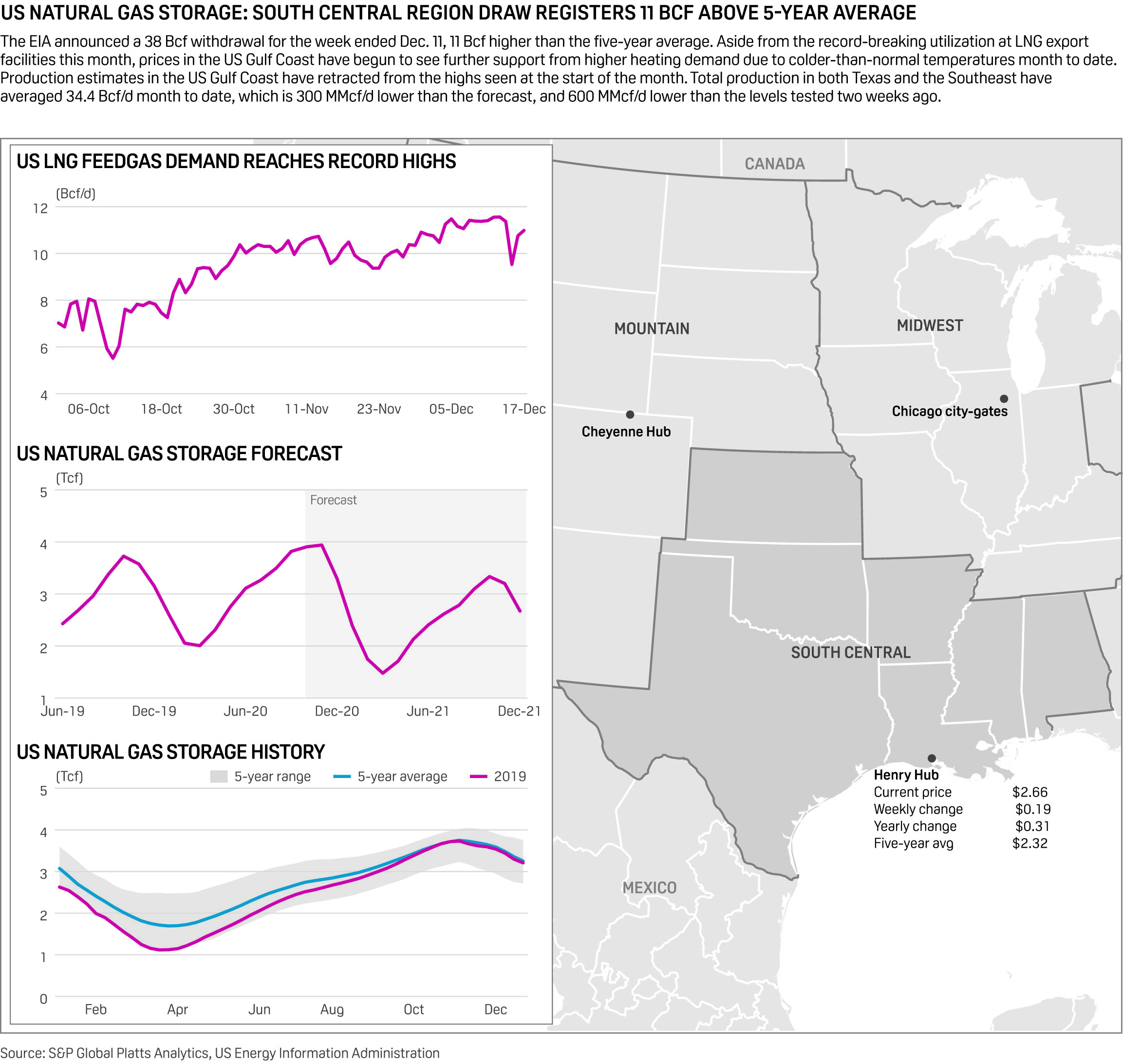

Denver — US working natural gas in storage posted its first triple-digit build of the heating season last week as South Central accounted for the largest regional draw on cooler weather and record-high LNG feedgas demand.

Storage inventories decreased by 122 Bcf to 3.726 Tcf for the week ended Dec. 11, the US Energy Information Administration reported Dec. 17.

The withdrawal was weaker than an S&P Global Platts survey of analysts calling for a 127 Bcf pull. Responses to the survey ranged from a 103 to 145 Bcf withdrawal. However, the pull was stronger than the 97 Bcf draw reported during the same week last year as well as the five-year average withdrawal of 105 Bcf, according to EIA data.

The draw was also stronger than the 91 Bcf withdrawal reported the week prior.

Residential and commercial demand grew by 3.5 Bcf/d week on week and power demand gained 1.6 Bcf/d, according to S&P Global Platts Analytics. Incremental power demand was also spurred by falling wind generation, which declined by nearly 15 GWs, the equivalent of 2.5 Bcf/d in gas-fired generation. Total supply was up a marginal 100 MMcf/d week on week as lower US production was offset by a 700 MMcf/d increase in net Canadian imports.

Storage volumes now stand 284 Bcf, or 8.3%, more than the year-ago level of 3.442 Tcf and 243 Bcf, or 7%, more than the five-year average of 3.483 Tcf.

The NYMEX Henry Hub January contract slipped 3 cents to $2.64/MMBtu in trading following the release of the weekly storage report at 10:30 am ET. The remaining winter strip, February and March, also dipped 3 cents to average $2.63/MMBtu, a decline of 5 cents from the week prior.

Entering the Dec. 17 EIA report, the prompt-month January NYMEX contract has been in a well-defined range this week – oscillating between $2.60 and $2.70/MMBtu. The relatively narrow range appears to be linked to weather model uncertainty entering January with some models pointing to a colder regime, while others predict a milder background state, according to S&P Global Platts Analytics.

So far this withdrawal season, inventory has declined by a net total of 229 Bcf. Over the past five years, stocks have decreased by an average of 497 Bcf by this time of the heating season.

Platts Analytics supply and demand model currently forecasts a 166 Bcf withdrawal for the week ending Dec. 18, which would shrink the surplus versus the five-year average by an additional 39 Bcf as cooler temperatures spike US-level demand week over week.

Colder temperatures have boosted residential and commercial demand by nearly 5 Bcf/d week on week. Colder temperatures also boosted power and industrial demand by 500 MMcf/d and 900 MMcf/d, respectively. Total supply could not keep pace with demand, with supply falling by about 400 MMcf/d – led by a 200 MMcf/d decline in US production.