25 Feb 2020 | 22:50 UTC — New York

Factbox: Energy prices retreat as coronavirus outbreak accelerates beyond China

Commodity prices moved sharply lower this week amid a renewed focus on demand destruction following a flurry of new coronavirus outside of China.

ICE front-month Brent futures settled at $54.95/b Tuesday, down $4.36 over the past three trading days, and down $10.25/b since January 20, when commodities markets began to react to the virus.

S&P Global Platts Analytics has adjusted its 2020 global oil demand growth outlook down to 860,000 b/d, marking the weakest since 2011. Asian refined products demand is expected to grow by 380,000 b/d in 2020, "posting its weakest growth since the global financial crisis in 2009," according to Platts Analytics.

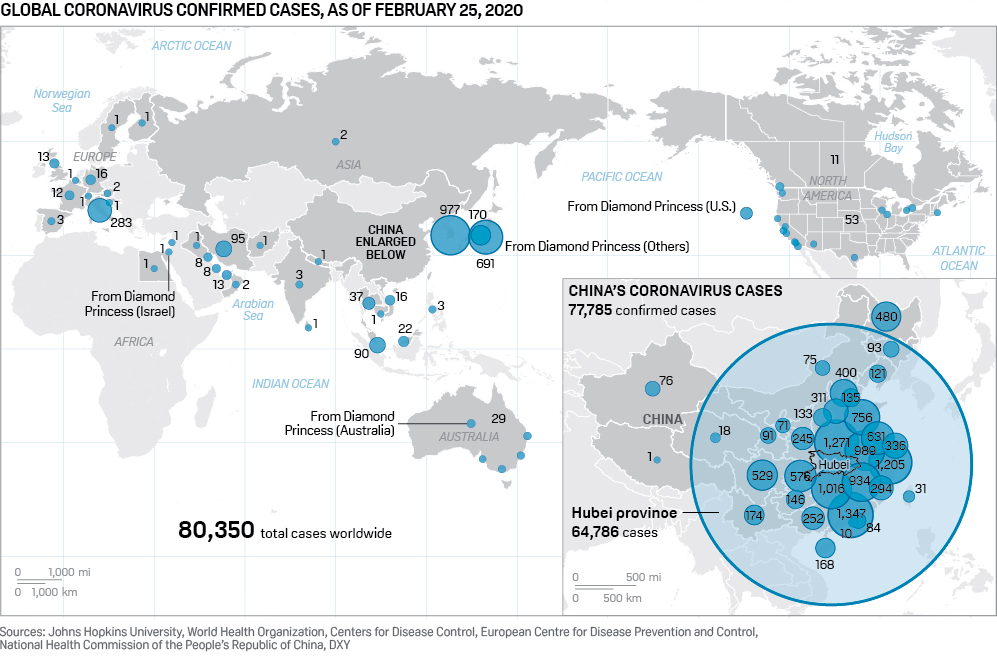

Globally, 80,238 cases of Covid-19 coronavirus have been confirmed in 34 countries as of Tuesday morning, according to World Health Organization data.

Mainland China accounts for just under 97% of confirmed cases worldwide, but South Korea and Italy have emerged as major growth centers for new cases this week.

Recent statistics on the number of coronavirus cases have had two separate narratives: cases in China are no longer growing rapidly; but there are new cases in discrete geographical areas, hinting that global efforts to contain the disease may have problems.

Authorities in northern Italy have ordered the closure of schools, bars and other public spaces until March 1, following a flurry of new confirmed coronavirus cases.

Traffic activity in China remains a critical key to normalizing business operations in China; recent developments are encouraging on these fronts, but in these trends it will likely take until end of March for complete normalization

Airlines have canceled flights, reducing jet fuel demand.

IP Week is going ahead in London this week but a number of oil industry events, evening receptions in particular, have canceled.

OPEC and its allies will meet in Vienna on March 5-6, formally abandoning plans to hold an earlier summit to confront the coronavirus' impact on oil markets.

Click here for full-size image

{kind=link}

PRICES

Oil

**The recent sell off in crude prices has weakened the backwardation in the Brent forward curve. Year-ahead Brent futures settled at a 72 cents/b discount to the front month Tuesday, in from $1.75/b Friday.

**The one-year NYMEX WTI structure has also collapsed, falling to an 11 cents/b backwardation Tuesday from $1.07/b Friday.

**The Singapore jet crack spread against Brent ended Tuesday at $6.67/b, down from $11.34/b January 20.

**The Rotterdam jet fuel crack against Brent ended Tuesday at $9.00/b, down from $14.17/b January 20.

**The New York jet crack ended Tuesday at $9.679/b, down from $14.19/b January 20.

LNG

**The Platts JKM, the LNG price benchmark for the Northeast Asia region, edged up 1 cent to $2.904/MMBtu Tuesday, but was down 31% from January 20.

**The Platts FOB Gulf Coast LNG price slid 1 point to $2.159/MMBtu on Tuesday, down 52 cents from January 20.

Shipping

**The West Africa to East route for VLCCs was assessed at $17.11/mt Tuesday, down $10.81 since January 21.

**The Arab Gulf to China VLCC route was assessed Tuesday at $9.67/mt, down $10.33 since January 20.

Metals

**The front-month rebar futures contract on the Shanghai Futures Exchange closed at Yuan 3,473/mt Tuesday, down 6.1% from January 20.

**Platts assessed the 62% Fe Iron Ore Index at $90.10/dry mt CFR North China Tuesday, up $7.4 from its February 3 nadir, but still down 5.8% from January 20.

**The London Metal Exchange three-month copper price ended Wednesday at $5,686.00/mt, up $6 on the day but down more than 9% from January 20. Copper is often seen as a barometer for global economic health.

TRADE FLOWS

Oil

**S&P Global Platts Analytics has adjusted its 2020 global oil demand growth outlook down to 860,000 b/d, marking the weakest since 2011. Asian refined products demand is expected to grow by 380,000 b/d in 2020, its weakest since 2009.

**Key international airlines have suspended or reduced flights due to the virus, reducing jet fuel demand.

**While Sentinel Midstream's Texas GulfLink deepwater crude export terminal project remains on schedule, the spread of the virus comes just as the company is trying to nail down contracted shippers and buyers, especially in Asian markets. "The coronavirus is a big gut punch right now," the company's CEO said Tuesday. "It's put talks on hold."

**The Port of Corpus Christi expects February crude exports to slip from January's record-high 1.38 million b/d due to ripple effects from coronavirus.

**Demand for Chinese mainstays such as Russian ESPO Blend crude and medium sour Oman is expected to take a hit this month, with trade and economic activity declining.

**Run rates at China's state-owned oil giants - Sinopec, PetroChina, CNOOC and Sinochem - fell to a record low 67% of nameplate capacity in February, from 85% in January: S&P Global Platts' survey. Run rates for independent refineries in Shandong plunged to 35-36% from 63.5% in January, with 15 refineries idle in February.

**With Asia's crude buying curtailed while the region tackles the outbreak, more oil from West Africa is being offered in Europe, pushing the Mediterranean's light sweet prices down from their recent highs.

**The provincial government in Hubei, the epicenter of the coronavirus outbreak, has asked companies not to resume work until March 11 instead of February 21.

**OPEC confirmed it will meet in Vienna March 5-6. A technical committee February 7 recommended deepening the OPEC+ 1.7 million b/d production cut accord by 600,000 b/d through the end of Q2. Russia has yet to endorse the plan.

LNG

**The impact of China's coronavirus outbreak on LNG market is expected to worsen in coming weeks as economic activity in key manufacturing hubs struggles to rebound, keeping a lid on natural gas demand and triggering more LNG trade flow disruptions.

**China's state-owned CNOOC has declared force majeure on LNG contracts.

**CNOOC remains most affected due to the suspension of many factories and transport restrictions, and many domestic LNG terminals were running with high inventories.

**China's National Development and Reform Commission said it will reduce domestic natural gas prices to help companies restart operations, potentially reducing profit margins for gas importers and further slowing their LNG imports.

**Shell expects Chinese LNG demand to remain lower than expected into March. LNG cargoes that cannot be absorbed in China would be deferred for delivery at a later date, while current cargoes on the water are being diverted "to find a safe home where they are needed," Maarten Wetselaar, Shell's Integrated Gas and New Energies Director, said.

**Indian LNG importers, capitalizing on these diverted cargoes and lower LNG spot prices, have tendered for and procured almost 67 cargoes, amounting to about 4.3 million mt, to be delivered during the year, Platts data showed.

**Several US developers have delayed final investment decisions, with one warning it was running out of cash to continue normal operations.

**Houston-based Cheniere Energy, which has a supply contract with PetroChina, said difficulty in securing new long-term supply purchase agreements could pose headwinds to advancing its Texas liquefaction project by June. Two LNG cargoes for April loading from Cheniere's terminals were recently canceled by customers.

Shipping

**Contango in crude forward curves is incentivizing the use of VLCCs as floating storage. Floating crude storage in the anchorages around Malaysia and Singapore rose steadily from 5.133 million barrels on January 21, to 17.636 million barrels on February 3, a more than threefold increase in less than two weeks, Kpler's data showed.

**The Shanghai delivered marine fuel 0.5%S price declined $40/mt week on week to be assessed at a six-month low of $495/mt Monday.

**With the coronavirus outbreak coinciding with the Lunar Year holidays, a lack of demand from China has been putting pressure on tonnage requirements out of the West African region. China is a major buyer of WAF crudes.

**Delays in loading and delivery of cargoes in the tanker, dry bulk and container shipping segments are being reported due to ships being forced to sit idle amid a lack of crew availability.

**From Fujairah in the Middle East to the Asian bunkering hub of Singapore, traders are reporting sharp declines in fuel demand as shipowners brace for a potentially extended slowdown in global seaborne trade.

Metals

**Chinese steel production has slowed since early February due to weak demand and logistics constraints in receiving raw materials and delivering finished products amid the outbreak.

**Daily crude steel output by China Iron & Steel Association members fell 2.7% to 1.939 million mt/day over February 1-10 from 1.993 million mt/day in late January, latest CISA data showed.

**As of February 21, 73 blast furnaces operated by Chinese mills have been suspended, causing a daily pig iron loss of 21,000 mt, CISA data showed.

**S&P Global Platts estimates a reduction of at least 29 million mt in Chinese finished steel consumption in February, down 75% year on year and equating to pig iron consumption of 26 million mt. Finished steel consumption in March is estimated to fall by at least 22 million mt year on year, equating to 19 million mt of pig iron consumption, down 30% year on year.

**China's finished steel inventories at mills and spot markets are likely to reach 40 million mt by the end of February, up 24 million mt from the end of December 2019, Platts analysis showed.

**Turkish steel exporters have received increased demand from some Asian and African markets in the last 15 days, as these countries directed some of their steel orders to Turkey instead of China.

**A total of 12 silicon producers -- five in Sichuan, three in Xinjiang, one in Yunnan, one in Guizhou and two in Heilongjiang -- are operating below capacity, China Nonferrous Metals Industry Association data showed. In Sichuan, the current run rate is just 10% with 12 furnaces running, compared with 32% in January.