21 Feb 2020 | 21:58 UTC — New York

Oil retreats as coronavirus spread renews demand concerns

By Chris van Moessner and Herman Wang

Highlights

Coronavirus spread beyond China spooks markets

US manufacturing PMI sinks to 6-month low 50.8 in February

Saudi Arabia dismisses rumors of OPEC+ strife

The oil complex settled lower Friday, snapping eight consecutive up days, amid a renewed focus on demand destruction concerns after the further spread of the coronavirus outside of China.

ICE April Brent settled down 81 cents at $58.50/b and NYMEX April WTI finished 50 cents lower at $53.38/b.

Oil prices moved lower overnight amid reports of a sharp uptick in the number of coronavirus cases outside of China. In South Korea, the number of confirmed cases doubled to 204 in just 24 hours, according to media reports.

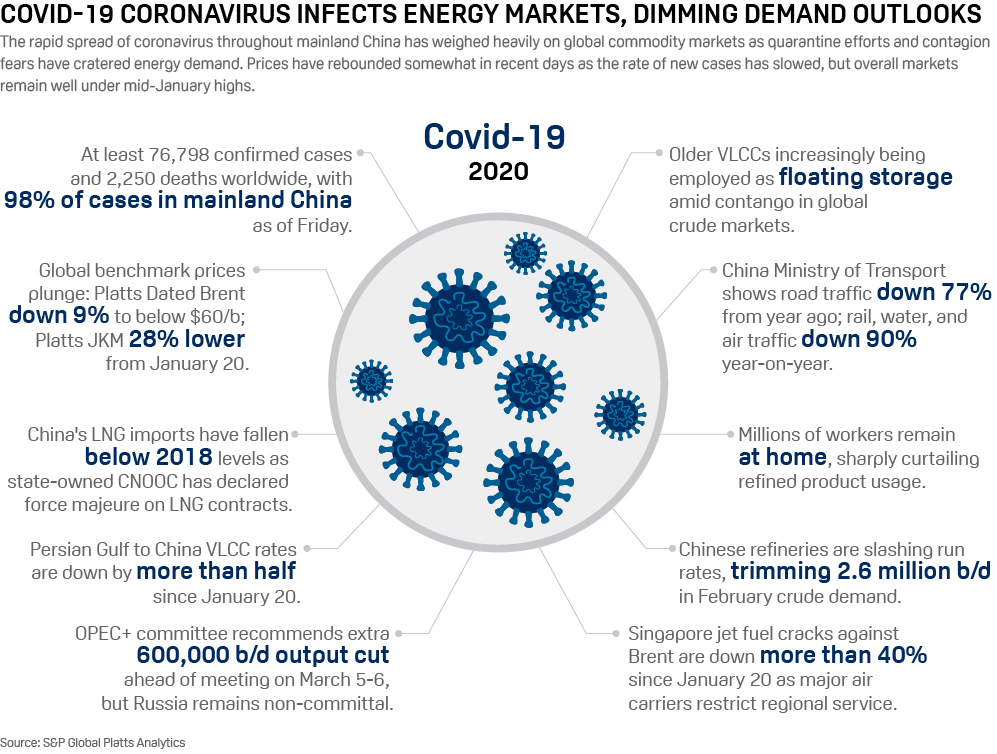

As of Friday there were 76,798 confirmed cases of the virus resulting in at least 2,250 deaths worldwide, according to data from the Johns Hopkins University. Mainland China accounts for around 98% of all cases, down from 99% earlier this week.

"For so long, investors have been resilient to the ugly numbers coming out on Wuhan, in relation to the number of cases and deaths from the coronavirus," OANDA senior market analyst Craig Erlam said in a note. "The spike in South Korea, including another fatality, rattled investors in the region overnight and that appears to have spread across Europe and now the US."

Click here for full-size graphic

{kind=link}

Swiss investment bank UBS said Friday Chinese oil demand will likely average 12.1 million b/d during the first quarter, a 1.3 million b/d, or 10%, downward revision to its previous estimate (See story 1531 GMT).

"COVID-19 [coronavirus disease] has added a new negative dimension to oil markets," UBS analyst Jon Rigby said in a note. "It is early days but at the very least Q1 oil demand will see a dramatic fall in China as economic activity grinds to a halt, and likely spill-over effects onto global activity."

UBS cut its 2020 global oil demand forecast by 450,000 b/d, or 0.4%, to largely reflect China's widespread travel bans to contain the virus.

The backwardation in year-ahead Brent futures eased Friday, narrowing to $1.75/b from $1.98/b on Thursday. But the WTI structure was more bullish, with backwardation emerging in the front-to-sixth month spread for the first time since January 30.

Weak US economic data added to downside price pressure, especially on product futures. The IHS Markit manufacturing PMI for February fell to 50.8 from 51.9 in January, while the services PMI dropped to 49.4 from 53.4 the month prior. A PMI index below 50 indicates a contraction in the sector.

NYMEX March ULSD settled down 1.10 cents at $1.6866/gal and March RBOB was 1.91 cents lower on the day at $1.6506/gal.

SAUDI ARABIA DISMISSES RUMORS OF OPEC+ STRIFE

Saudi Arabia remains committed to the OPEC+ alliance with Russia and other key oil producers, the kingdom's energy minister said Friday, rejecting a report that it was considering a pause in its cooperation with the group.

"We are in continuous communication and dialogue with all our OPEC and OPEC+ partners," Prince Abdulaziz bin Salman told S&P Global Platts.

The Wall Street Journal reported earlier Friday that Saudi Arabia could take a break from the OPEC+ alliance, given Russia's reluctance to commit to deeper production cuts to combat the coronavirus outbreak's impact on global oil demand.