03 Oct 2019 | 14:29 UTC — Insight Blog

China waste policy could make or break the global ferrous scrap market

By Samuel Chin

China’s recent battle against waste imports into the country has proved a success, as August ferrous scrap imports fell to zero, a figure unseen for the past 20 years in the country, according to the latest customs figures.

Since late December 2018, China has been slowly isolating itself from the global scrap market. The restrictions on ferrous scrap imports are part of a pushback against the country’s prior, unwanted, role as a dumping ground for global waste.

But regional industry participants, including those in China, feel that ferrous scrap has been unfairly caught up in Beijing’s drive for a cleaner environment.

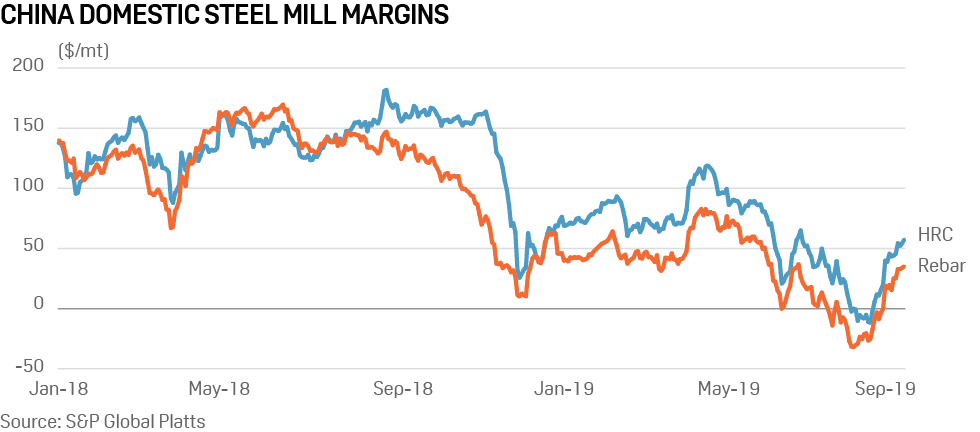

The restrictions have contributed to higher domestic scrap prices for its steel makers. At the same time, Chinese steel prices have been weakening, pushing mill margins down.

These difficult conditions for the Chinese steel sector have led at least one participant to appeal to the government for a change in regulation, in the hope that easing controls on imported scrap could reduce the pressure on margins.

China’s rising scrap demand

China’s consumption of ferrous scrap remained unmatched globally in the first half of 2019, hitting 101 million mt, up 13.4 million mt, or 15.3% from the same period in 2018. Last year’s consumption reached a staggering 188 million mt, according to figures from the China Association of Metal scrap Utilization (CAMU). This was six times that of Turkey, at 30 million mt in 2018, which holds the top spot among importers of scrap.

China’s scrap generation has been keeping up with its large appetite. In H1 2019, 116 million mt of scrap generated, up 13 million mt or 13% on the year.

Though isolated from the global scrap market though the recent restrictions, China remains a “sleeping dragon” that could potentially heavily alter the global balance if its policy changes. A brief rush of illegal exports of Chinese scrap in early 2017 had seaborne prices plummeting by 17% in East Asia – showing the impact of any sudden change in flows to and from the country.

The current year-long slump in the global scrap market saw prices hit two-year lows during September, with sentiment remaining dampened by depressed steel demand.

The Platts Turkish scrap index has fallen 38% since its 2018 peak in March. In East Asia, bulk scrap prices to the region marked a 36% fall in the same period, with a similar contraction of 34% seen for the containerized market.

Go deeper: Ferrous scrap plays catch up after steel’s dramatic tumble

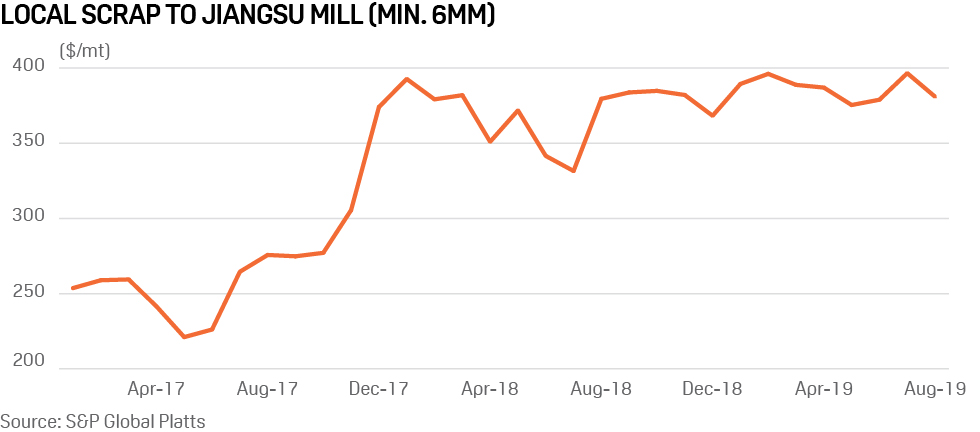

But while global scrap prices remain bearish, Chinese domestic prices have stayed high. Monthly prices for thick scrap, minimum width 6mm and delivered to Jiangsu steel mills, averaged at $387/mt this year to end-August, including 13% value added tax. Surprisingly, this was up by $16/mt from the 2018 years average, despite a drop in VAT from 16% to 13% that came into effect in April 2019. The thick scrap price closed at $378/mt on Sep 25, according to Platts data.

In comparison, Heavy Scrap (HS) material in Japan is currently at Yen 29,160/mt ($272/mt) delivered to mill, including 8% consumption tax, as of September 25. This was down by $138/mt year on year, based on Platts price data.

Factoring out the respective local government taxes, this would mark a disparity of $106/mt for thick scrap, not factoring in freight to China, and the trucking and port charges within the country, as of September 25.

“The difference is huge, it would be a great (arbitrage) opportunity if we can supply to China. We need more buyers at a time when the Japanese domestic demand is falling,” a Japanese trader commented.

“But we need to be aware of the waste regulations that the Chinese government has in place, we are not too familiar with it as most have taken their eyes off this market.”

Sky-high scrap prices

So what lies behind the continued strength of demand for scrap within China? Due to environmental protection policies, Chinese steelmakers have become more restricted in the coking, sintering and blast furnace production processes required to produce steel from iron ore. This has fuelled an insatiable hunger for scrap from China’s blast oxygen furnace (BOF) operators.

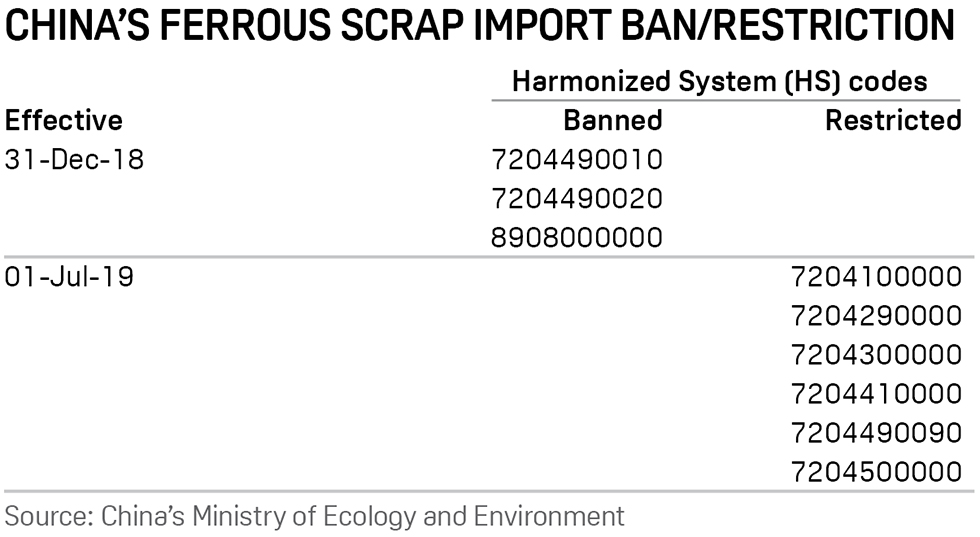

The restrictions on scrap imports came in two tranches, in December 2018 and July 2019, banning or restricting different grades of product (see table).

This capped Chinese steelmakers’ ability to import scrap, subjecting them to an enclosed market, and supported prices. Meanwhile, the nation’s steel makers have seen margins dipping to bare figures and EAF mills have been struggling to survive as raw material prices remain expensive.

“The government’s restriction on importing quality raw material like scrap is not entirely right. This is a raw material that is environmentally friendlier (as compared with the Iron ore steelmaking route), and if proper controls are set, it can really benefit the steel industry here,” a Chinese blast furnace mill source told Platts.

“Domestic prices are just too far (high) from the international market now.”

Although in theory Chinese mills should be able to obtain environmental licenses for scrap importation, this has proved difficult, and hinders their ability to enter the international spot market, a major Chinese mill told Platts.

“We need to get this license, and it is quite complicated to get an approval for it,” the source said. “To date we do not have it at all.”

Regional market sources told Platts that the removal of such restrictions could lend support to falling global scrap prices by boosting demand, while helping to naturally balance down the high Chinese domestic scrap prices.

This would in turn improve the low steel making margins in the country, and allow more room for the Chinese EAFs to grow, the sources said.

Since the July 1 restrictions, only three batches of approvals have been granted by the Ministry of Ecology and Environment for ferrous scrap imports. These amounted to just 20,918 mt of scrap allowed into the country within the restriction list.

The domestic industry has now taken its first step towards addressing the problem. A major Chinese steelmaker has told Platts that they have already written to the relevant government authorities asking them to improve the situation, and allow clean scrap imports into the country for the benefit of the steel industry.