Fertilizers, Chemicals, Energy Transition, Agriculture, Renewables, Rice

March 20, 2026

Asia's fertilizer disconnect: Crop prices lag surging costs

By Hui Min Lee and Elizabeth Thang

Editor:

HIGHLIGHTS

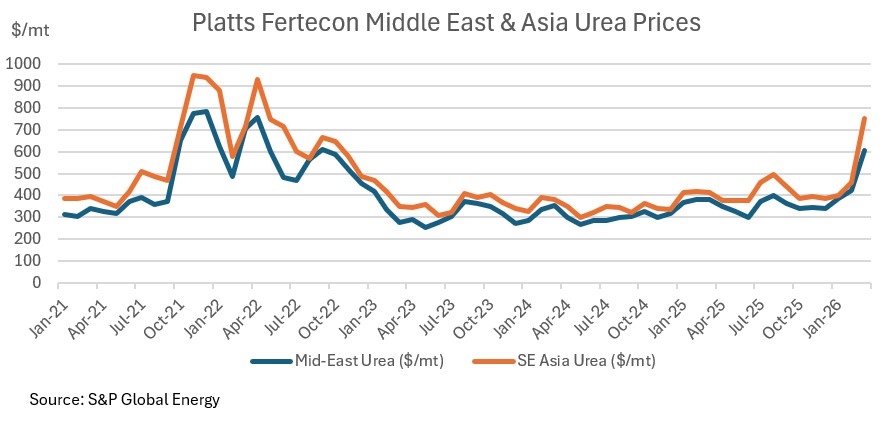

Asia fertilizer prices surge but still below 2022 highs

Asian crop prices lag behind input cost jump

Government subsidies shield farmers temporarily

The ongoing conflict in the Middle East has driven fertilizer prices sharply higher across Asia since late February, but the surge in input costs has yet to translate into corresponding gains for key crop prices, creating a delayed risk to farmer profitability and planting decisions for the coming season.

The disconnect between soaring fertilizer values and subdued crop markets reflects a lag effect that could tighten exportable surpluses and eventually push food prices higher, as farmers absorb higher costs or reduce plantings, said analysts.

Since late February, disruptions to the Strait of Hormuz have sent nitrogen and phosphate prices soaring. Nitrogen fertilizer prices, in particular, have surged globally. Platts assessed FOB Middle East granular urea at $604-$710/mt on March 19, a sharp jump from $436-$494/mt on Feb. 26 before the conflict began. The Southeast Asia granular urea price was $750/mt FOB on March 19, up from $490-$498/mt pre-conflict. While still under upward pressure, it is below the highs of 2022, and this increase puts prices firmly above levels seen since 2023.

This price shock is a direct result of severe logistical disruptions that are tightening supply-demand balances and putting clear upward pressure on prices for key products like ammonia, urea, and ammoniated phosphates. Crucially, this also affects raw materials in these value chains, namely natural gas and sulphur.

Compounding this, China—an important urea and phosphate producer for the region—remains largely absent from export markets due to strict quota controls, effectively removing a key relief valve for the strained global market.

Amid the disruptions, offers for key fertilizers have become scarce, with available cargoes commanding steep premiums. While bids have risen to chase the limited supply, a sense of caution is emerging, and some buyers are choosing to delay procurement in the hope that prices will stabilize.

Crop prices lag behind soaring inputs

Despite the input cost inflation, the effect on crop markets has been uneven.

This is most evident in the rice sector, where Platts spot price assessments have declined steadily since September 2025 due to a global supply glut. The Long Grain White Rice 5% Broken FOB India price assessment averaged $343.95/mt in February 2026, down almost $54/mt (13.5%) from a year ago, based on Platts data and was assessed at almost $11/mt lower at $333/mt on March 19.

On a delivered basis, Platts' Long Grain Parboiled 5% STX CFR West Africa has gained only $20/mt to $408/mt since Feb. 19, a rise attributed mainly to higher freight costs.

In the wheat market, Thailand buyers have seen delivered prices of feed wheat rise 5%-13% ($15-$34/mt) since Feb. 28, based on Platts tender data. But, more striking is the tenor of those purchases: cargoes for shipment as far as February 2027, which multiple sources described as uncommon for such advanced buying.

However, for Australia, the region's key milling wheat exporter, the FOB Australia APW price assessment has gained just $4/mt since Feb. 27 to $263/mt on March 18, reflecting subdued demand.

"For Australia, the near-term wheat outlook remains relatively insulated given pre-purchased inputs," said Zinkovski Vladimir, Head of Crops at S&P Global Energy CERA. He cautions, however, that "sustained fertilizer and energy inflation—combined with rising El Niño risk—could curb yields and tighten exportable surpluses, while the current higher flat price environment may also trigger demand destruction."

Delayed impact

Fertilizer price shocks don't translate instantly into crop markets because of timing mismatches built into agricultural cycles.

This means the price shock will be most acutely felt by those now procuring inputs for upcoming plantings, where higher fertilizer prices could translate into lower yields and, eventually, higher crop prices.

In India, fertilizer availability appears comfortable, and supportive policies like the Minimum Support Price and urea subsidies reinforce farmer incentives to maintain plantings for the kharif season. "Given this, major reductions in kharif rice acreage seem unlikely," said Dipanshi Agarwal, principal analyst for APAC Crops at CERA.

However, this protection has a potential downside. Indian farmers have continued to purchase urea at a fixed price, shielding them from global shocks, but yield losses could be a risk if farmers rely solely on nitrogen fertilizer.

"India's reliance on imported diammonium phosphate, Muriate of Potash, and complex fertilizers remains a structural vulnerability," Agarwal said. "Any rise in global prices or supply disruptions could push farmers toward subsidized urea, worsening nutrient imbalance and risking yield losses."

Alberto Persona, director of Fertilizer Analytics and Sustainability at S&P Global Energy, adds that subsidy and farm support schemes were expanded significantly in many countries during recent global shocks, including the COVID-19 pandemic and the Russia-Ukraine war.

While these policies help, the pressure will eventually find an outlet. "Prolonged high prices inevitably end up being transferred on to consumers further down the value chain," says Persona, though he adds that "higher prices today do not necessarily imply a proportional increase in overall farm costs as farmers can adapt their application rates."

"Overall, the situation remains concerning, but it is also important not to overstate the magnitude, immediacy, and duration of the impact on everyone's livelihood – despite what some might say," Persona said.