Electric Power, Energy Transition, Nuclear, Renewables

March 30, 2026

North America’s PPA market: Beyond volumes

By Bruno Brunetti and Francisco Sequera

Editor:

Three major themes are driving today's US power purchase agreement (PPA) market: demand growth, market complexity and policy uncertainty.

Rapid load expansion from artificial intelligence (AI) and hyperscalers is pushing multigigawatt procurement into a grid that was not built for speed. At the same time, congestion and curtailment are changing renewable capture rates, while interconnection queues are ballooning and being reformed, adding more timeline uncertainty.

As developers and buyers navigate a more complex market, policy and execution environment, North American PPA activity accelerated in early 2026, after a slow finish to 2025.

An analysis by S&P Global Energy Horizons shows PPA activity totaled about 36 GW in 2025, down from around 60 GW in 2024, when deal flow was supported by improved project economics under the Inflation Reduction Act (IRA) as the AI rush had just started.

Horizons analysts characterize 2025 less as a demand collapse and more as a recalibration period, reflecting higher development costs, supply chain constraints and increased uncertainty around the ability of some projects to monetize the full value of IRA tax credits.

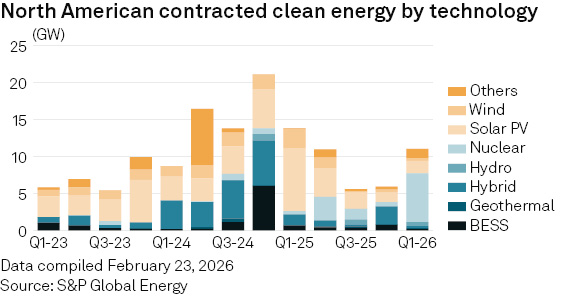

From the start of 2026 through February 23, roughly 11 GW of clean energy PPAs had been announced, according to Horizons, signaling a rebound in contracting pace just as market participants work against a July construction-start window that is acting as a near-term catalyst for dealmaking.

What changed is not the direction of demand, but the terms under which demand clears: greater scrutiny of tax-credit bankability, wider pricing dispersion tied to capacity factors and curtailment assumptions, and more attention on the shapes or timing of the power delivered, which is elevating the strategic importance of firm- and hybrid-based resources.

Hyperscalers shape the market

Corporate buyers--especially the "Big Four" hyperscalers: Meta, Google, Amazon and Microsoft--continue to drive the majority of PPA activity. They accounted for 76% of volumes in Q4 2025, and that share rose to 90% in early 2026.

Data centers have become the single most important source of PPA demand, and their influence continues to grow. According to S&P Global Energy analysts, data centers consumed roughly 270 TWh of electricity and procured about 180 TWh of clean energy through PPAs in 2025.

US data center loads may reach about 765 TWh by 2030, the analysts project.

Sustainability remains a top priority: over half of data center operators surveyed by Horizons' 451 Research say it directly influences their vendor selection. Even so, grid connection availability constraints are increasingly forcing developers to consider alternative strategies, with an increasing number of behind-the-meter gas projects – an option that was almost unthinkable a while ago.

More complex policy environment

The policy environment is playing an increasingly central role in PPA execution.

New US Treasury and Internal Revenue Service guidance issued Feb. 12 clarified some of the detailed compliance expectations around Foreign Entities of Concern and "material assistance" demanding deeper cost tracing, more extensive documentation and new supplier certifications.

More regulation is expected. As a result, tax credit eligibility and the bankability of those credits remain a top concern for both developers and financiers.The complexity has not stopped deals from being signed, but it has hindered a stronger contracting rebound.

Nuclear, hybrid PPAs take center stage

It is increasingly becoming a "multitechnology" market, according to Horizons analysis, with meaningful commitments to nuclear and hybrid structures alongside solar photovoltaics' (PV) continued dominance.

The motivation is clear: hyperscalers are increasingly prioritizing scale and firm, 24/7 zero-carbon resources over purely variable renewable generation.

In 2025, data centers procured nearly 6 GW of nuclear capacity. In January 2026, Meta alone announced 6.6 GW of nuclear PPAs with TerraPower, Vistra and Oklo.

Hybrid PPAs--especially solar-plus-storage--also rebounded, with 2.4 GW contracted in Q4 2025, a ninefold increase from Q3, according to the S&P Global Energy PPA database. While still below the 2024 highs, the upswing signals growing comfort with more complex structures that can mitigate intermittency and price volatility.

Battery energy storage systems (BESS) show a mixed picture. While standalone BESS contracts remain limited, installed capacity is growing, with 18 GW expected in 2026, rising to 21.5 GW by 2028, according to the S&P Global Energy analytics dashboard for clean energy technology.

Many storage projects are advancing without longterm PPAs, instead relying on merchant opportunities, ancillary services and state incentives.

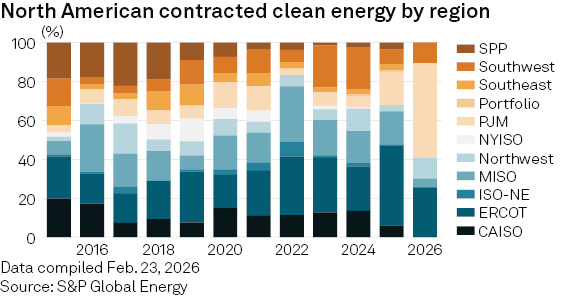

Regional trends: ERCOT, PJM dominate

As for the regional trends, the Electric Reliability Council of Texas (ERCOT) remains central to PPA activity, benefiting from comparatively faster development timelines and a large pipeline of solar and hybrid projects. Texas remains the US solar powerhouse, adding about 7.4 GW of utility scale solar in 2025, with total capacity additions expected to exceed 9 GW in 2026. At the same time, congestion risk and cannibalization are becoming more pronounced, sharpening location specific differentiation. PJM Interconnection has been gaining strategic attention as data center demand accelerates, with the recent nuclear deals signed this year propelling the region to the top of the national leaderboard by contracted volume early this year, but interconnection constraints for clean energy projects are increasingly binding.

The Midcontinent Independent System Operator (MISO) has seen renewed interest, while California Independent System Operator activity has been more muted over the past year. CAISO has seen contracting fall sharply to about 2 GW in 2025, down from over 6 GW the prior year, weighed down by interconnection delays, curtailment concerns and rising development costs.

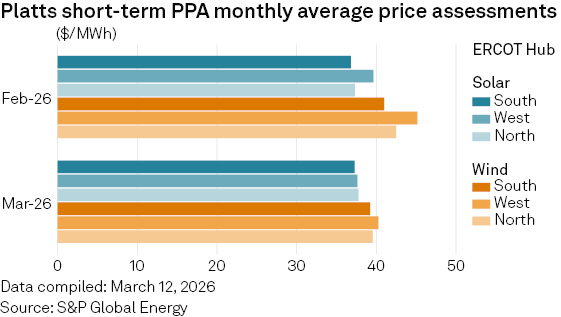

Pricing: wider dispersion around risk

Platts assessments on the ERCOT market for short term (12-60 months) solar PV PPAs were stable in the mid-$30s since the launch in February until mid-March. Short-term wind PPAs were assessed at a slight premium, ranging from $37.7/MWh (ERCOT South) to $38.3/MWh (ERCOT West). Platts is part of S&P Global Energy.

Long-term solar PPA prices for newbuild projects were assessed in a range of $40.59 (ERCOT West)-$41.33/ MWh (ERCOT South) as of March 12. The premium for long-term newbuild solar PPAs over short-term PPAs is currently running at approximately $3.2-$3.9/ MWh depending on the hub. The spread has widened in early March from levels closer to $1-$2/MWh seen in mid-February, indicating stronger demand for long-term offtake contracts relative to spot/short-term arrangements.

Platts also reported in early February that in PJM, bids for long-term solar newbuild virtual PPAs with 2027 start dates were at $75/MWh, while offers on REsurety's CleanTrade platform were in the $80-$83/ MWh range in early March. S&P Global Energy has exclusive access to transactional data on REsurety's CleanTrade platform to explore the development of spot market price assessments for PPAs and other clean energy instruments.

In the Southwest Power Pool (SPP), traditionally a wind-driven market, activity was seen mostly around solar newbuild projects in the South Hub, mainly for tenors of 15 years or more and generally starting post2028, with several at end-2029. Offers in February and March were in the $58-$75/MWh range, according to CleanTrade, with no bids seen. Some offers were also reported for the SPP North Hub in the $69-$72.5/MWh range. Wind PPAs are predominantly operational projects.

The MISO region saw bids for postbuild assets at $35$36/MWh while prices for long-term newbuild assets were reported between mid $50s-upper $60s/MWh during February and March.

By integrating S&P Global Energy's forward-looking cost models with real-time Platts assessments and transactional data from the REsurety CleanTrade platform, a clearer picture emerges around how PPA prices will be moving against fundamentals.

Horizons forecasts show prices will be increasingly reflecting both market fundamentals and delivery certainty. Horizons cost-based PPA forecasting indicates base-case solar PV PPA prices for 2027 commercial operation date projects ranging from April 2026 about $39/MWh in ERCOT West to $75/MWh in PJM Western Hub.

A key shift is how strongly price responds to performance risk. Under a lower-output case (capacity factor 15% below base), Horizons shows modeled 2028 solar PPA prices rising to about $52/MWh in ERCOT West and nearly $100/MWh in PJM, underscoring why buyers are increasingly focused on production uncertainty, curtailment exposure and settlement design.

Moving from volume to selectivity

Despite the resurgence in early 2026 deal activity, the next phase of the PPA market will not be necessarily defined by record-breaking volumes. Projects that can demonstrate bankable tax credit eligibility, realistic performance assumptions and credible timelines will increasingly stand out from the pack.

Volume alone is no longer enough to win offtake. Buyers that underwrite shape, curtailment exposure and tax credit risk up front will clear deals faster – and avoid unpleasant surprises post-COD. In this environment, operational assets are increasingly advantaged, capturing market share as buyers place less weight on additionality and more on delivery certainty.

Pricing expectations for newbuild projects reflect tighter market fundamentals and increasing sensitivity to risks around capacity factors. Solar newbuild PPA prices for 2027 range from $39/MWh in ERCOT West to $75/MWh in PJM Western Hub. Lower capacity factor assumptions can push prices 20%-35% higher, especially in constrained regions and nodes.

Looking ahead to 2028, Horizons base case price forecasts for newbuild solar rise into the $60s in ERCOT and $80s in PJM – levels that may test some buyers' willingness to transact. But with tax credit eligibility tightening and clean energy demand still accelerating, contracting is likely to persist.

In this context, short-term PPAs are well-positioned to gain traction, particularly as a growing share of operational fleets roll off legacy long-term contracts. Offtakers have also been less inclined to publicly announce short-term PPAs, reinforcing the perception that headline PPA volumes may be understating underlying contracting activity.

The early months of 2026 demonstrate that North American PPA markets are not slowing – they are evolving. And as the energy transition accelerates, the foundations being laid this year will shape the next generation of clean energy procurement, technology adoption and grid transformation.

This article contains views and forecasts from S&P Global Energy Horizons analysts.