S&P Global — 25 Oct, 2022 — Global

Daily Update: October 25, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Grim Days for Auto Industry

A weak automotive industry recovery risks running out of gas as production costs rise and consumer demand slips.

Between a global pandemic and the war in Ukraine, costs for vehicles are soaring, with average U.S. transactions nearing $46,000 in June. Demand has remained strong this year, but persistent shortages in components such as semiconductors continue to weigh on production.

U.S. auto sales declined 18% in the first half of 2022, mostly due to low dealership inventory, S&P Global Ratings credit analysts Nishit Madlani and David Binns wrote in a report. The analysts expect “only a gradual improvement” in access to key vehicle components through the rest of 2022, leading to a marginal decline in U.S. auto sales this year.

Given the continued uncertainties of the global supply chain, National Automobile Dealers Association Chief Economist Patrick Manzi does not expect automotive production to return to normal levels until 2024, Manzi told S&P Global Market Intelligence.

“That's what we're hearing from the [original equipment manufacturers],” Manzi said. “They are still dealing with supply constraints. One day, it's chips; the next day, it's tires. And then it might be wire harnessing.”

By the time production normalizes, the industry faces the prospect of a potential drop in consumer demand. Credit is getting more expensive as the U.S. Federal Reserve seeks to tame inflation by hiking its benchmark rates. Gas prices have been erratic as well this year, leading some consumers to rethink their driving habits.

In the meantime, consumers in the market for a new car are shedding brand loyalty as they shop for whatever is in stock, according to a report by S&P Global Mobility. New vehicle registration data from July indicated that industry brand loyalty dipped below 50%, hitting the lowest level of any month in three years.

For automakers and dealers, this represents both a warning and an opportunity, wrote Tom Libby, associate director of loyalty solutions and industry analysis at S&P Global Mobility. Once-loyal customers can no longer be relied upon to return. With targeted sales outreach and careful inventory management, however, some sellers could grab market share from struggling rivals.

The picture is somewhat bleaker in Europe, which faces the prospect of an especially cold winter if a prolonged war in Ukraine continues to constrain gas supplies from Russia.

Skyrocketing energy costs in Europe could lead continental manufacturers to churn out fewer vehicles, with forecasts from S&P Global Mobility and S&P Commodity Insights anticipating production losses of a million or more units starting in the fourth quarter.

It’s not just European car manufacturers that will feel the impact. European parts suppliers that ship all over the world will be affected by sharply higher costs.

"Anecdotally, we're hearing that some of this manufacturing capacity is becoming so uneconomic that companies are simply shutting up shop," said Edwin Pope, principal analyst of materials and lightweighting at S&P Global Mobility.

A prolonged energy crisis could result in lasting structural change for the automotive industry as suppliers seek production locations with greater energy self-sufficiency and lower costs.

In such a scenario, the Czech Republic could become a top European destination, according to an S&P Global Mobility analysis. Germany might also fare well, given its financial resources, low reliance on gas to power electricity and gas storage reserves.

Today is Tuesday, October 25, 2022, and here is today’s essential intelligence.

Written by Christina Mitchell.

Economy

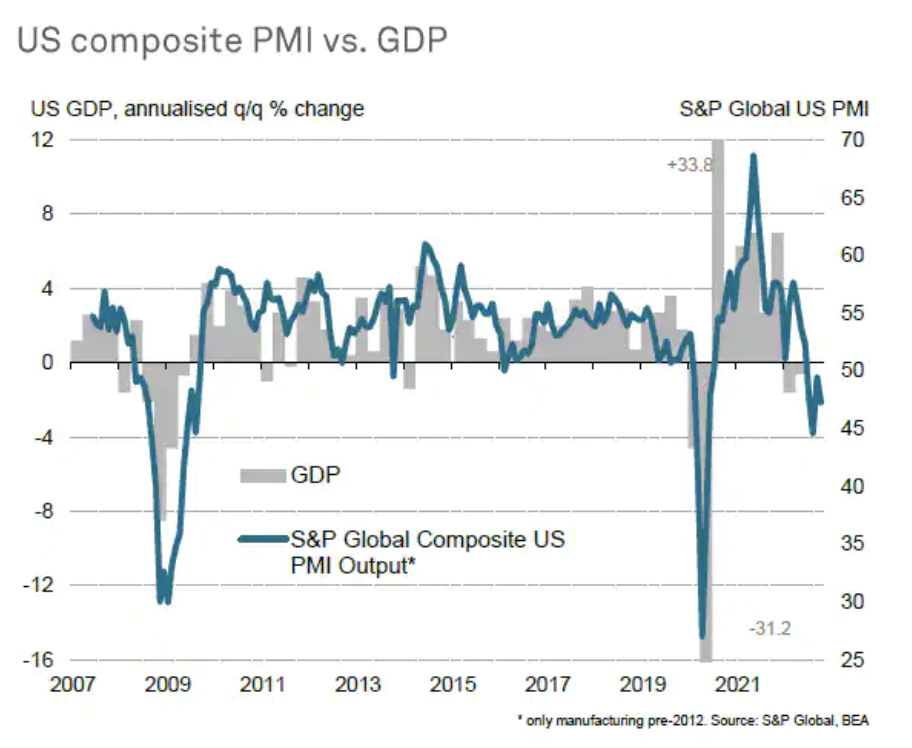

Flash U.S. PMI Falls Sharply Into Contraction Territory In October As Optimism And Demand Slumps

The October S&P Global flash PMI surveys present a picture of the economy at increased risk of contracting in the fourth quarter at the same time that inflationary pressures remain stubbornly high. Forward-looking indicators have also deteriorated. However, there are clearly signs that weakening demand is helping to moderate the overall rate of inflation, which should continue to fall in the coming months, especially if interest rates continue to rise.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

Pathways To Leadership: Empowering The Next Generation Of Powerful Women In Banking

This is the second annual wave of Arizent’s DEI research. The goal of this year’s research is to understand how diverse groups experience their workplaces and how different approaches to addressing diversity, equity and inclusion are impacting employees. This research was conducted online during July 2022. The data in this white paper comes from 180 respondents in the banking industry, from different types and sizes of organizations.

—Read the report on SPGlobal.com

Access more insights on capital markets >

Global Trade

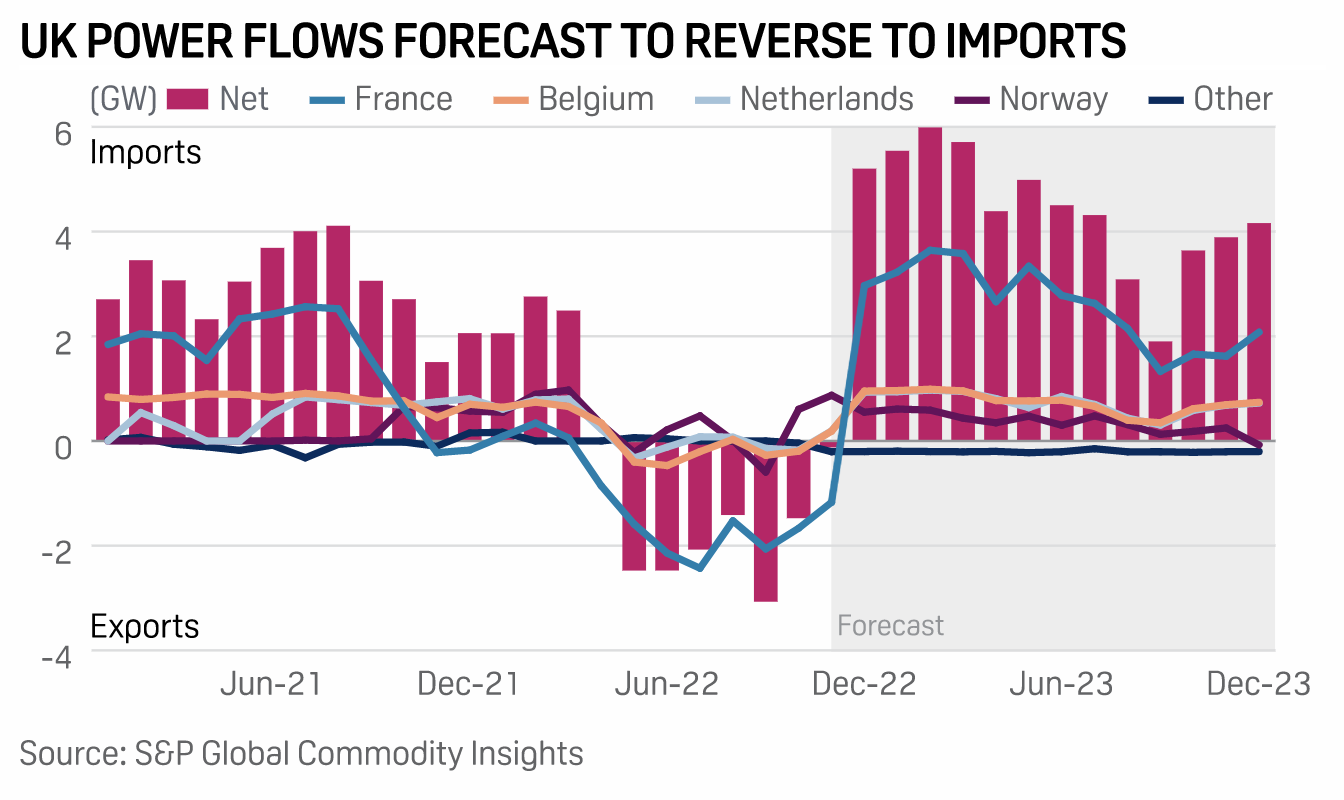

U.K.'s Record Power Exports To Europe Set To Reverse From November

Great Britain net exported over 8 TWh of electricity to EU markets over the summer, but flows are forecast to reverse over the coming weeks as a possible tug of war develops over scarce output, analysts at S&P Global Commodity Insights said in a report Oct. 20. GB, traditionally a net importer of power from the Continent on its 4 GW of interconnection, saw NBP gas prices fall to a steep discount to Europe's TTF gas price benchmark over the summer.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Women CEOs: Leadership For A Diverse Future

This S&P Global research aims to contribute to a better understanding of women leaders and their leadership styles during a time of economic uncertainty and workplace transformation. By analyzing the language of earning call transcripts of both men and women CEOs during the COVID-19 pandemic, this follow-up study found that women CEOs more frequently use terms associated with positive communication. Mapping language with various components of leadership styles, it observed that women CEOs more often articulate concepts of diversity, empathy, adaptability, and transformation.

—Read the report from S&P Global

Access more insights on sustainability >

Energy & Commodities

Fuel For Thought: As Asia Focuses On Energy Security, Diplomacy Takes A Backseat

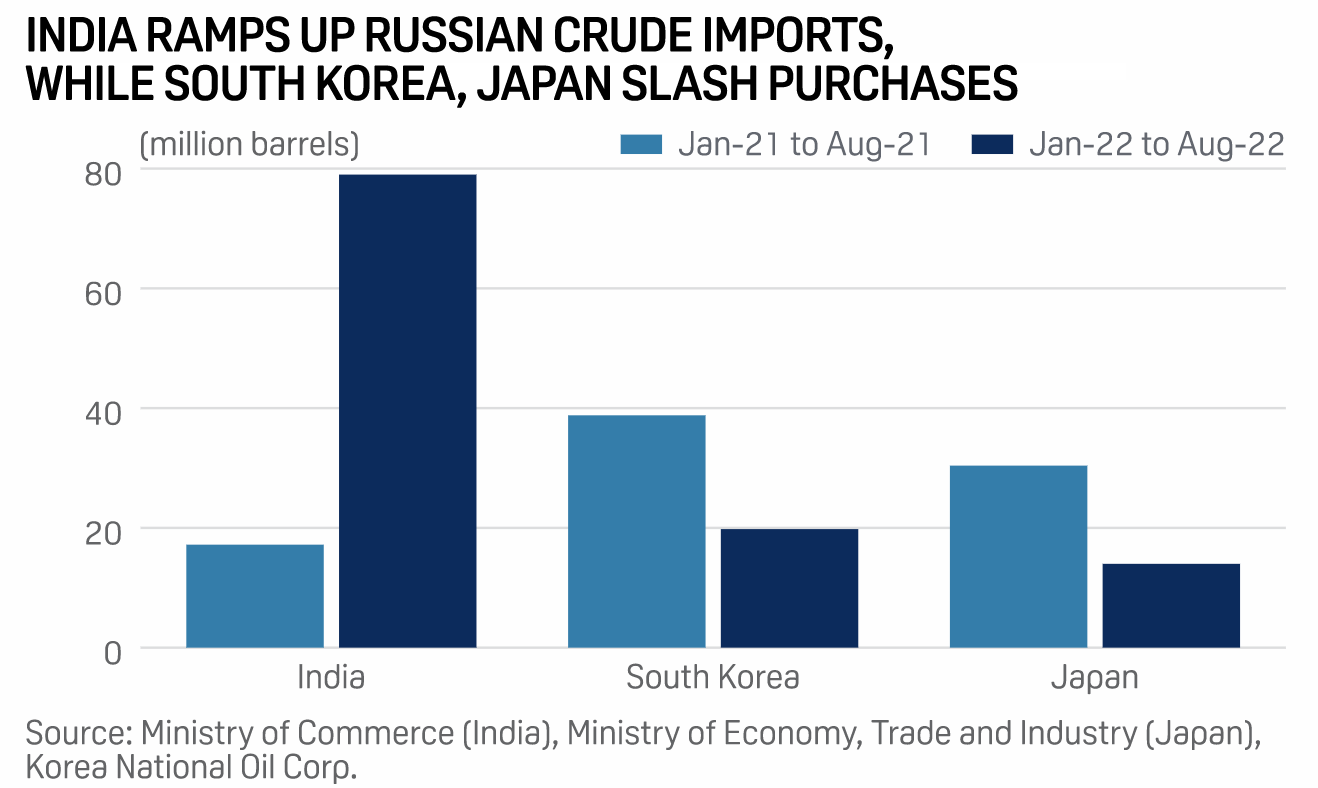

At a time when keeping fuel affordable is the prime concern of many import-dependent Asia energy consumers, diplomacy may be the last thing on the minds of their policymakers. Delegates who attended the Asia Pacific Petroleum Conference by S&P Global Commodity Insights in late September were unanimous in their view that as long as any trade is within legal bounds, many Asian countries will continue to buy oil from Russia despite the rest of the world preparing itself to get tougher on Moscow for its war on Ukraine.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

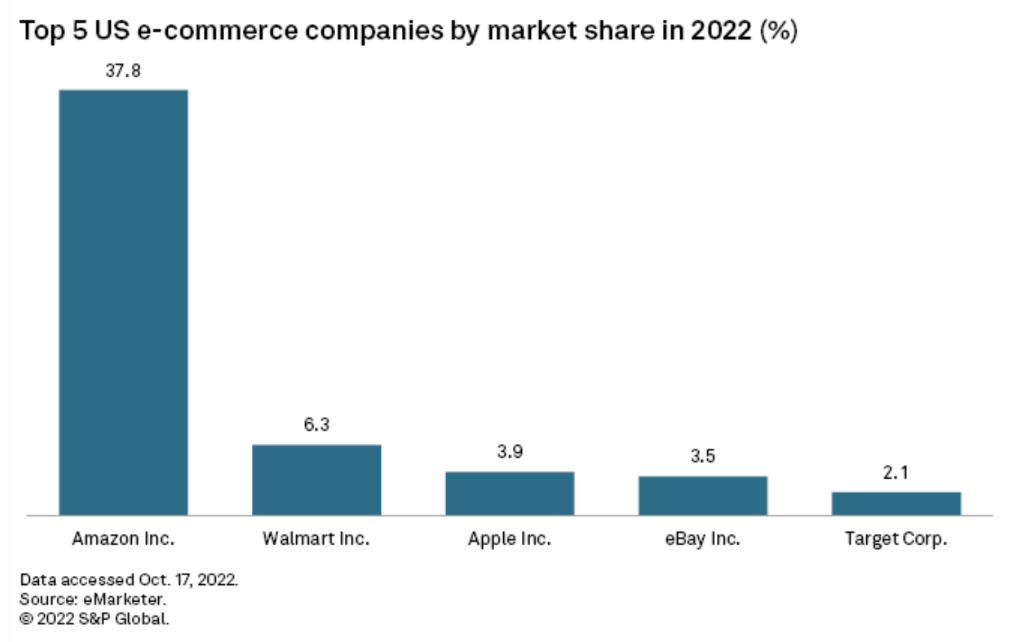

Amazon Drivers Push For Higher Pay Amid Heightened Pressure Ahead Of Holidays

Amazon.com Inc. is facing headwinds from retention challenges with its contract delivery drivers, according to drivers and labor experts who spoke to S&P Global Market Intelligence. Heading into the busy holiday sales season, drivers interviewed by S&P Global Market Intelligence said safety, pay and schedule pressures are contributing to worker dissatisfaction. While Amazon is likely to find the drivers it needs in the immediate term, retention issues are becoming a long-term risk, labor experts said.

—Read the article from S&P Global Market Intelligence