S&P Global — 24 Oct, 2023 — Global

Daily Update: October 24, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Southeast Asian Economies Strong Despite Tepid Trade

The Tan Cang – Cat Lai Terminal container port lies on the outskirts of Ho Chi Minh City near the mouth of the Soài Rap river. The terminal has access to several major highways, allowing manufactured goods to reach the port from the Vietnamese interior. The port can accommodate most ocean-going container ships as well as barges that come from upriver. While Tan Cang – Cat Lai is the largest of the Vietnamese container ports, its modern facilities and access to transportation networks are not unusual in the emerging market economies of Southeast Asia. With the prize of the major export markets of China, the EU and the US in the balance, Southeast Asian economies are developing into manufacturing powerhouses.

At first glance, the emerging markets of Southeast Asia appear to be experiencing difficult economic conditions. Global growth has stalled as decreased demand from developed markets has affected export-dependent emerging economies.

But things aren’t quite as bad as they appear. While mainland China experienced the sharpest fall in the Purchasing Managers’ Index (PMI) — a common measure of output for goods and services — the PMI for other emerging markets remained above the long-run average. In addition, strong domestic demand and steady employment have allowed many emerging market companies to pass on higher costs to consumers. While this results in modest inflation for some consumer goods, it is offset by weaker demand from developed markets.

S&P Global Ratings projects that five factors will determine the economic outlook for the emerging markets of Southeast Asia in 2024. Those factors are slower global growth, constricted capital flows, rate cuts in the US, fiscal policy consolidation and resilient domestic demand.

The developed economies in the US and Europe are projected to grow below trend in 2024. While that is bad news for countries that export to those markets, there are some indications that trade has bottomed out and started to recover, particularly for the electronics sector.

High interest rates in the US are drawing capital away from emerging markets, and volatile energy prices are putting pressure on current accounts for energy-importing countries such as Thailand, the Philippines and Vietnam. This could disrupt the disinflation process in these countries. However, monetary easing and fiscal policy consolidation in developed and emerging markets should ease some of this pressure. Domestic demand and strong regional employment numbers should protect Southeast Asian economies from the worst of a global slowdown.

Risks remain for emerging market economies in Southeast Asia. If the falloff in global growth is steeper than expected, no amount of domestic demand will protect these export-dependent countries. Inflation also remains a key concern, with higher oil prices and the potential for higher food prices during an El Niño year. Risks aside, the future looks bright for Southeast Asia.

Today is Tuesday, October 24, 2023, and here is today’s essential intelligence.

Written by Nathan Hunt.

Economy

Week Ahead Economic Preview: Week Of Oct. 23, 2023

Central bank meetings in the Eurozone and Canada will be the highlights next week alongside flash October PMI data for the earliest insights into economic conditions in major developed economies at the start of the fourth quarter. Additionally, the US releases Q3 GDP and other key economic indicators such as durable goods orders, core PCE and personal income and spending figures. Several tier-1 data are also expected from APAC economies.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

Biggest Banks Show Relative Strength Again In Q3 Earnings Reports

The four biggest US banks extended a string of earnings reports that have exceeded grim expectations for the sector this year with third-quarter results that beat earnings-per-share forecasts across the board. Three posted sequential expansion in net interest margins (NIMs) for the period, with all also coming in ahead of analyst forecasts on the measure, according to data from S&P Global Market Intelligence. All four also raised their net interest income guidance for the year.

—Read the article from S&P Global Market Dynamics

Access more insights on capital markets >

Global Trade

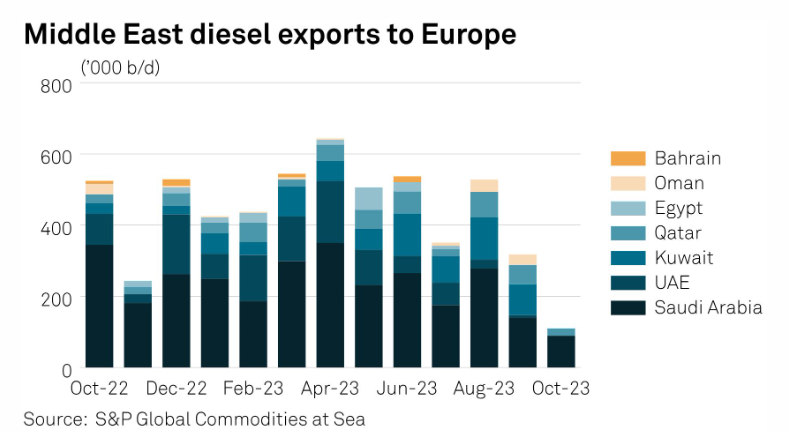

Middle East Diesel Exports To Europe Slow As US Steps In

Middle East diesel shipments to Europe have slowed while the US has moved in with more supplies after Russia's temporary ban on exports. Europe's diesel imports are averaging 165,000 b/d for October, more than the pace in September at 136,000 b/d, according to S&P Global Commodities at Sea data. The Middle East shipments to Europe are running at 110,000 b/d, with exports from Saudi Arabia and Qatar well below the September total pace of 317,000 b/d.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

ESG In Credit Ratings October 2023: ESG-Related Rating Actions Hit A 2023 Monthly Low

Total ESG-related rating actions decreased to 10 in September from 16 in August, marking a year-to-date low, as negative actions continued to lead positive ones, by four to one. Governance factors remained the primary driver, with seven rating actions, followed by social factors with three. Six of the seven governance factor-related rating actions in September were negative, with the largest concentration being risk management, culture and oversight.

—Read the article from S&P Global Ratings

Access more insights on sustainability >

Energy & Commodities

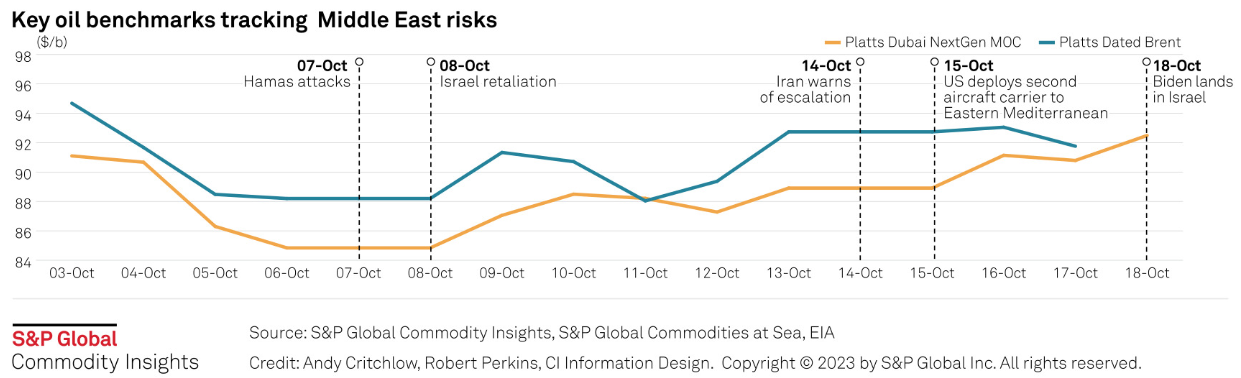

Infographic: Escalation Of Israel-Hamas War Could Put Middle East Oil Flows At Risk

With war ongoing between Israel and militant group Hamas, oil markets are on edge after Iran warned the conflict could escalate across the Middle East. The region's energy infrastructure and key shipping chokepoints are at risk should the conflict spread, which could send oil prices soaring and dramatically impact supply.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

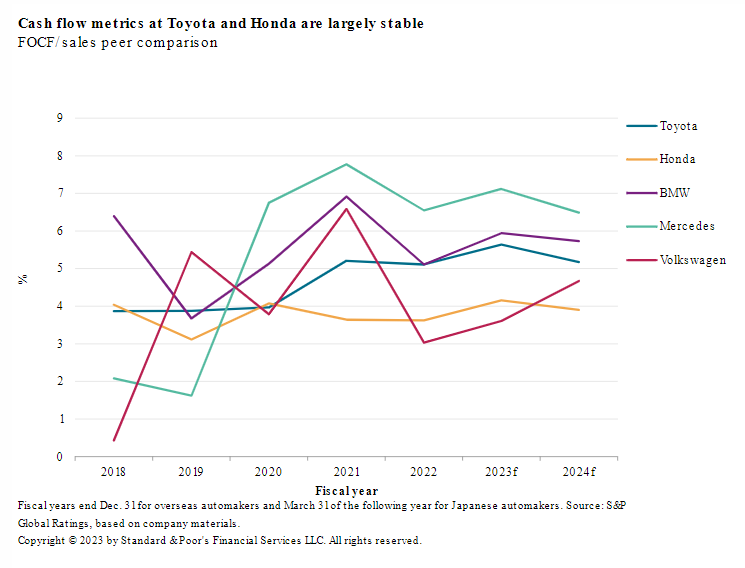

Japan Autos: Prepared For Weaker Momentum And Secular Change?

For Japan's automakers, things look good for now. Strong pent-up demand and easing semiconductor shortages in key markets including Japan, Europe and the US are all positive factors for key Japanese companies. A weak yen also underpins their performance. In addition, the companies will benefit from moderate growth in demand and improving operating efficiency, in S&P Global Ratings’ view. S&P Global Ratings therefore expects credit profiles for Japanese automakers to remain stable over the next one to two years.

—Read the article from S&P Global Ratings