S&P Global — 8 Apr, 2021

Daily Update: April 8, 2021

By S&P Global

Subscribe on LinkedIn to be notified of each new Daily Update—a curated selection of essential intelligence on financial markets and the global economy from S&P Global.

This year will be key in the London Inter-Bank Offered Rate (LIBOR) transition. While regulators have been warning financial companies for years that the benchmark interest rate—which indicates the borrowing costs for global banks’ short-term loans in the international interbank market—would be phased out by year-end 2021, the seismic shift away has been extended. This will become effective after December 2021 for sterling, euro, yen, and Swiss franc LIBOR settings and after June 2023 for most U.S. dollar settings. Nonetheless, market participants are approaching the change at varying speeds.

"I think they start getting an urgency in the first six months of 2021," Richard Sandor, chairman of American Financial Exchange and creator of Ameribor, a proposed LIBOR alternative, told S&P Global Market Intelligence. "If they are lending money beginning in January for a term of one year or more, they're going to run into trouble. The regulators will not be pleased with people entering into loans with Libor that extend beyond 2021."

Countries are likely to have divergent experiences undertaking the transition to a new benchmark rate, according to S&P Global Ratings. In Japan, the effect of losing LIBOR could be challenging, while the process for Australian banks is expected to be smooth. Latin America’s exposure is anticipated to be minimal. Banks, structured finance markets, and other financial institutions across Europe and the United Kingdom will likely benefit from the transition.

The most common alternative in U.S. debt markets to LIBOR is the Secured Overnight Financing Rate (SOFR), a volume-weighted median of transaction-level U.S. Treasury repurchase agreements data that reflects the cost of borrowing overnight collateralized by U.S. Treasury securities.

There are three distinct differences between the USD LIBOR and SOFR benchmark rates, according to S&P Dow Jones Indices.

Firstly, SOFR is an overnight rate, and the USD LIBOR benchmark includes seven tenors of forward-looking term rates.

Additionally, SOFR is nearly risk-free as an overnight secured rate collateralized with U.S. Treasury bonds, while LIBOR is credit sensitive and embeds a bank credit risk premium.

Finally, the divide between the two rates is most significant regarding their transaction rates. “SOFR is based on observable transactions in the largest rates market in the world at a given maturity. Since SOFR’s first publication in April 2018, the daily average volume of trades underlying it is about $977 billion. In comparison, the Fed estimates that on a typical day, there are a handful of transactions worth a few hundred million dollars at most that underpin total seven tenors of USD LIBOR in the term unsecured bank funding market,” S&P Dow Jones Indices said in a recent report. “In fact, diminishing transactions underlying LIBOR is one of the main reasons that authorities are pushing the financial industry to transition away from LIBOR to more robust reference rates that are based on observable transactions rather than estimates.”

While market participants have made strides in transitioning away from the benchmark rate and recognize the urgency for doing so, "people know what to expect [with LIBOR], and we just don't have a term structure yet for SOFR," Nitish Idnani, a principal with Deloitte & Touche LLP, told S&P Global Market Intelligence. Overall, the transition is "not just a sell-side topic anymore. Insurance companies, asset managers, they're all very focused on it … Over the last year or so, we've seen significant interest across financial services on what it means for them, which is encouraging."

Today is Thursday, April 8, 2020, and here is today’s essential intelligence.

Market Dynamics

Supply Woes Drive Mexican Steel Prices to 13-Year Highs

A long-standing regional supply shortage, aggravated by COVID-19 impacts, has prompted steel prices in Mexico to jump to 13-year highs, while local demand is yet to recover. Higher raw materials prices, coupled with a strong US dollar, were also drivers of a trend that is not expected to end in the short term. Adriana Carvalho, S&P Global Platts managing editor for Latin American metals, and Claudia Cardenas, pricing specialist of Mexican metals pricing, examine the trends influencing the markets and present the latest updates on Platts methodology and specifications for Mexican flat steel pricing.

—Listen and subscribe to Commodities Focus, a podcast from S&P Global Platts

The Future of Credit

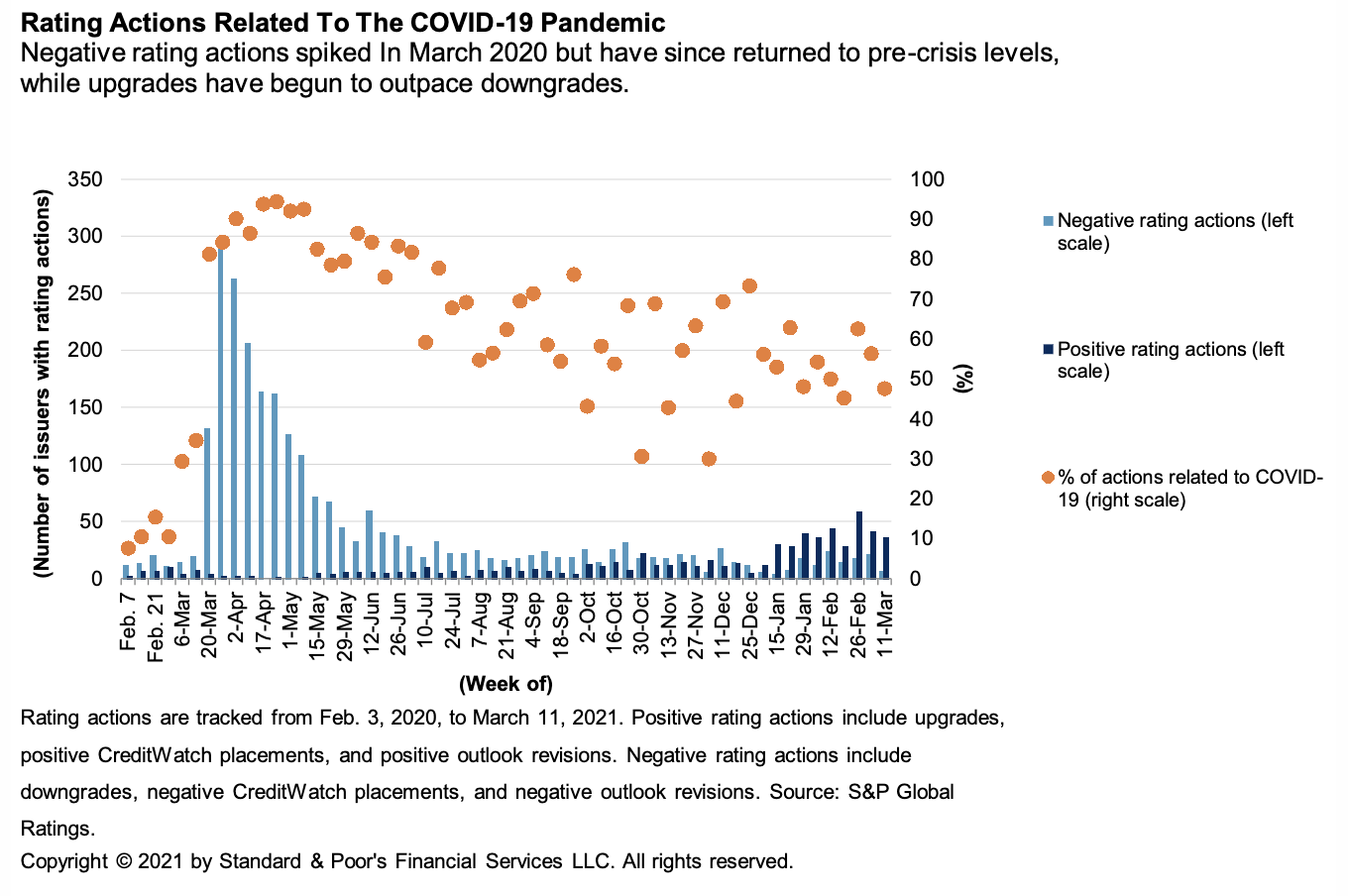

A Look Back at How The COVID-19 Pandemic Affected Creditworthiness Globally

A little over a year ago, the World Health Organization declared COVID-19 to be a global pandemic, and the world plunged into a steep economic downturn. A slew of negative rating actions quickly followed as S&P Global revised its assumptions to reflect the emerging risk of a sudden drops in revenues. The ratings impact was especially pronounced for weaker, more highly leveraged companies entering the downturn and issuers in sectors heavily affected by social distancing.

—Read the full report from S&P Global Ratings

The Global Business Services Sector is Poised for Growth

S&P Global Ratings believes the business and consumer services industry worldwide is poised for growth this year, after some turbulence in 2020 as a result of COVID-19-related shocks and the ensuing global economic recession. S&P Global Ratings has taken negative rating actions on more than one-third of the companies S&P Global Ratings rates globally in this sector over the past 12 months.

—Read the full report from S&P Global Ratings

Banking Sector Under Pressure

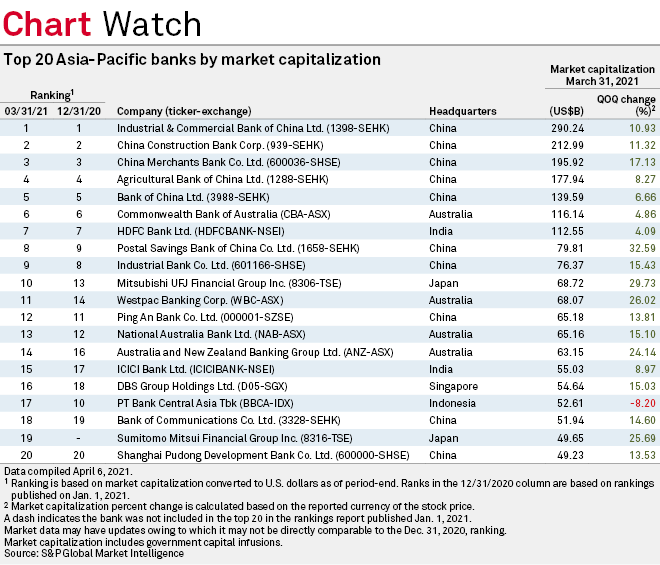

Major Asian Banks Log Market-Cap Growth in Q1 as Economic Recovery Persists

All but one of the 20 largest banks in Asia-Pacific saw growth in their market capitalization during the quarter ended March 31, continuing the momentum from the previous quarter, as economic recovery from the COVID-19 pandemic persisted across the region.

—Read the full article from S&P Global Market Intelligence

Technology & Media

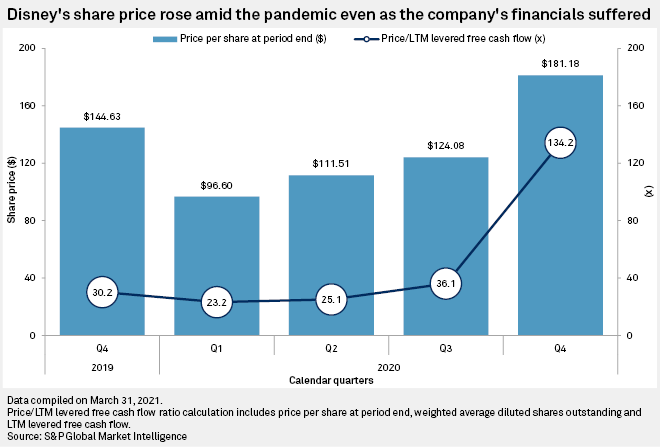

Disney's Pandemic Project: from Mouse House to Mouse Platform

Like many firms, Disney shares took an initial dive in 2020 when it became clear there would be no big screens on which to debut its big-budget blockbusters, no crowds to congregate at its theme parks and less advertising for its TV networks. Shares hit a low point on March 23, 2020, down over 40% from New Years’ Day. By comparison, the S&P U.S. BMI Media and Entertainment Index was off around 26% and the S&P 500 was down about 30%. But the company's investments in its streaming platform seemed to come at the exact right time. On April 8, 2020, Disney reported 50 million subscribers for Disney+, less than five months after the service launched in the U.S. Those numbers helped push a 22% recovery for the stock from the pandemic low.

—Read the full article from S&P Global Market Intelligence

ESG in the Time of COVID-19

In ESG Era, New Green Asset Ratio Could Give Europe's Banks an Edge Over Rivals

European banks may gain an edge over their U.S. peers with a proposed "green asset ratio" designed to give investors clarity on increasingly important environmental issues, according to market participants. The European Banking Authority has recommended that banks adopt a greet asset ratio, or GAR, to show how their economic activities are environmentally sustainable, putting the proposal out to consultation.

—Read the full article from S&P Global Market Intelligence

Enbridge Sticks to 'All-Of-The-Above' North American Oil, Gas, Renewables Strategy

Canada's Enbridge expects future spending on growth projects to be more heavily weighted to natural gas and renewables than oil, as it works to meet its carbon reduction goals, CEO Al Monaco said April 7.

—Read the full article from S&P Global Platts

The Future of Energy & Commodities

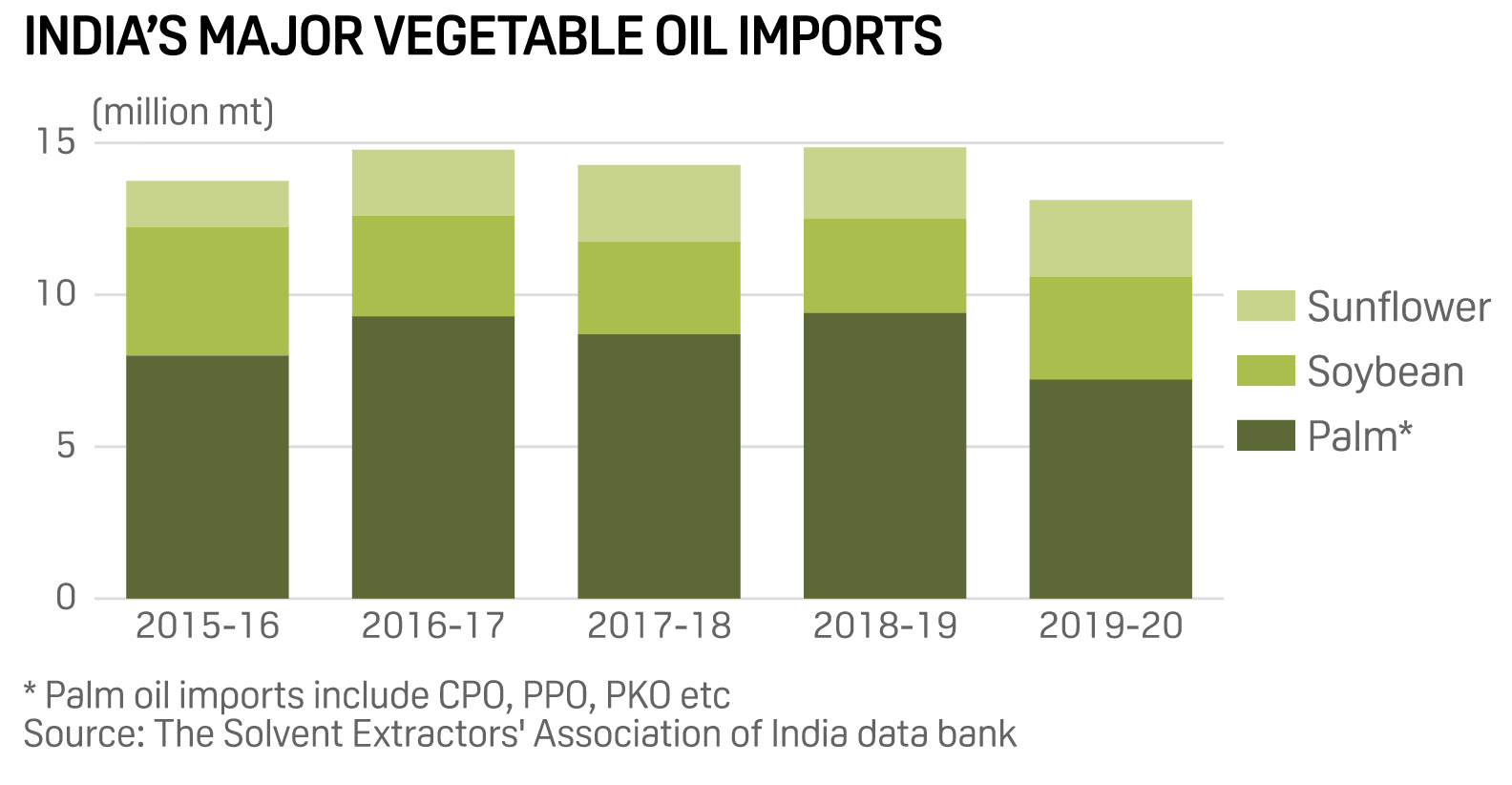

Pandemic Fears, High Prices to Stall India's Vegoil Demand Recovery in 2021: Sunvin CEO

India's vegetable oil imports are set for another subdued year in 2021 as refiners pass on high prices to the consumers and a resurgence of the coronavirus pandemic looms large in the country, according to Sandeep Bajoria, CEO of Mumbai-based vegetable oil broking firm Sunvin Group.

—Read the full article from S&P Global Platts

U.S., Iran Inch Closer to Reviving Nuclear Deal After Vienna Talks

The US and Iran appear to have made headway in their indirect talks in Vienna over restoring the nuclear deal, improving the prospects of sanctions relief that could see severe restrictions on Iranian oil sales lifted.

—Read the full article from S&P Global Platts

Chilean Mining Sector Expected to Be Undeterred by 2nd Wave of COVID-19

The copper mining hub of Chile is grappling with a large second wave of coronavirus infections amid a national lockdown, yet the mining sector could be poised to push through the crisis largely unimpeded.

—Read the full article from S&P Global Market Intelligence

Written and compiled by Molly Mintz.

Content Type

Location

Language