S&P Global — 7 Apr, 2022 — Global

Daily Update: April 7, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Full Speed Ahead for the Fed

Against the backdrop of heightened market uncertainty and volatility, persistent inflationary pressures, and a flat U.S. Treasury yield curve, Federal Reserve officials plan to reduce the central bank’s balance sheet by $95 billion a month alongside aggressively raising interest rates, with at least one hike of 50 basis points (bps) this year.

In the Federal Market Open Meeting Committee’s minutes from its March 15-16 meeting, released yesterday, Fed officials “generally agreed” that the central bank would reduce its nearly $9 trillion balance sheet by a $60 billion in Treasuries and $35 billion in mortgage-backed securities over three months likely beginning in May. The minutes also noted that “many” central bankers believe one or more 50-bps rate hike could be appropriate if inflation pressures intensify.

The U.S. central bank "will continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a rapid pace as soon as our May meeting," Fed Governor and Vice-Chair nominee Lael Brainard said on Tuesday following the release of the minutes, adding that she "expects the balance sheet to shrink considerably more rapidly" now than when the Fed established a pace of $50 billion in monthly holdings reductions during the 2017-2019 period.

“Minutes from the march FOMC meeting all but ensured that the Federal Reserve plans an aggressive monetary policy campaign to combat four-decade high price readings. We anticipate seven rate hikes total in 2022, including a 50-bps rate hike at the Fed’s policy meeting in May, and that the Fed will announce the start of quantitative tightening in May,” S&P Global Ratings Chief North America Economist Beth Ann Bovino told the Daily Update. “But based on the hawkish statements from the FOMC minutes, markets may need to brace themselves for even more this year.”

The U.S.’s solid jobs growth—with 431,000 jobs added to U.S. nonfarm payrolls and a net 95,000 job gains in January and February, according to the Bureau of Labor Statistics' March jobs report—is laying the foundation for the Fed to act sooner and stronger due to confidence that the strong economy can absorb tighter policy and continue to grow, according to Dr. Bovino’s recent research.

“The minutes of the Fed’s March meeting were released yesterday, and the markets did not like them,” Benedek Vörös Director, director of index investment strategy at S&P Dow Jones Indices, said in a market note today. “The result was a classic ‘sell everything’ day—bonds, stocks, gold, and oil all dropped while credit spreads widened and VIX moved up to 22. This morning, European equities are mounting an early comeback, U.S. futures are indicating modest gains, but Asian markets finished today’s trading with losses.”

The market sell-off “wasn’t that bad,” Mr. Vörös said. “But it was widespread.” The S&P 500 benchmark index closed down 1% yesterday, while every region of the S&P Developed BMI and 20 out of 24 S&P Emerging BMI regions declined. But this doesn’t necessarily indicate more to come, as historical performance over the last two decades doesn’t indicate a clear link between changes in interest rates and changes in the equity market, according to S&P Dow Jones Indices.

Following the release of the FOMC minutes and Fed Governor Brainard’s public comments, yields on benchmark 10-year U.S. Treasury notes reached 2.56%, the highest level seen in three years. U.S. bonds suffered their worst quarter in more than 40 years the January-March of this year, and investors are closing watching the yield curve as a potential indicator of a recession in the U.S. economy. At the same time, the spread between two- and 10-year Treasury yields narrowed notably in March—and low spreads are also often seen as an indicator of recessions.

Still, the Fed appears to be moving forward with its aggressive policy plans amid low bond yields due to companies' healthy corporate balance sheets, and a sizable reduction in corporate demand for debt, according to S&P Global Market Intelligence.

Today is Thursday, April 7, 2022, and here is today’s essential intelligence.

Written by Molly Mintz.

Economy

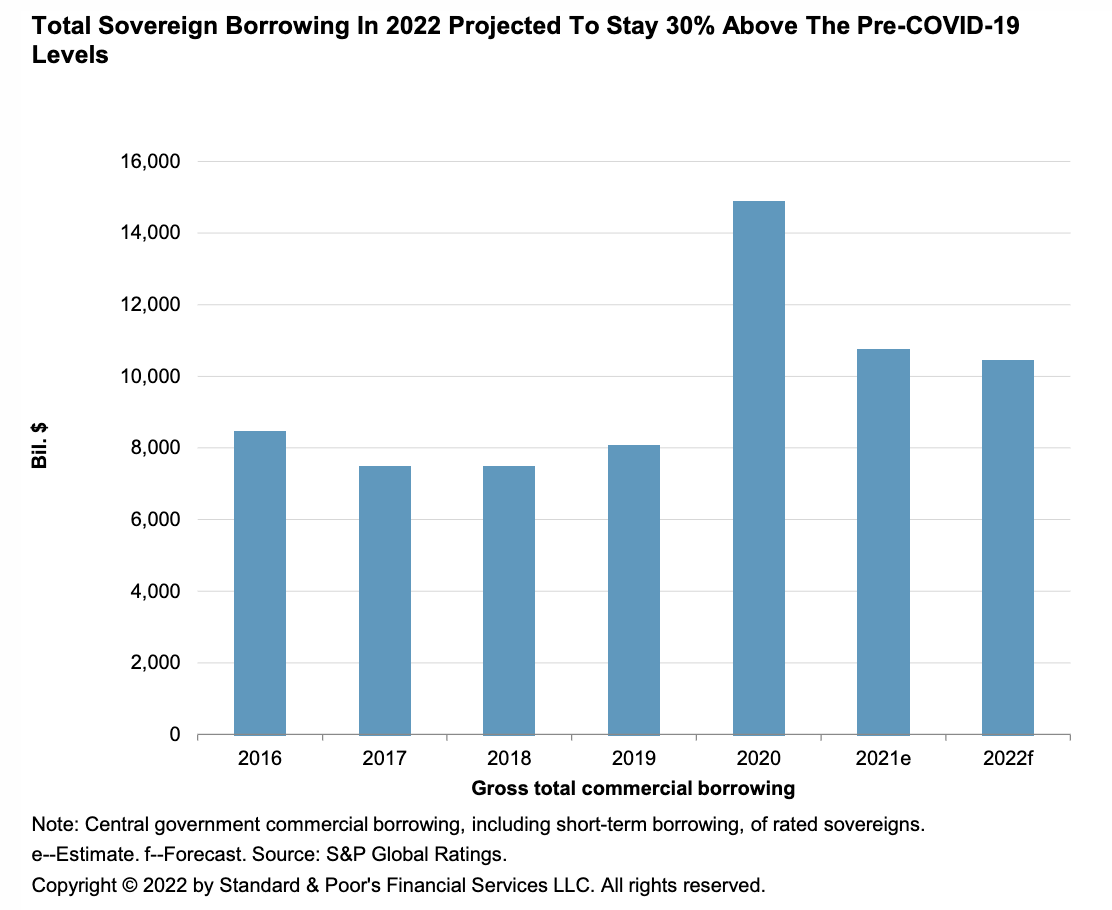

Sovereign Debt 2022: Borrowing Will Stay High On Pandemic And Geopolitical Tensions

S&P Global Ratings estimates sovereign borrowing will reach $10.4 trillion in 2022, nearly one-third above the average before the COVID-19 pandemic. Despite an economic recovery, it expects borrowing to stay elevated, owing to high debt rollover needs, as well as fiscal policy normalization challenges posed by the pandemic, high inflation, and polarized social and political landscapes. The global macroeconomic repercussions of the ongoing military conflict between Russia and Ukraine will put further upward pressure on government funding needs this year. Tightening monetary conditions will push up government funding costs. This will pose additional difficulties to sovereigns that have been unable to restart growth, reduce reliance on foreign currency financing, and where interest bills are already critically high.

—Read the full report from S&P Global Ratings

Access more insights on the global economy >

Capital Markets

With Recent Surge, YTD U.S. Leveraged Loan Returns Edge Into Positive Territory

The S&P/LSTA Leveraged Loan Index gained 0.14% on April 4, lifting the year-to-date return for the segment to 0.19%. Just three weeks ago, on March 15, U.S. loans were down 2% for the year as geopolitical risk gripped asset classes worldwide and cast a pall of uncertainty over the financial landscape. Since hitting that low point, however, secondary loan prices have rebounded strongly—the index gained 2.25% between March 16 and April 4. The riskiest names continue to underperform this year. Both single-B and double-B sub-indices are now in the black in 2022, while triple-Cs remain in the red, down 0.86% as of April 4. Single-B names have a small edge over their higher-rated counterparts, at 0.33% to 0.13%, based on total return.

—Read the full article from S&P Market Intelligence

Access more insights on capital markets >

Global Trade

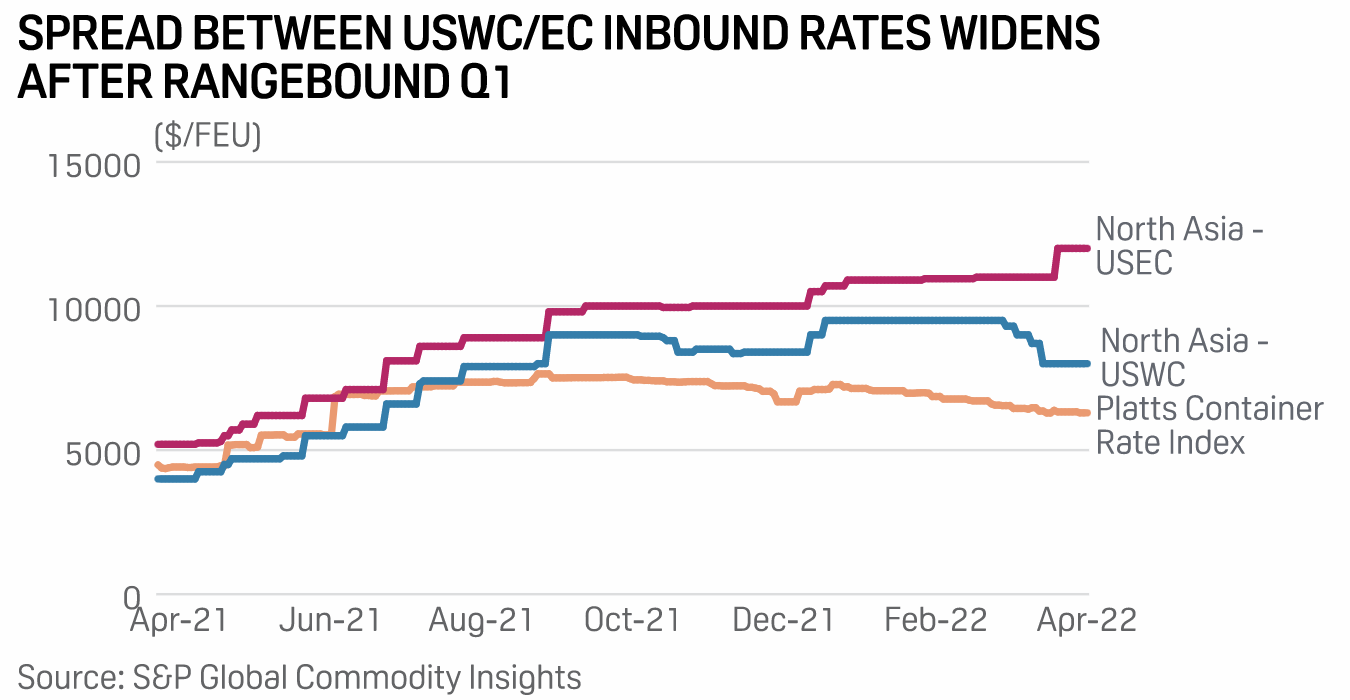

Container Quarterly: Shippers Look To USEC Gateways Amid USWC Congestion, Uncertainty

Shippers importing goods into the United States from Asia have been allotting more cargos to the U.S. East and Gulf coasts in an effort to avoid congestion and diversify their risk ahead of potential industrial action at USWC ports, sources said. The shift comes as many North American ports continue to grapple with vessel lineups and congested terminals, unable to efficiently move containers due to inland logistical constraints. Vessel queues outside of the Ports of Los Angeles/Long Beach peaked in January at 109 and have since fallen to just 33 vessels on April 4. Vessel wait times remain unpredictable, sliding from 10 to 40 days depending on terminal availability.

—Read the full article from S&P Global Commodity Insights

Access more insights on global trade >

ESG

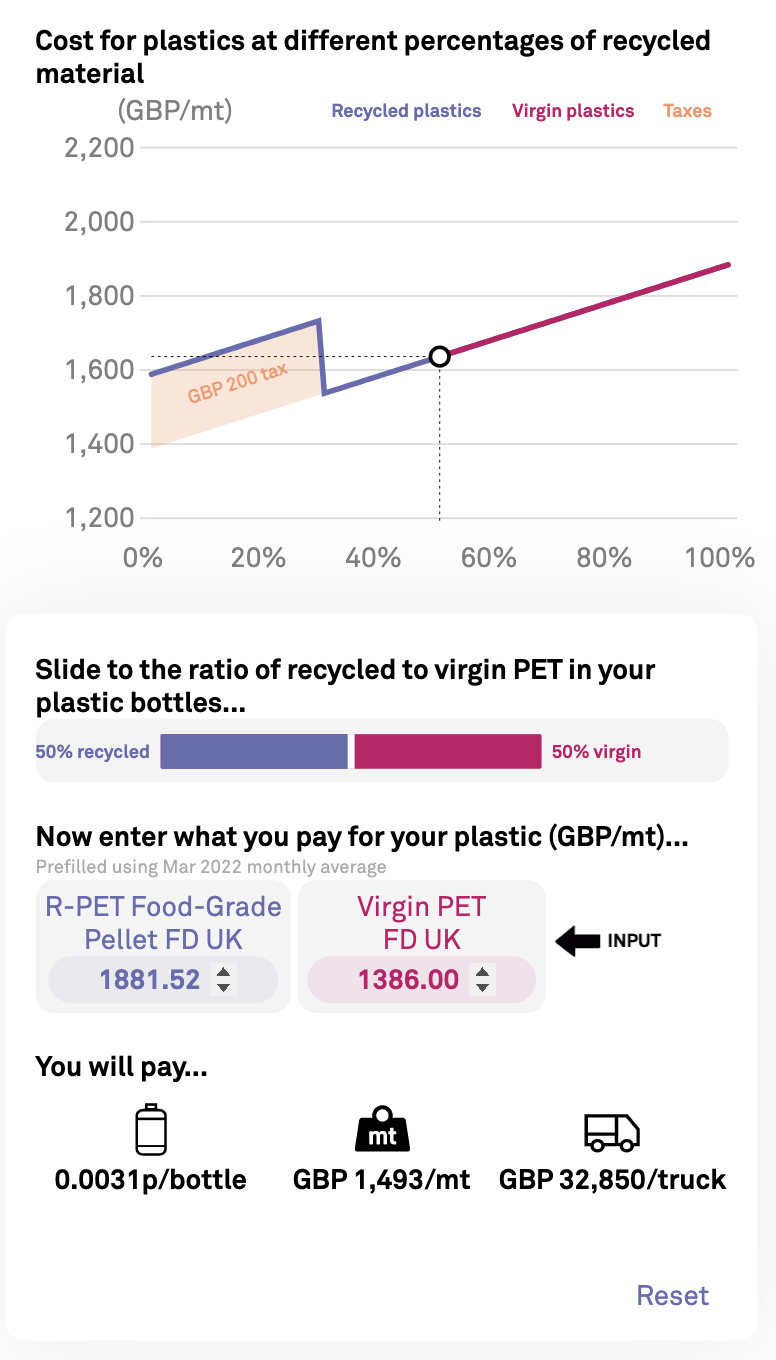

Interactive: U.K. Plastic Tax Calculator

In April 2022, the U.K. introduced a tax on plastic packaging. The tax, introduced to help reduce plastic waste pollution, is the first of its kind globally to cover all types of plastic packaging. Under the new rules, any packaging that is predominantly plastic by weight made in or imported into the U.K. for final sale to the consumer will have to include 30% recycled plastic as a minimum. If the recycled content falls short of this inclusion rate, a £200/mt tax on the total weight of the package will be due.

—Read the full article from S&P Global Commodity Insights

Energy & Commodities

Listen: The Rise Of Asia’s Carbon Trading Hubs

Asia's carbon markets are on a trajectory of rapid growth as demand for carbon offsets rises and regional governments work towards net-zero commitments. While turmoil in global energy markets has temporarily shifted attention to energy security, commodity trading hubs like Singapore are pushing ahead with plans to become a carbon trading powerhouse. Eric Yep and Roman Kramarchuk of S&P Global Commodity Insights discuss with Mikkel Larsen, CEO of Climate Impact X, a Singapore-based carbon exchange, on what lies ahead for Asia's carbon markets.

—Listen and subscribe to Future Energy, a podcast from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

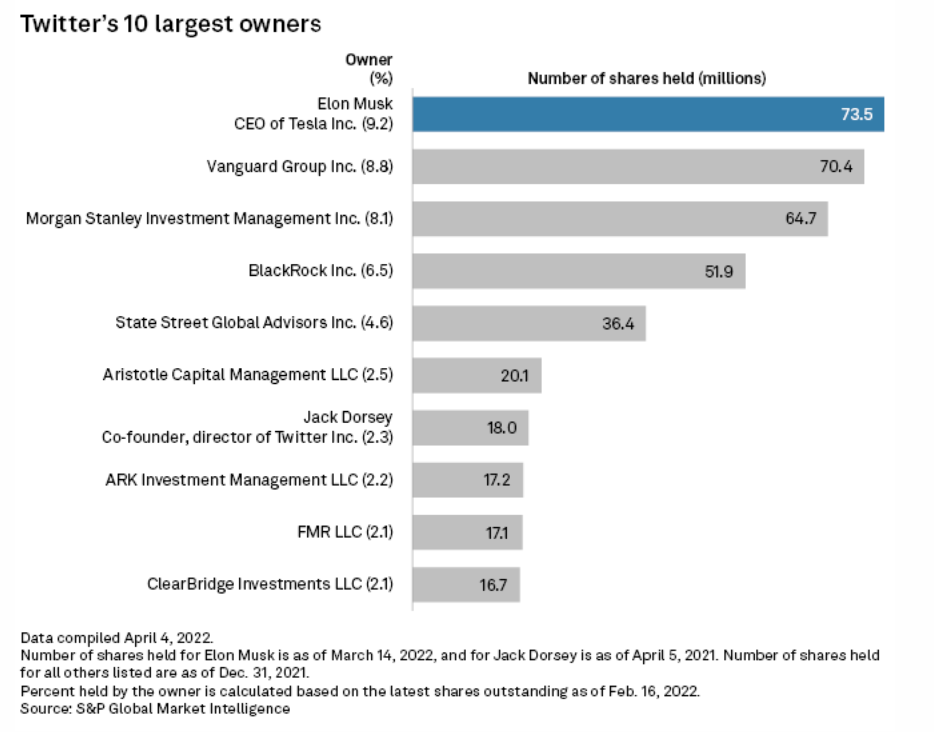

Gauging Elon Musk's Intentions For Twitter As He Takes Board Seat

Twitter Inc.'s newest director and largest shareholder is both a power user and an outspoken critic of the microblogging platform. On April 4, Twitter's management agreed to appoint Elon Musk, CEO of Tesla Inc. and Space Exploration Technologies Corp., to a two-year director term expiring in 2024, according to an SEC filing. Twitter CEO Parag Agrawal and Musk confirmed the move in an exchange on the platform April 5. "[Musk is] both a passionate believer and intense critic of the service which is exactly what we need on @Twitter, and in the boardroom, to make us stronger in the long-term," Agrawal wrote.

—Read the full article from S&P Global Market Intelligence