S&P Global — 18 Apr, 2023 — Global

Daily Update: April 18, 2023

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

With Markets in Turmoil, Petrochemicals Suffer Hangover From Building Boom

Turmoil in global petroleum markets, fueled by high interest rates, the prospect of economic slowdowns in many regions and Russia’s invasion of Ukraine, has hit the petrochemical sector, which is staring at a long-predicted contraction in production capacity over the next several years.

Analysts and executives have long highlighted the industry’s supply overhang, but a variety of factors — including the February 2021 winter storm, which virtually shut down the US Gulf Coast petrochemical complex — have delayed the reckoning, according to S&P Global Market Intelligence.

“The massive build-out of petrochemical capacity” since the Great Recession of 2008–2009 “is finally starting to catch up to the market,” Rob Westervelt, editor in chief of S&P Global Commodity Insights’ Chemical Week, said during a recent podcast.

Commodities prices and earnings by major petrochemical companies both spiked in 2020, in the early months of the COVID-19 pandemic, said Kristen Hays, global market lead for polymers at S&P Global Market Intelligence. But “several factors changed that a year ago,” including the war in Ukraine, growing recession concerns, falling housing and vehicle sales, and the pandemic lockdowns that shrank demand in China. The margins of big producers such as Dow Chemical and LyondellBasell Industries, which spiked during the pandemic’s height, have cratered to about 5%, according to earnings reports. And prices for natural gas, a key feedstock in many refining processes, remain stubbornly high after soaring at the start of the Russia-Ukraine war.

As a result, the building boom in production and refining capacity has screeched to a halt.

“New plants that were originally expected to come online in 2022 have been pushed into at least the first half of 2023,” said Clay Boswell, markets editor at Chemical Week. “Nobody is in a hurry to bring this stuff online and add to global capacity.”

The effects of the war in Ukraine are being felt as far away as South Korea, Asia’s biggest importer of naphtha, which is used by refiners to blend gasoline. The country imported 57.6 million barrels of naphtha from Russia in 2021. In 2022, that figure tumbled 72%, and shipments from Russia have essentially ceased this year. To make up the lost supplies, South Korean refiners have turned to North Africa, importing 5.3 million barrels of naphtha from Algeria in January 2023.

Meanwhile, overall global commodities prices have fallen by more than one-third in the past year, according to S&P Global Market Intelligence’s Material Price Index, although they remain well above pre-pandemic levels. Chemical prices have seen a modest rebound recently, with the spot price for propylene climbing nearly 50% week over week to 76 cents per pound in the week of March 6. That bounce is expected to be short-lived.

“Chemical demand remains weak by historical standards,” wrote Michael Dall, associate director for pricing and purchasing at S&P Global Market Intelligence. “Markets continue to grapple with mixed signals on global economic growth.”

A turnaround in the petrochemicals sector is likely years away. Ethylene demand, for example, is expected to increase by 8.8 million metric tons in 2023, according to S&P Global Market Intelligence data. But production capacity will increase by 9.8 million metric tons per year.

“The fundamental mismatch between supply and demand remains, and it will grow,” Boswell wrote March 6.

Today is Tuesday, April 18, 2023, and here is today’s essential intelligence.

Written by Richard Martin.

Economy

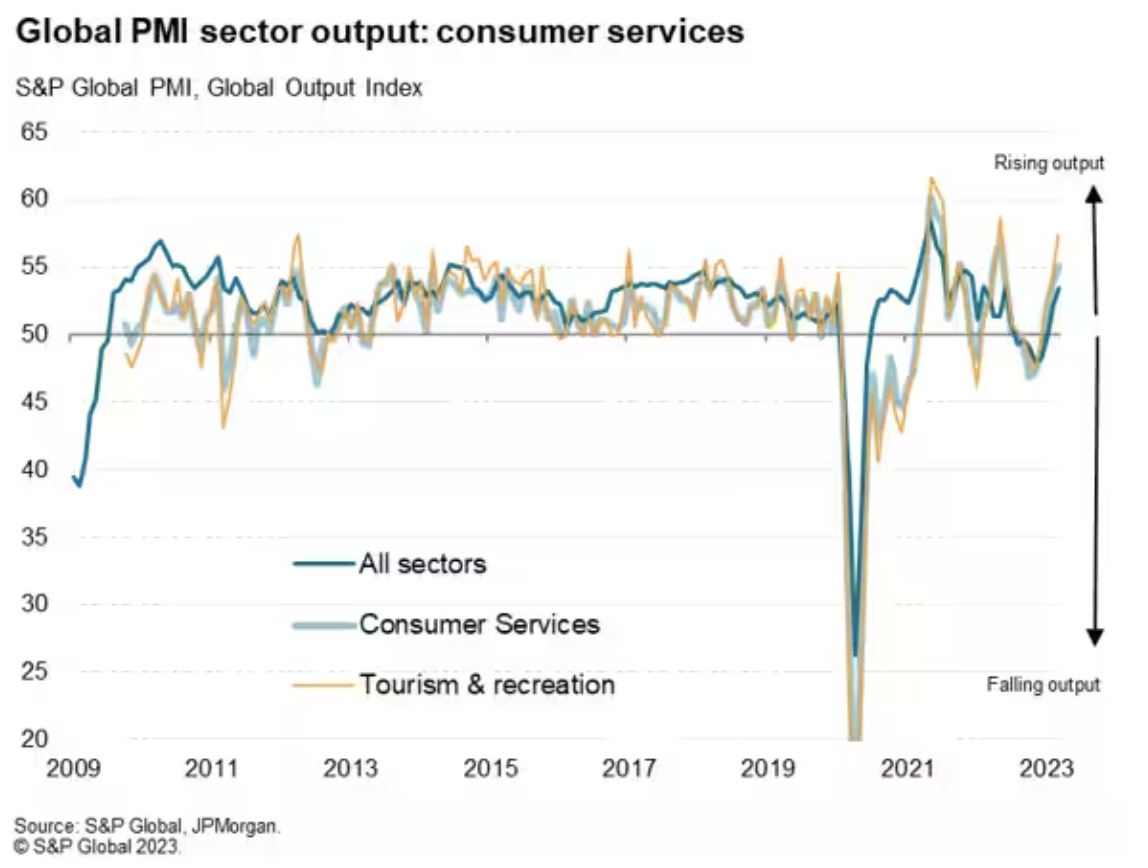

Consumer Services Drive Global Economic Expansion In March Amid Travel Surge

Detailed sector Purchasing Managers' Index (PMI) from S&P Global reveal how faster than anticipated economic growth in March can be traced to a boost from resurgent spending by consumers on services such as travel and tourism. Especially strong growth of which is evident in Asia following the recent loosening of COVID-19 health precautions in mainland China, though a broader loosening of travel restrictions globally has also helped so far in 2023 compared to prior years. The concern is that, like prior spending waves following loosened COVID-19 restrictions in 2021 and 2022, this latest fillip to growth could prove short-lived.

—Read the article from S&P Global Market Intelligence

Access more insights on the global economy >

Capital Markets

This Week In Credit: Earnings Season In The Spotlight (April 17, 2023)

A near-term Fed pivot could be on ice again as recent economic and survey data suggest inflation has yet to cool down sufficiently. Benchmark yields jumped back up last week as markets grew more certain of near-term rate hikes. With limited data releases this week, attention will likely turn to the Q1 2023 earnings season. As well as gaining a clearer view of the impact of recent turmoil on financial institutions, S&P Global Ratings should also be able to gauge current cost inflation dynamics across nonfinancial corporates.

—Read the report from S&P Global Ratings

Access more insights on capital markets >

Global Trade

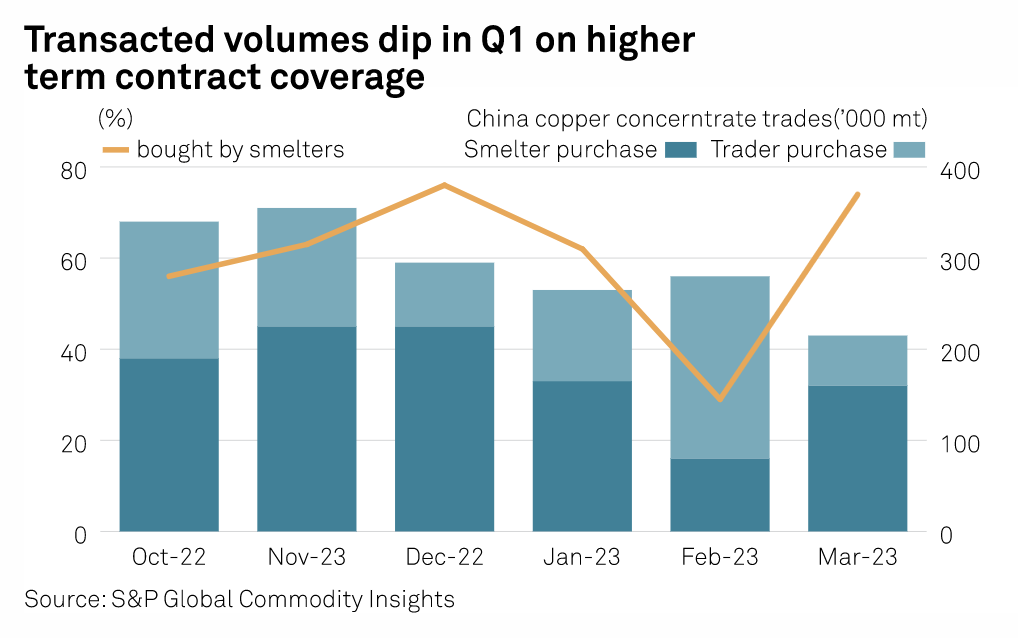

Recovery In Sight For Asian Copper Concentrate TC/RCs In Q2, But Uncertainties Linger

Spot copper treatment and refining charges (TC/RCs) are expected to recover in Q2, on easing supply disruptions and seasonal maintenance at several Chinese smelters, despite the potential Indonesian export ban and political instability in Peru. Multiple supply disruptions pushed down spot TC/RCs in the first quarter.

—Read the article from S&P Global Commodity Insights

Access more insights on global trade >

Sustainability

Listen: Why Latest IPCC Report Includes Urgent Warning On Net Zero

In March 2023, the UN's Intergovernmental Panel on Climate Change (IPCC) released a synthesis report warning that the world needs to act fast to reduce emissions. The synthesis report is likely to be the go-to document for many stakeholders setting their climate policies and plans over the next several years. This episode of ESG Insider features two authors of the IPCC report.

—Listen and subscribe to ESG Insider, a podcast from S&P Global Sustainable1

Access more insights on sustainability >

Energy & Commodities

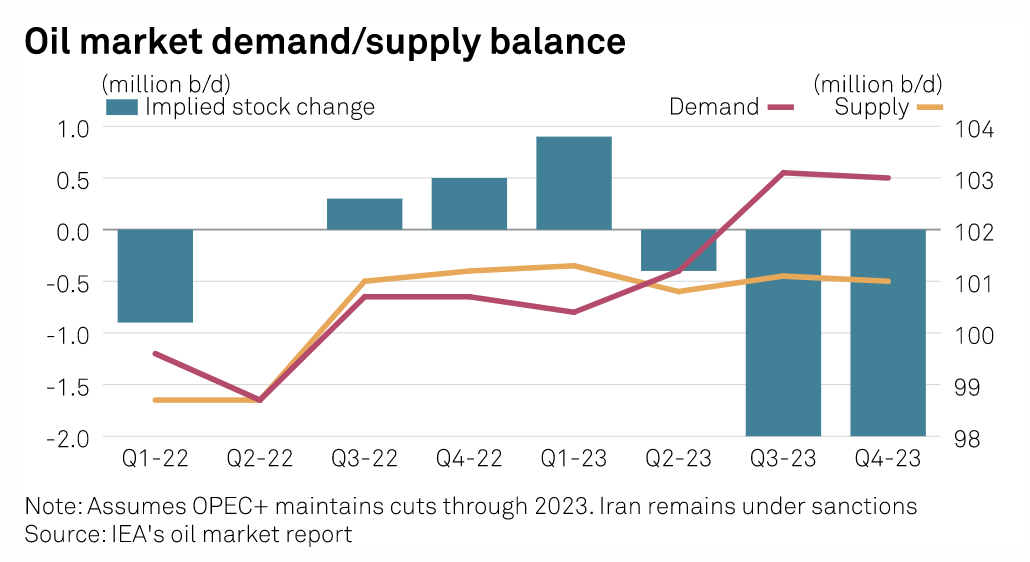

OPEC+ Output Cuts To Deepen H2 Oil Supply Deficit, Risk Higher Prices: IEA

OPEC+'s recent announcement of new output cuts this year will deepen an expected supply deficit in the second half of the year and risks higher prices as China's economic rebound continues to drive growth, the International Energy Agency said April 14. OPEC+ on April 2 announced a surprise "precautionary move" to cut 1.16 million b/d of production this year from May, which has triggered a jump in oil prices to over $85/b from March lows of $70/b.

—Read the article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

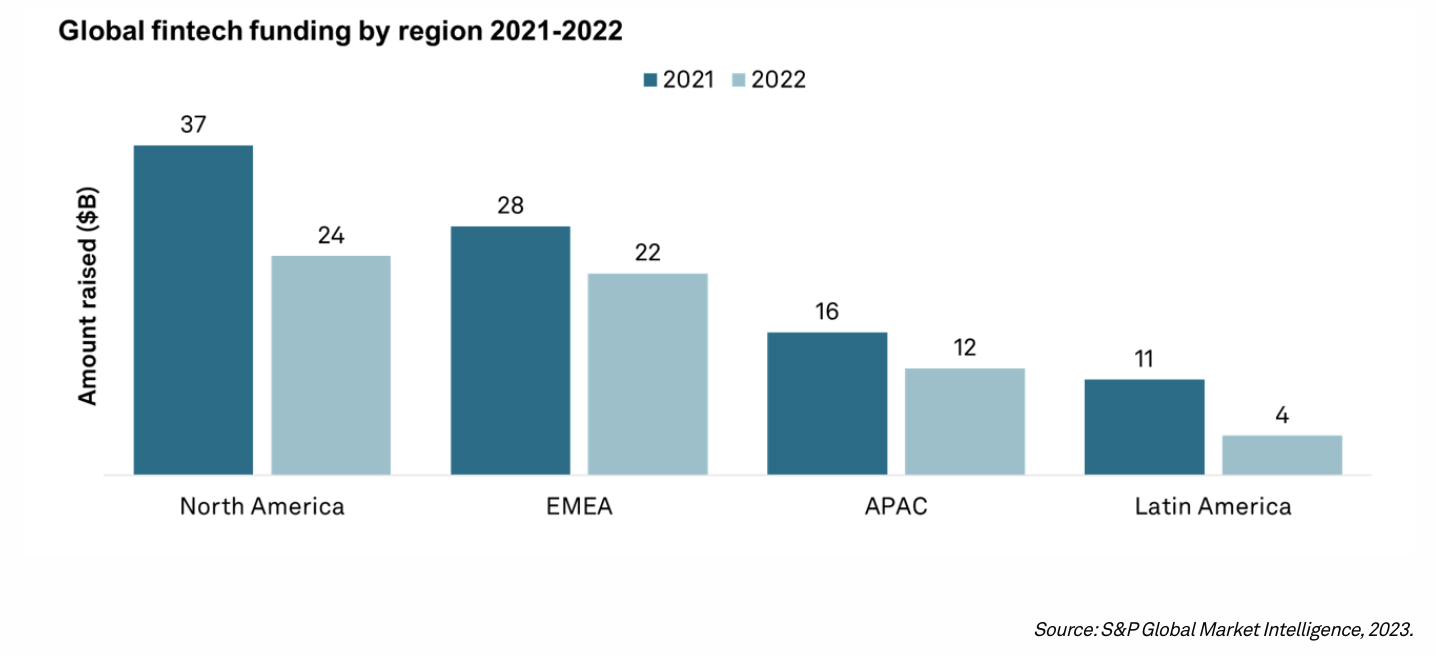

Global Fintech Funding Primed For Reset In 2023: Report

A broad-sweeping downturn in the technology sector led fintech funding to fall by a third globally to $63 billion in 2022, according to S&P Global Market Intelligence’s Global Fintech Funding Trends report. Fintech funding saw a massive deceleration in the last quarter of 2022, registering only 599 rounds for $8 billion, compared to nearly 1,000 rounds worth $26 billion in the year-ago period.

—Read the article from S&P Global Market Intelligence