Customer Experience Focus Can Improve Equity And Credit Performance

Published: September 20, 2021

By Sheryl Kingstone, Sudeep Kesh, Jeong Choi, Clayton Davis, William Watson, and Sundaram Iyer

Highlights

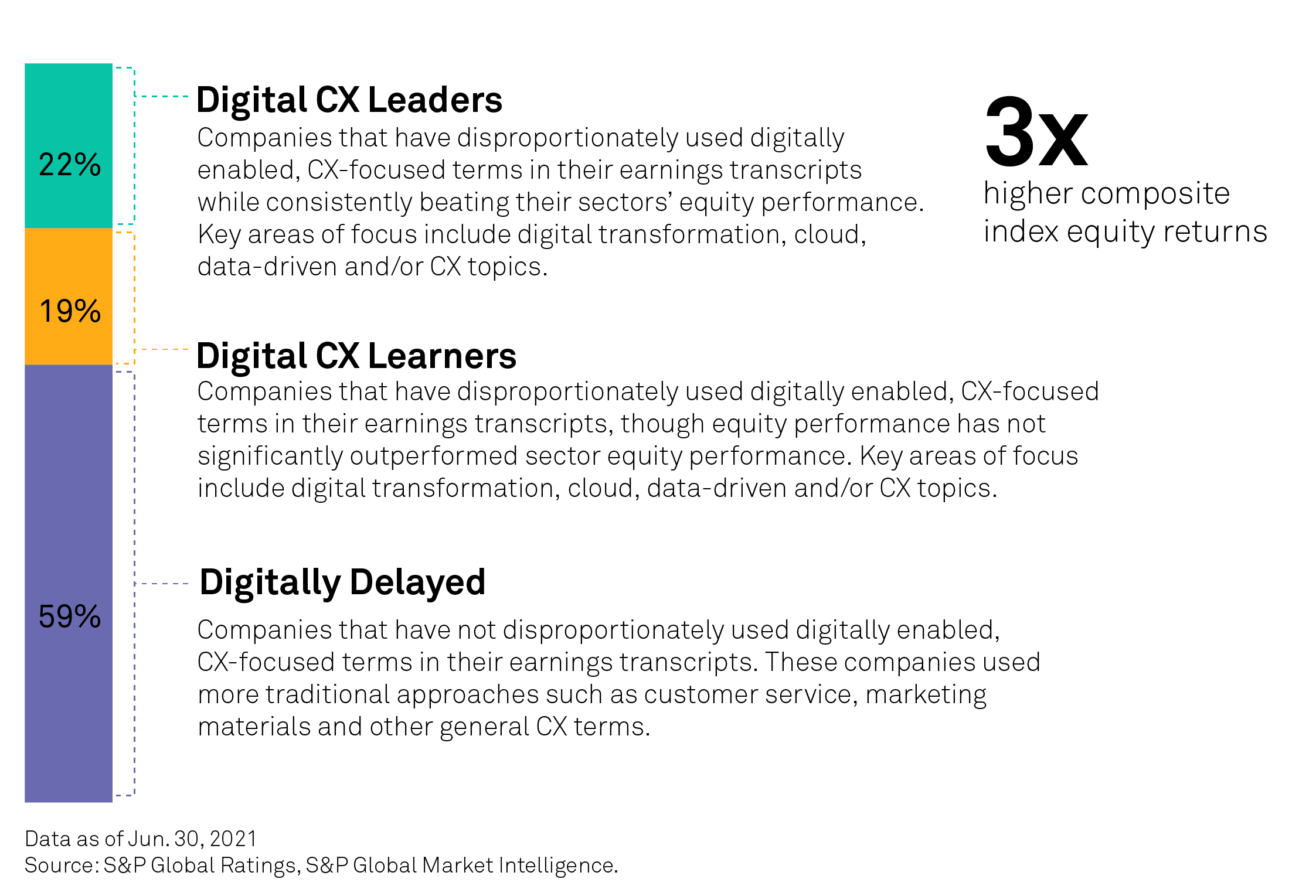

Of all companies using digital customer experience (CX) terms in their earnings transcripts, CX leaders and CX learners--as we define them in our study--have higher equity returns (using a composite index method) than their industry peers on average. Companies that use technology as a way of focusing on and adapting to their customers' needs have a clear advantage from the standpoint of investor appetite.

The top 22% of digital CX leaders have 2.7x higher average equity returns than their digitally delayed peers. The majority frequently and consistently use CX and service terms in earnings transcripts, in addition to digital transformation and machine learning terms.

Digital CX leaders generally see lower observed default rates during benign times (when macroeconomic shocks or periods of major market dislocation are absent) than the totality of global rated issuers. Of the two periods in the last decade that dispute this trend (2016 and 2020), oil and gas companies (2016 oil price crisis) and energy, brick-and-mortar retail, and travel companies (2020 COVID-19 pandemic) account for over three-quarters of defaults, whereas CX leaders generally show significantly lower default rates.

While the global portfolio as a whole narrowly beats CX leaders on the share of investment-grade credit ratings (51% versus 49%), when including the ‘BB’ category, we found three-quarters of CX leaders are rated ‘BB’ or higher, compared with 62% of their global peers (inclusive of CX leaders and their counterparts).

As companies invest more in technology, digital experiences for customers improve. As businesses continue to invest in their digital transformation to improve the customer experience, benchmarking their digital maturity is critical to business planning and growth.

Download the PDF

Companies that are using digitization as a way of focusing on and adapting to their customers' needs have a clear advantage from the standpoint of investor appetite. Indeed, CX leaders have a higher composite index equity return than their digitally delayed counterparts (see chart 1). Our data shows how the use of CX focus and technology investments affects companies' equity performance and creditworthiness across sectors.

Listen to a synopsis of this research, read by one of our lead authors.

Digital transformation is real, and it’s happening. Every business is becoming a digital business through the delivery of one or more of the following:

-

Innovative products, services, or business models;

-

Continuous improvement in business operations; and

-

Personalized experiences for customers, employees, and partners.

Since CX is a catalyst in many digital transformation projects, it is important to understand where businesses are making investments in new technologies to deliver differentiated and consistent CX. In technology terms, executing on business transformation demands new investments in more modern software and related technologies. This requires a well-planned approach to business and IT innovation and investing in new tactics to remain relevant in the eyes of customers.

This research is the first collaboration of its kind between S&P Global Ratings and 451 Research, a part of S&P Global Market Intelligence. We evaluated the credit ratings, market capitalization, and earnings transcripts of nearly 10,000 global issuers to determine trends and identify three categories among the companies we evaluated: digital CX leaders, digital CX learners, and digitally delayed companies (see chart 1).

Chart 1: Digital CX Leaders Produce Higher Composite Index Returns

CX Tech Investments Boost Equity And Credit Performance

We are witnessing a dramatic shift in the balance of power between many organizations and their customers across virtually all industries. Price and products are no longer enough; customers value experiences. Organizations can digitally transform their businesses by leveraging the latest applications, analytics, and infrastructure to provide customers with a differentiated experience that is not a luxury, but a necessity for survival.

The power of a digital transformation strategy lies in executive leadership determining its vision and objectives. Formal digital transformation strategies have accelerated over the past decade. According to a 2020 survey conducted by 451 Research1, 54% of businesses have formal strategies in place, up from 43% in 2019 and 29% in 2016. The results also show that 24% of businesses consider themselves early adopters of technology. Technology today can ensure that businesses meet changing customer expectations, but many businesses have a long way to go to ensure that vision meets reality.

Chart 2: Growth in Digital Transformation Strategies Create Digitally Driven Leaders

![]()

Digitally driven organizations are early adopters of technology and have formal digital transformation strategies (see chart 2). Growth in effective use of customer data, empowered by technologies such as CX management, and cloud and machine learning, will create a significant gap between digitally driven leaders versus digitally delayed when it comes to using technologies for strategic innovation.

While 2020 changed CX by accelerating the shift to digital, we stated long before the pandemic (and will continue to state long after) that experiences are the battleground for competitive differentiation. As we head toward a post-pandemic reality, businesses must prepare to address the shifting behaviors and preferences of empowered consumers not just online, but across the entire customer journey. What were once aspirational views of innovative digital experiences are now requirements for both business-to-consumer (B2C) and business-to-business (B2B) markets. B2B organizations face rising customer expectations for less friction and improved digital experiences, with 80% of businesses stating that they are likely to stop buying from a technology vendor as a result of a poor CX. This is accelerating digital transformation, including the need for more modern applications for front-line employees and customer self-service.

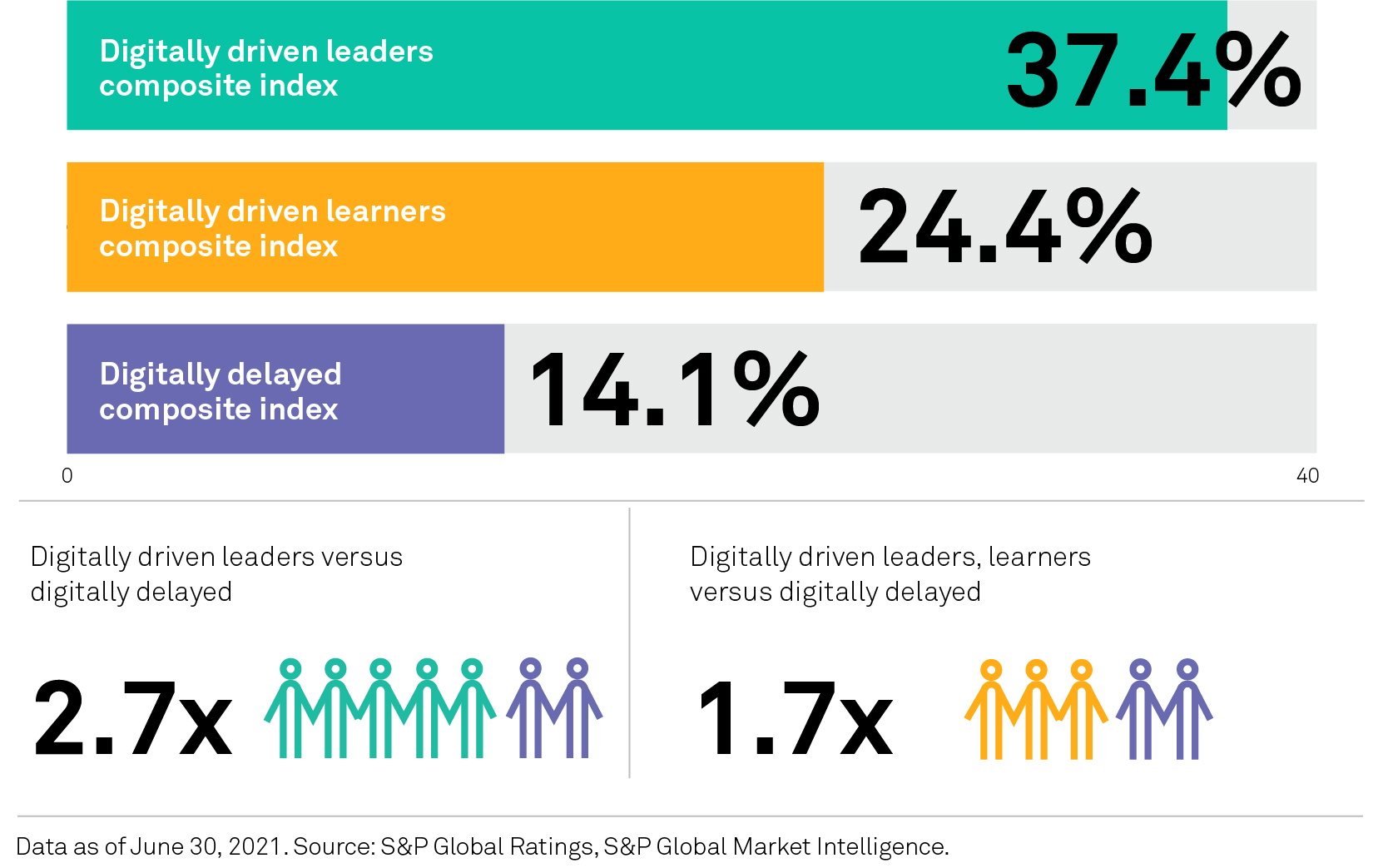

True Leaders Emerge: The Top Leaders Have Almost 3x Higher Equity Returns

A rising number of organizations are focusing on transforming their businesses to capitalize on long-term customer relationships that build brand loyalty. Digitally driven organizations have taken strides to invest in their digital transformation and adopt new technologies; we find that such differentiation makes for radically different performance across digitally driven and digitally delayed groups when comparing the composite index averages (see chart 3).

Chart 3: Comparing the Averages

Leaders Make Up Only One-Third of the $70 Trillion Market Cap

As the balance of power between organizations and customers shifts, businesses are strategically shifting their IT spend. Despite CX leaders making up just one-third of the $70 trillion in market capitalization of globally rated, public companies, the majority frequently and consistently use CX and service terms in addition to terms such as "digital transformation" and "machine learning" (see chart 4). Such concepts are illustrative of high-performing companies, and our analysis shows how such companies outperform their benchmark peers.

Chart 4: Overall Composition of CX Leaders

The utilization of specific words in earnings transcripts can paint a picture of where companies are focusing their time and resources relating to digital transformation and customer experience technology. By and large, consumer-facing sectors had relatively sizable utilization of experiential terms, including "digital experience," "digital transformation," and "customer experience." Since demand for the products and services in these sectors is more elastic than other durable, B2B, and less discretionary sectors, the adoption of CX strategies and digitization is vital to remaining competitive.

Beyond CX and service, the most common technology terms digital leaders used were "digital transformation," "cloud," and "machine learning." As businesses continue to invest in their digital transformation to improve CX, benchmarking their digital maturity is critical to business planning and growth. This involves assessing their use of:

-

Automation of customer-facing processes using data and intelligent automation, and

-

Modern application and cloud infrastructures.

The coronavirus pandemic has changed CX, altering strategic priorities and related technology spending trends. Specifically, the widespread economic and societal impacts have accelerated enterprises’ adoption of digital technologies to stay relevant to customers. To achieve growth, we believe businesses will need to not only invest in digital transformation, but also understand and benchmark their progress. The growth of data, along with demands for rich media content and regulatory compliance, are requiring new approaches to managing customer data and intelligence.

Digitally Driven CX Leaders Consistently Outperform On Median Equity Performance

In our study, we found that companies that are using digitization to focus on and adapt to their customers' needs have a clear advantage from the standpoint of investor appetite. Indeed, equity returns for digitally driven CX leaders were consistently higher over the last three years (see chart 5). Consistency can equate to stability as leaders focus on long-term, customer-centric initiatives (outside-in metrics) versus cost reduction and operational performance (inside-out).

Chart 5: Equity Performance Shows Consistent Results

Digitally Driven Leaders Similarly Show Strong Creditworthiness

Finally, the fixed income asset class show similar strength from the standpoint of creditworthiness. In fact, CX leaders have more stable creditworthiness than the global portfolio overall. While the global portfolio as a whole narrowly beats CX leaders on the share of investment-grade ratings (51% versus 49%), when including the ‘BB’ category, CX leaders are generally more stable than their broader peers. Indeed, three-quarters of CX leaders have credit ratings of at least ‘BB,’ compared with 62% of their global peers.

Why does this matter? Over the past 10 years, stability rates (the absence of both upgrades and downgrades) are at least 80% for companies in the ‘BB’ rating category and above, while companies rated in the ‘B’ and ‘CCC’ categories are less stable. This aspect is particularly important to fixed-income investors who, despite a thirst for yield, are often concerned with mitigating default risk--namely, the return of capital, in full and on time. From the borrower perspective, capital costs for fixed-income instruments are significantly more attractive, with spreads trading well below 300 basis points (bps) in these categories compared with over 600 bps for the ‘CCC’ category. Put another way, an investor holding a portfolio of CX leaders will have significantly less credit risk than will an investor holding a portfolio of the entire bond market--especially during times of market dislocation.

Chart 6: CX Leaders Have Better-Performing Credit Ratings

Addressing customers’ demand for new personalized experiences relies heavily on data-driven insight, intelligent automation, and digital platforms to build deeper connections, recommend next best actions and create more contextually driven interactions. As companies invest in algorithmic technologies and intelligent applications take over execution, that can free up resources--helping to lower capital and operational costs and preserve investor capital.

Indeed, digital CX leaders have lower observed default rates during benign times than do the totality of issuers on a global basis other than two periods in the last decade: 2016 and 2020. The uptick in defaults in 2016 was largely a result of a rapid decline in oil prices, causing record-high numbers of defaults and distressed exchanges. For both CX leaders and digitally delayed companies, oil prices were simply too low to support profitability and defaults amplified. In 2020, the rapid loss of confidence in the financial system during the fastest and sharpest decline in economic growth in recent history, caused by the combination of the COVID-19 pandemic and oil pricing pressure, caused a surge of defaults. Digitally enabled CX may have helped issuers diversify revenue streams, though rising defaults was inevitable given the rapid decline in revenue-generating prospects. While default rates of digital CX leaders even exceeded their broader, global peers, three-quarters of defaults were in just three industries: energy, brick-and-mortar retailing, and travel-related sectors.

Chart 7: Digital CX Leaders Have Lower Observed Default Rates

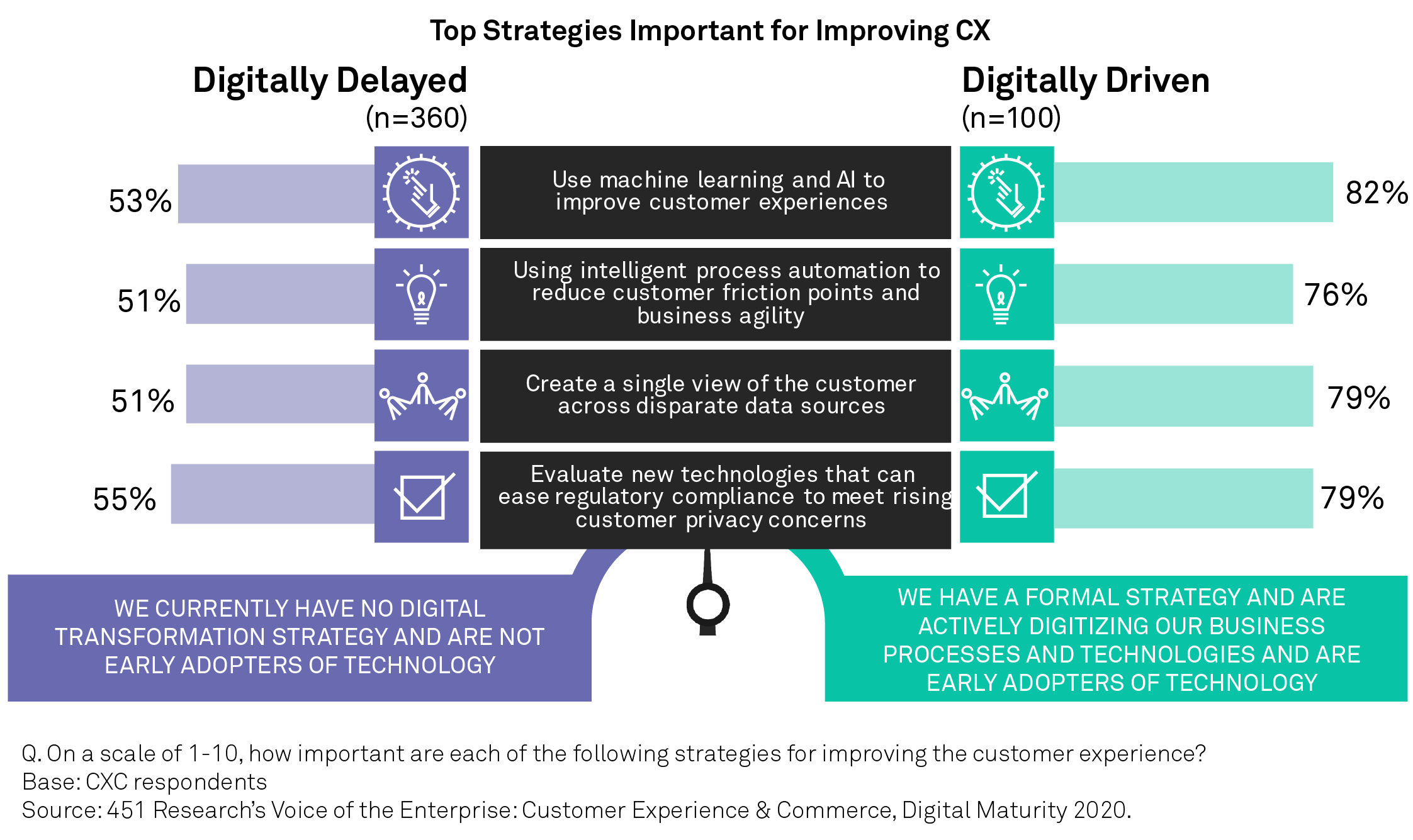

Why Are Digitally Driven CX Leaders Gaining a Competitive Edge?

The desire to capture and analyze new forms of data plays a powerful role in improving digital innovation. Businesses are investing in machine learning technologies, which help users see further and deeper into growing data sets to improve business decision-making. Users aren’t limited to what they discover themselves. Human exploration augmented by intelligent guidance from machine learning can be a powerful combination. The role of data, intelligence, and automation will also help digitally driven organizations to significantly outpace their digitally delayed counterparts. One of the greatest divides we consistently see between these two groups (a 29-percentage-point differential as of Q4 20202) is with "using machine learning and AI to improve CX"--a key differentiator in delivering exceptional CX.

Chart 8: AI Creates the Largest Wedge Between Digitally Driven and Digitally Delayed

CX technologies will remain essential for many businesses, from large enterprise providers to niche providers targeting small businesses or industry segments. According to a 451 Research survey, nearly 69% of digital leaders have already deployed a customer relationship management (CRM) application, while another 27% are considering a redeployment. For decades, businesses have sought a comprehensive picture of customer activity and behavior. Achieving this, and capitalizing on improvements to CX, usually involves dynamically maintaining a single repository of preferences and behaviors about each customer to personalize experiences.

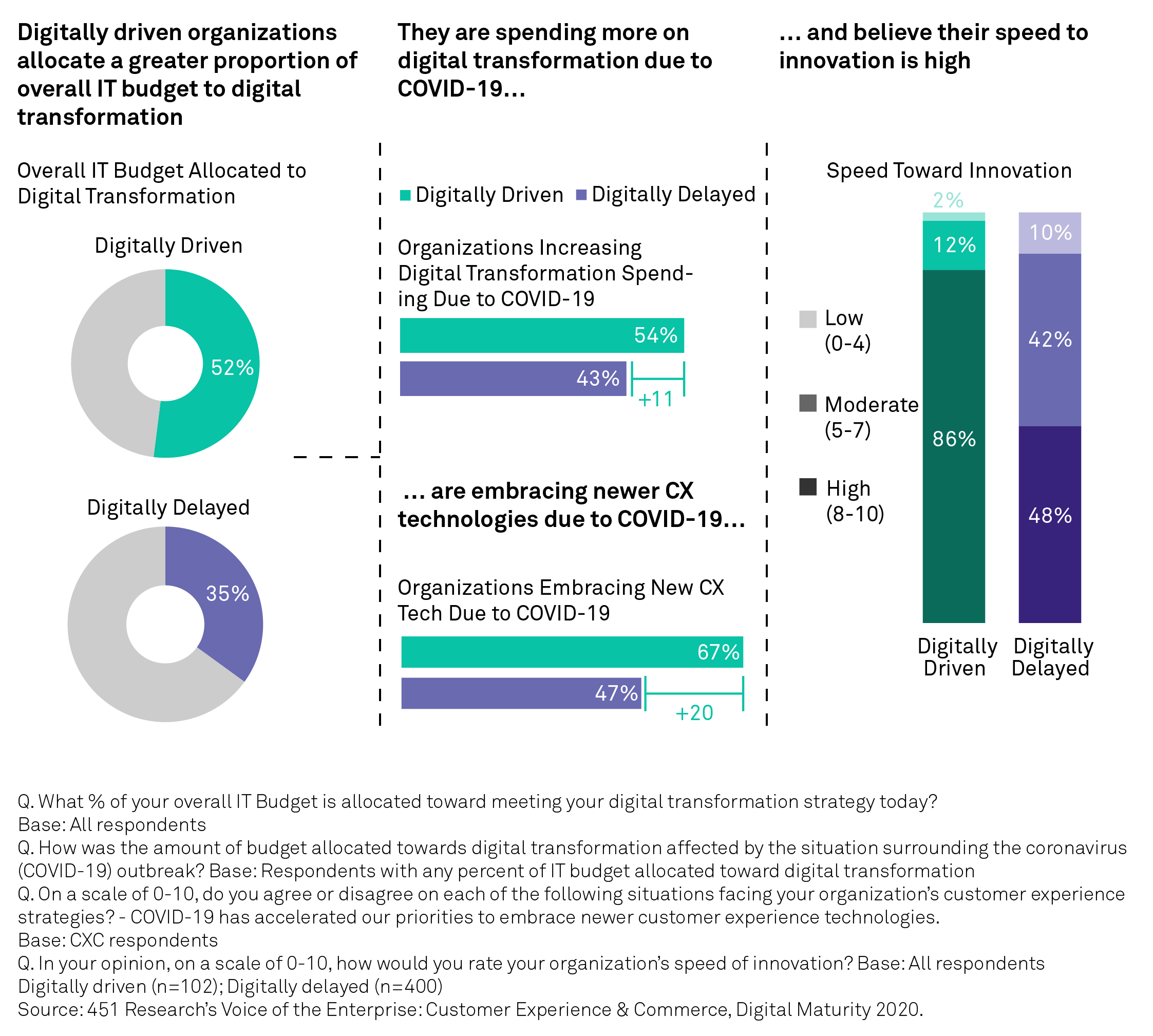

Digitally driven organizations are allocating a greater proportion of their IT budget to digital transformation (52%), and 54% state that they are spending more due to COVID-19 (see chart 9). The result is an acceleration of newer CX technologies as 67% of digitally driven companies say they are adapting in response to the new customer requirements. We expect that some industries where businesses were capable of pivoting to digital will maintain or increase technology spending to support innovation.

Chart 9: Spend and Speed to Innovation Is Higher for Digitally Driven Companies

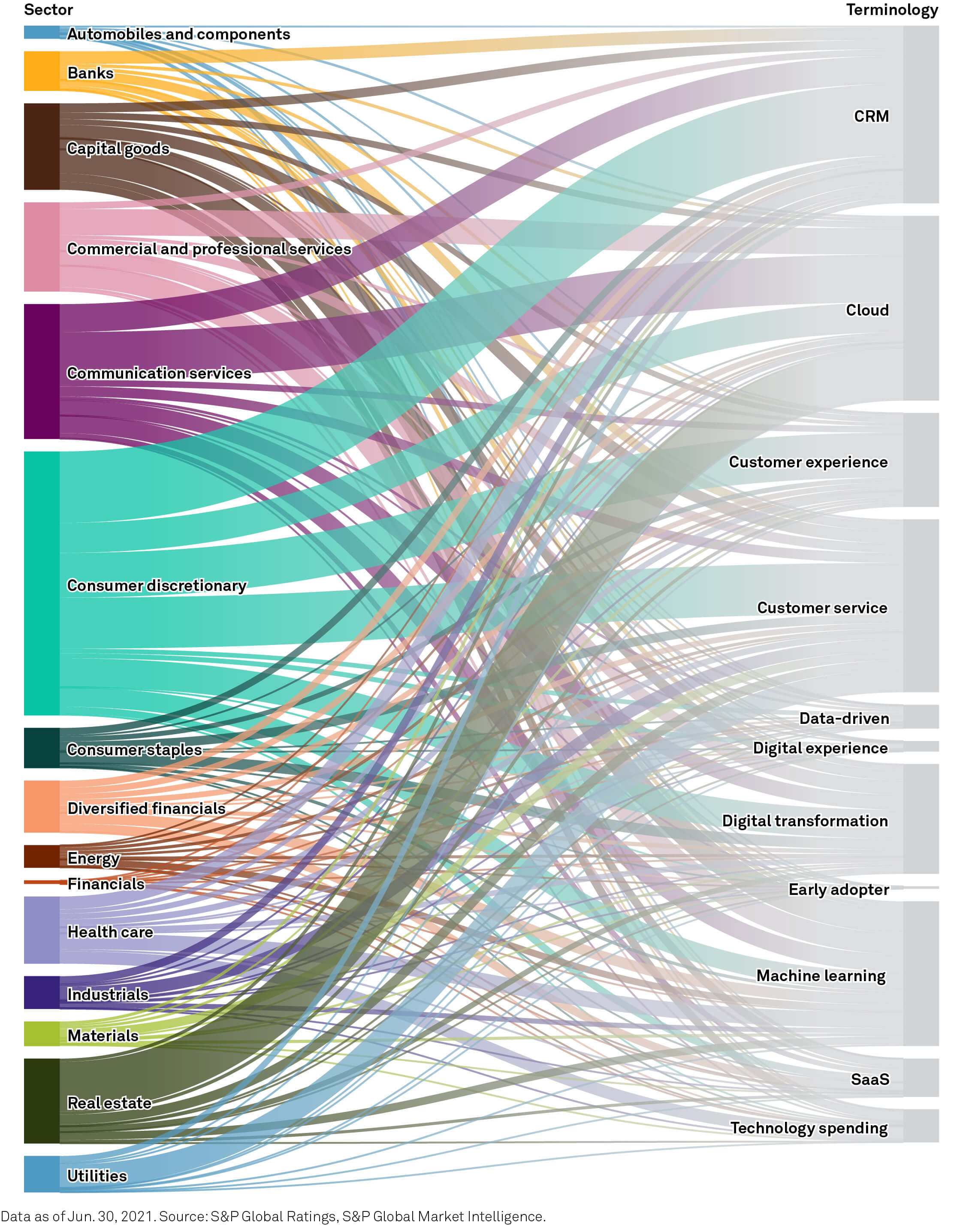

Sector Performance Differentiation Creates Different Class Of Leadership

Today’s experience economy is a powerful differentiator, but execution varies across sectors. For example, the consumer discretionary sector produced the largest number of overall companies meeting our CX leader qualifications based on CX terms appearing in earnings transcripts (see chart 10). It also showed the most usage of transformative technology and CX-focused business strategy. Machine learning and CRM systems, which power more adaptive, responsive customer engagements, saw a connection with sectors including capital goods, diversified financials, and consumer discretionary.

Chart 10: CX Terms Appearing in Company Earnings Transcripts, by Sector

While leaders generally beat the average year-over-year equity performance of their peers, certain industries, including diversified financials, industrials, automobiles and components, commercial and professional services, and banks, showed a larger disparity between equity performance of digitally enabled CX leaders and their digitally delayed peers. Sectors like utilities, energy, real estate, communications services, and consumer staples all had a significantly less pronounced disparity between leaders. Together, these trends underscore a certain point of elasticity: Companies in sectors rewarded by responsive changes in revenue generation, profitability, and customer retention--generally sectors that customers themselves will notice--saw better equity performance because this connection between CX strategy and return to equity investors is explicit.

For companies that are less elastic--meaning changes in customer preferences do not have a commensurate change in customer demand--CX strategies may have less of an impact on revenue and profitability and, subsequently, impede shareholder returns less. However, this does not signal that use of such strategy is not valuable to other industries--rather, the impact is simply elsewhere, namely in revenue retention and credit risk mitigation, which we address later in this report.

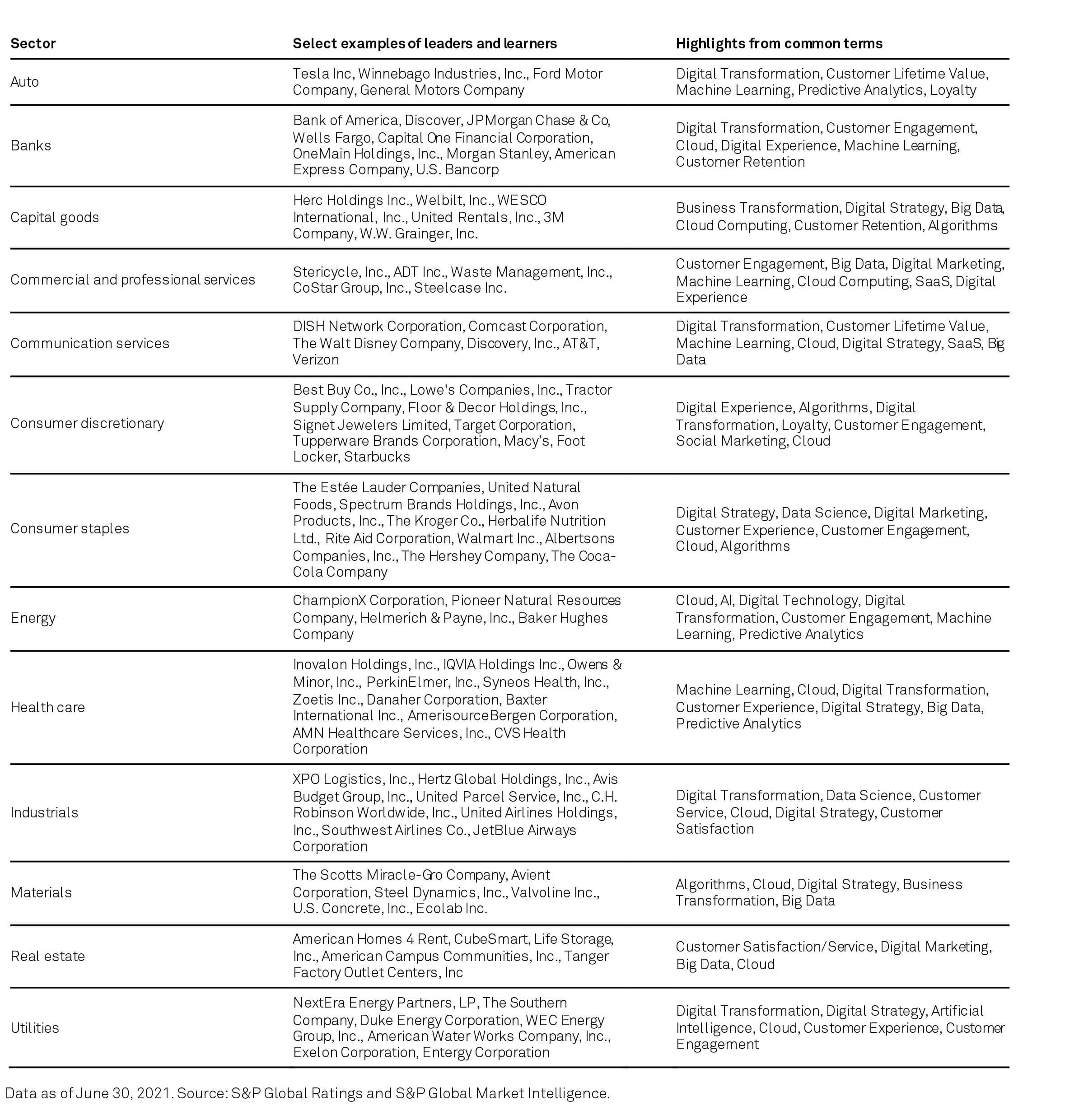

Chart 11: Crème de la Crème

In the automotive category, some of the leaders and learners include Tesla Inc., Winnebago Industries Inc., Ford Motor Co., and General Motors Co. (see chart 12). These organizations are focused on both CX action and related technology infrastructure. For example, Tesla not only has a strong loyalty base, but it also has implemented intelligent processes to connect with its customers. It uses data to tailor experiences and technology to completely personalize the experience--even embedded into the product experience itself.

Data from a recent 451 Research survey shows that the financial services industry is one of the strongest sectors, with 62% embracing formal digital transformation strategies. Bank of America Corp., Morgan Stanley, American Express Co., and U.S. Bancorp are some of the leaders that started digitization a few years back with projects such as digitizing the mortgage process, embracing digital assistants, and providing employees with useful insights from customer feedback. Leading institutions have made investments to empower both front-line employees and customers with digital technologies such as co-browsing, chat, and one-to-one interaction with the customer.

Chart 12: Sample CX Leaders And Learners

Even the capital goods market is embracing digital transformation and CX. United Rentals Inc. provides a completely digital experience on demand, available 24/7 for customer engagement and final rental of heavy equipment. Not surprisingly, one of the largest categories of leaders is consumer discretionary. Best Buy Co. Inc. began its digital transformation prior to the pandemic. The company enables omnichannel commerce with buy-online-pick-up-in-store/curbside, as well as augments its sales and service with video consultations and digital chats. Our research shows that $66.5 billion in sales in the U.S. alone in 2020 came from omnichannel experiences. Brands such as The Kroger Co., Avon Products Inc., 3M Co., and Floor & Decor Holdings Inc. are transforming their products and services to capitalize on digital commerce and customer engagement. Floor & Decor is enabling a connected customer strategy to fully integrate the in-store and online shopping experiences for information, design inspiration and convenience. Avon is reinventing the physical experience with digital, mobile-enabled interactions. Other beauty brands are digitizing the product experience with augmented and virtual reality. Real estate brand American Homes 4 Rent uses digital to connect with prospective renters. Businesses that were ramping up digital experiences prior to the pandemic were more capable of pivoting during the pandemic. Even Tractor Supply Co. ramped up innovation efforts already under way, such as initiatives to its improved e-commerce platform, enhanced mobile-enabled shopping, and expanded delivery options.

Some businesses that had already implemented omnichannel (such as buy-online-pick-up-in-store) quickly added curbside pickup as an option to support the growth of online experiences. Material manufacturer The Scotts Miracle-Gro Co. shifted its contact center to the cloud to maximize digital engagement and social channels. Valvoline Inc. uses technology to reach new customers when they are due for an oil change. It also uses first- and third-party data to ensure that marketing content is more relevant.

When comparing digitally driven CX leaders’ equity performance with their sectors’ equity performance more broadly, we can identify some of the outperformers: diversified financials, industrials, automobiles and components, and materials (see chart 13). Those sectors closer to the dashed line, such as capital goods, health care, financials, and consumer staples, had significant equity returns but were more on par with their sector averages (including both digitally driven and digitally delayed companies).

Chart 13: Equity Performance by Sector

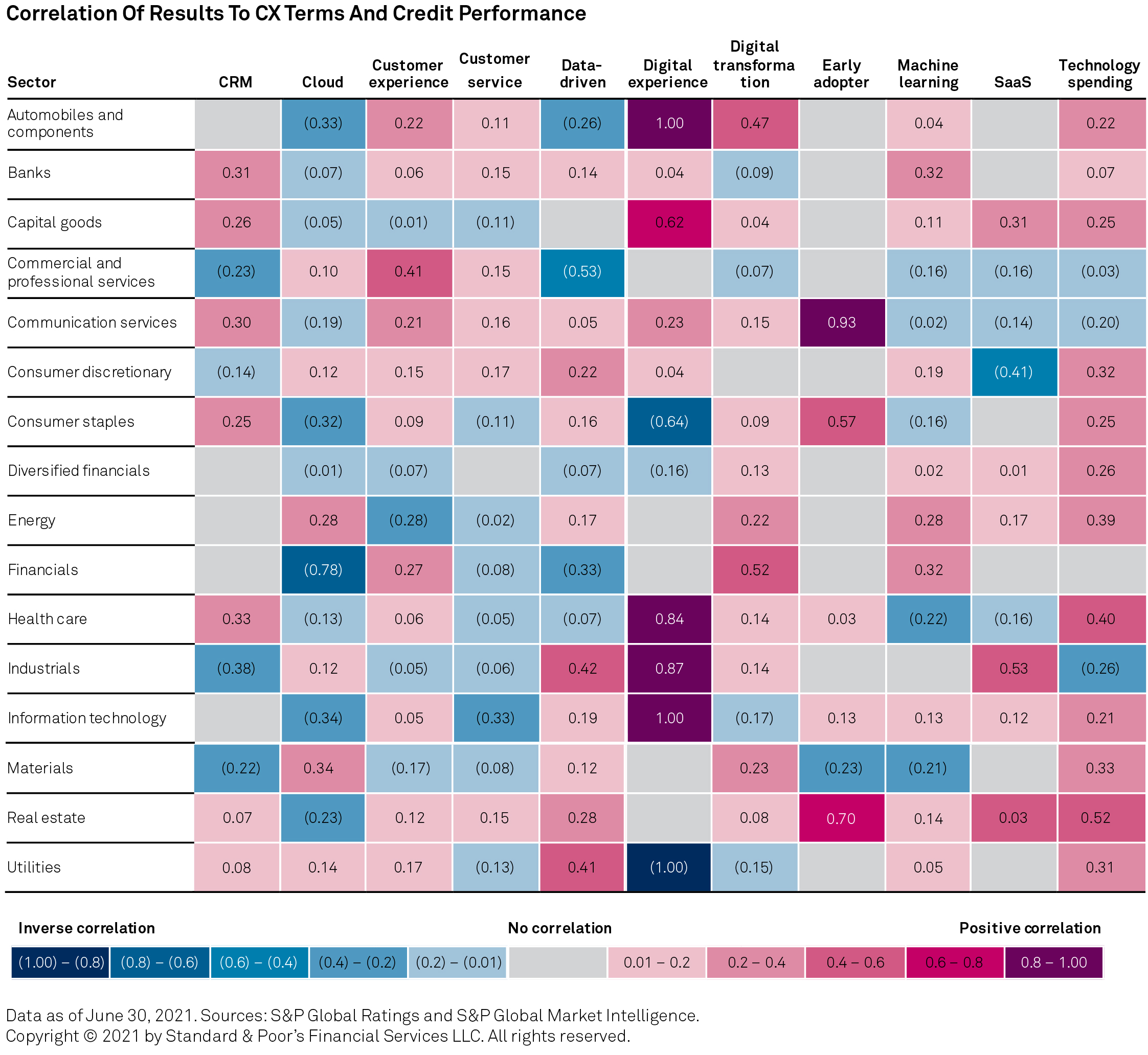

Digital Experience And Technology Spending Are Positively Correlated

Digital experiences and related technology investments define the way businesses engage with their partners, suppliers, customers, and prospects and are also leading to a more complex and intertwined system of vendors and service providers. Businesses are charged with navigating this market complexity to deploy new digital platforms and services that ensure data, insights, and key technologies connect consumers with the seamless experiences that they desire.

The ways sectors capitalize on data-driven initiatives vary. Consumer discretionary, consumer staples, and even industrial, for example, rely heavily on consumer behavior, product, and supply chain data to, among other things, enhance products and increase revenues.

The correlation of digital CX terms varies by sector as well as direction. For example, cloud has a fairly inverse correlation with most sectors’ credit performance--meaning there is a higher correlation with the use of cloud terms in earnings reports with lower ratings, which tend to be companies with higher leverage. However, a positive correlation exists with technology spending and higher credit ratings. This is illustrative of investments in the future, which protect companies’ creditworthiness in the form of sustained revenues.

Chart 14: Correlation of Results to CX Terms and Credit Performance

Becoming data-driven entails an organizational and cultural shift. The adoption of data-driven initiatives grew to 37% in 2020 from 25% in 2019, but it remains in the early stages.

Having a successful, data-driven organizational strategy is key to reaching CX digital maturity. The percent of digitally driven organizations with a formal data-driven strategy (71%) is now almost triple those that are digitally delayed. As we correlate digitally driven organizations with businesses that prioritize data-driven CX decisions in real time, we see that 63% of leaders say their business is capable of creating and delivering exceptional CX (e.g., a consistent and real-time CX across the customer journey), as shown in chart 15. These leaders are also more likely to focus on a modern single source of the truth for customers.

For businesses to effectively compete, it's essential to capture, analyze, and act on information, as well as recognize patterns, plan, and solve problems. The explosion in connectivity and intelligent devices--and the digital interfaces overlaying this information--is increasingly making it possible to create personalized experiences, augmented by real-time data.

Chart 15: Data-Driven, AI And Cloud Create CX Leaders

The alignment with a data-driven culture suggests that digitally driven organizations recognize the transformational value of data and the pivotal role it plays in enabling modern CX strategies and architectures. COVID-19 has also accelerated demand for more customer insight, especially as historical models may not provide the real-time assessment necessary for decision-making.

Conclusions And Implications

Businesses are doubling down on their CX strategies, with a noticeable shift in dollars being funneled into digital experiences. As organizations expand their CX budgets, many are looking to establish oversight of the behavioral changes that are redefining digital experiences. Innovations in cloud infrastructures, application architectures, and AI/machine learning are all enabling ways to digitally transform and deliver more immersive and frictionless customer experiences. The rapid acceleration of digitization, cloud, and data is underpinning innovation and CX performance.

As companies pivot their strategies toward digital experiences, they face increased competition and abrupt changes to brand loyalty. Fifty-nine percent of U.S. consumers in a recent 451 Research survey state that an unsatisfactory customer service interaction would significantly influence their likelihood to stop shopping with a preferred brand or retailer. Businesses must gather insight from volumes of unstructured data to better understand products, processes, demand, brand management, and employee engagement to strengthen relationships between customers and brands.

And as companies make digital investments, aligning the pace of innovation with major changes in the overall industry will be key to seeing a positive impact on equity and credit performance.

Methodology

This study considers nearly 10,000 global issuers rated by S&P Global Ratings, their credit ratings as of June 30, 2021, equity and market capitalization data from S&P Global Market Intelligence Capital IQ Pro (from the same time period), and earnings transcript data processed by a proprietary natural-language processing (NLP) algorithm. The earnings transcript algorithm evaluated the earnings transcripts of all companies with available transcripts, searching for the incidence, consistency and proximal location of terms related to digitally enabled CX.

Digitally enabled CX terms were then categorized into 11 topics to enable clarity when paired with equity performance and credit ratings. Further refinement was given to differentiate CX action topics, or those terms that are strategically linked directly to customer acquisition, management and service. Such topics include CRM, CX, customer service, data-driven, digital experience, digital transformation, early adopter and SaaS. Additionally, topics related to infrastructure (i.e., topics strategically linked to the infrastructure needed to enable direct-to-customer actions) included cloud and machine learning.

The digitally enabled CX terms data was then linked with company equity performance (period-over-period stock appreciation) for years 2018, 2019, 2020 and 2021 (as of June 30) as well as issuer-level credit ratings information as of June 30. To facilitate more generalized information and minimize idiosyncrasies in the data, the statistical median equity performance and credit ratings were compared for those companies that utilized digitally enabled CX terms versus companies more broadly.

To ensure that structural differences did not result in comparative differences, the market capitalizations of those companies using digitally enabled CX terms were compared against globally rated, public companies. The results were largely comparable though certain industries did highlight certain biases, as described in the Sector Performance Differentiation section of this publication.

Finally, we categorized results into groups for comparability. All companies across sectors whose primary business was affiliated with technology disruption or those companies whose digitally enabled CX was tantamount to their business strategy were eliminated. Examples of such cases are real estate investment trusts (REITs) whose real estate portfolio is entirely comprised of datacenters, enabling cloud computing, data storage and digitization. Of these, we further cataloged companies into three groups: digital leaders, digital learners and digitally delayed companies.

Digital leaders are companies that utilized the largest and most consistent digitally enabled CX terms in their earnings transcripts. Digital learners are companies that used digitally enabled CX terms in their earnings transcripts but with less

significance than their digital leader peers. Digitally delayed companies are those that did not use digitally enabled CX terms in their earnings transcripts.

While software and services and technology hardware and equipment had a sizable share of the utilization of cloud and SaaS terms in their earnings transcripts, the sector was excluded from this analysis because the majority of key terms were used in the delivery of the products and services used by other sectors, such as cloud infrastructure and related application software.

This report also contains data from the following surveys conducted by 451 Research, a part of S&P Global Market Intelligence:

-

Voice of the Enterprise: Customer Experience & Commerce, Digital Maturity 2020 -- This web-based survey was fielded in October 2020 among approximately 500 IT and line-of-business decision-makers worldwide.

-

Voice of the Enterprise: Customer Experience & Commerce, Vendor Evaluations 2020 -- This web-based survey was fielded in from July through September 2020 among approximately 1,570 customer experience technology decision-makers and influencers primarily based in North America.

-

Voice of the Enterprise: Customer Experience & Commerce, Organizational Dynamics & Budgets 2020 -- This web-based survey was fielded in January 2020 among approximately 1,000 IT and line-of-business decision-makers worldwide.

-

Voice of the Enterprise: Customer Experience & Commerce, Organizational Dynamics and Budgets 2021 -- This web-based survey was fielded in January 2021 among approximately 7,000 IT and line-of-business decision-makers worldwide.

-

Voice of the Connected User Landscape: Connected Customer (Consumer Representative), Quantifying the Customer Experience 2020 -- This web-based survey was fielded in July 2020 among approximately 5,000 U.S. online consumers who are 18 years of age or older.

1 451 Research’s Voice of the Enterprise: Customer Experience & Commerce, Digital Maturity 2020.

2 Ibid

3 451 Research’s Voice of the Enterprise: Customer Experience & Commerce, Vendor Evaluations 2020.

4 451 Research’s Voice of the Enterprise: Customer Experience & Commerce, Organizational Dynamics & Budgets 2020.

5 451 Research’s Voice of the Enterprise: Customer Experience & Commerce, Digital Maturity 2020.

6 451 Research’s Voice of the Connected User Landscape: Connected Customer (Consumer Representative), Quantifying the Customer Experience 2020.

Content Type

Location

Language