Panjiva's Q3 2020 Outlook: Heading into the great unknowns

Published: July 1, 2020

Highlights

This report is a three-part series providing a guide to developments we expect for global supply chains in Q3 2020. The impact of COVID-19 has been the defining factor for supply chains in the first half of the year. Recovery will mark the second.

Part 1: 4 Stages of COVID-19

In prior research, Panjiva identified four broad stages for corporate supply chains in tackling COVID-19. The first was supply chain disruptions centered on Asia and then more widely. The second was demand destruction in the large Western markets. The third is the staggered reopening of markets, while the fourth will involve long-term decisions around supply-chain structure.

Stage 1: Supply chains breakdown

The struggle with the first two stages of disruptions caused by COVID-19 has been a defining feature of corporate decision making in the second quarter. The late second quarter and start of third quarter were absorbed with the reopening process, though there should be an evolution away from stage three reopenings to stage four long-term planning decisions.

The major risk is slipping back to industrial closures should the current increase in cases, particularly in the U.S., become unmanageable. While the Trump administration has committed to not returning to earlier lockdowns:

(a) the decisions are made at the state level, as discussed in Panjiva's June 29 report;

(b) other countries may restrict operations anyway, as shown by the later-and-harsher lockdown in Mexico, which can crimp longer supply chains such as those in the autos sector, and;

(c) individual companies may choose to cut operations, disrupting supply chains on a more isolated basis as has been the case in meat processing.

The first two stages of the COVID-19 pandemic's impact can be clearly seen in global export data. Panjiva's analysis shows global exports across 37 countries plus the EU dropped by 8.4% in March before slumping 21.0% lower in April. In May, there was a small improvement as some Asian markets reopen to a 15.8% decline. Some caution is needed, though, as May is skewed upward by China's export decline being just 3.3% as earlier orders were finally completed and delivered, while data for the EU is not available until mid-July.

Part 2: Tough on China

This report is the second of three providing a guide to developments we expect for global supply chains in the third quarter of 2020. The whole outlook series is available here. The U.S.-China trade war has been somewhat on hold during the coronavirus pandemic. Its longer-term development will depend crucially on the result of the U.S. elections in November.

In November 2016, everything changed for global trade policy with the Trump administration bringing a more muscular, bilateral, tariff-driven approach to international trade policy when compared to previous administrations. The remainder of 2020 will reveal the trade policy positions of the next president of the United States — whether it is President Donald Trump's second term in office or the first of former Vice President Joe Biden.

In terms of Trump administration policy, there are unlikely to be many changes from the current course: a preference for bilateral trade deals focused on goods; a desire to reform multilateral institutions; a hawkish stance with regards to China; and a focus on the U.S. trade-in-goods deficit as a measure of trade policy success.

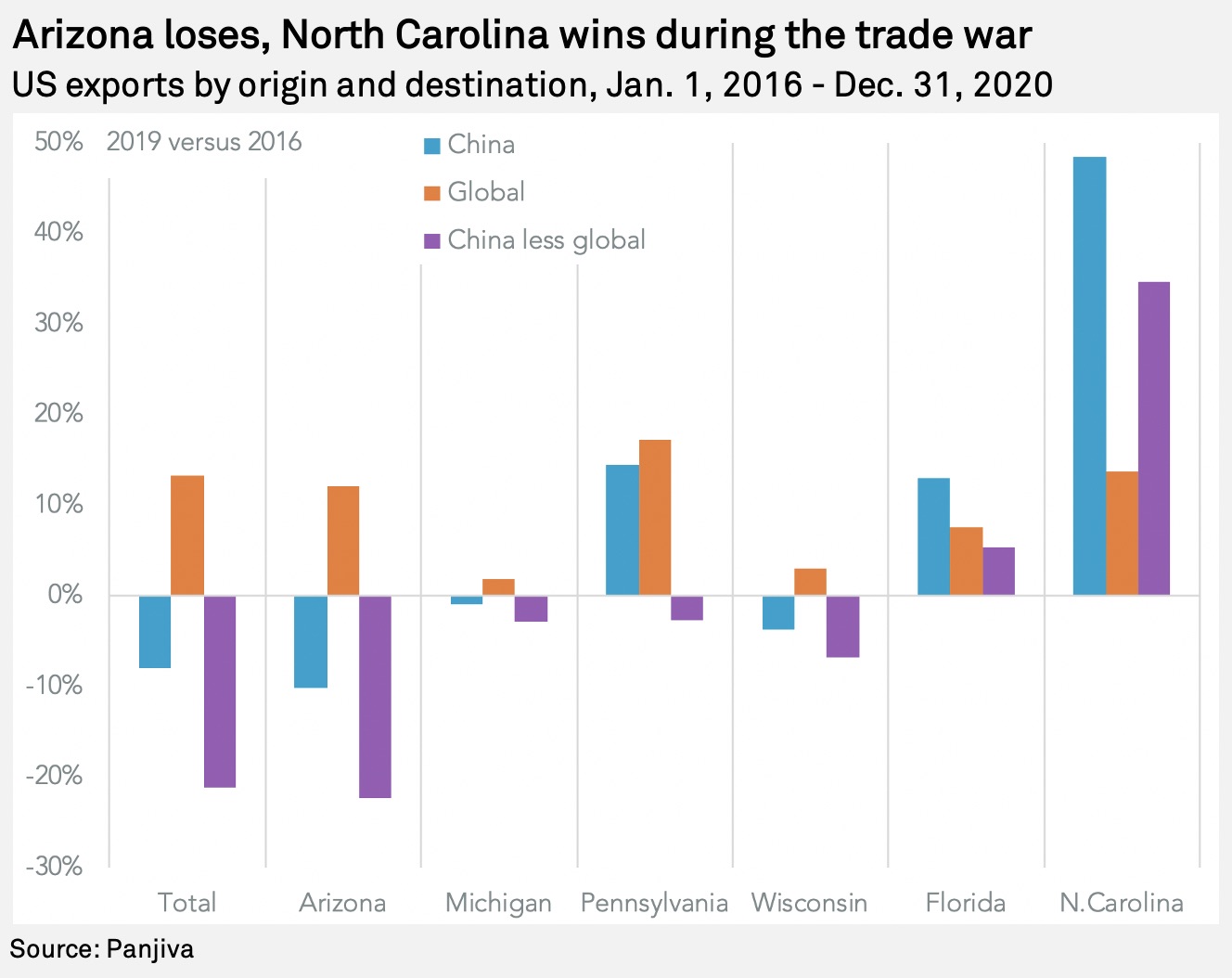

On the latter measure alone, the administration has failed in its objective of bringing the deficit down. Panjiva's data shows that in the 12 months to May 31 the U.S. trade-in-goods deficit reached $815 billion, compared to $737 billion in 2016, though it is at least below the $877 billion reached in 2018. Exports in the past 12 months have expanded by 5.8% compared to 2016 while imports expanded by 7.5%.

The latter includes a significant switch away from China, however, with imports from China in the 12 months to May 31 having fallen by 10.3%, while those from the rest of the world climbed 9.4% higher. As a consequence, the trade deficit with China specifically has fallen to $311.0 billion in the past 12 months from $346.8 billion in 2016.

Figures for the past three months are distorted by COVID-19 of course, so it may be unfair to judge performance until later in the year.

Part 3: Brush fires in global trade policy

This report is the third of three providing a guide to developments we expect for global supply chains in the third quarter of 2020. All three reports can be found here. Supply chain decision-makers' attention has been rightly focused on COVID-19 during the first half of 2020 while the U.S.-China trade war may dominate attention ahead of the U.S. elections. Yet, there are many other trade policy uncertainties that will affect conditions in the remainder of 2020 and in particular as we head into the peak shipping season.

EU-U.S. trade conflict: Carousel trouble now, digital and carbon tax issues later

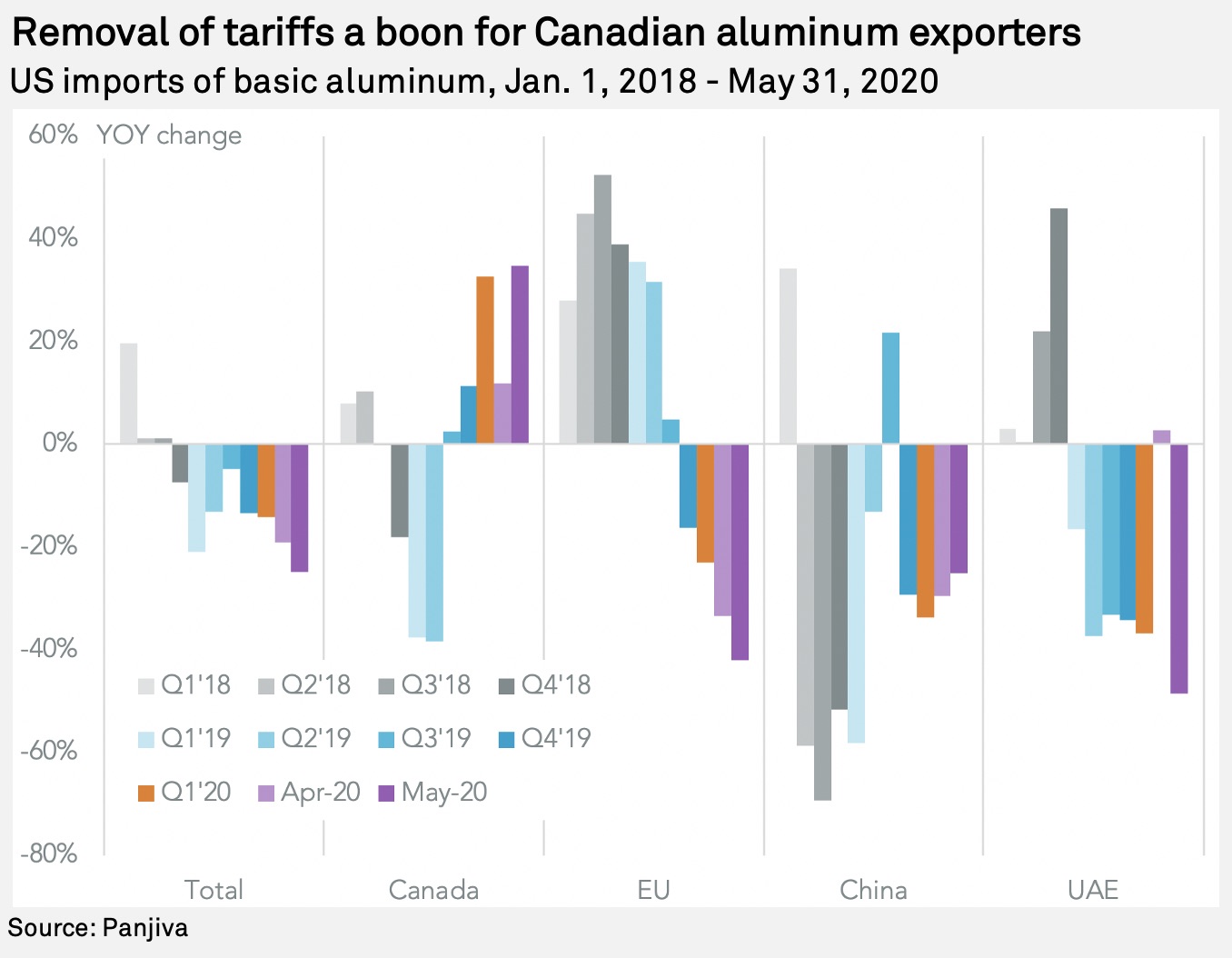

Relations between the U.S. and EU have deteriorated steadily over the past two years, in large part because of the EU's lack of willingness to engage in the narrow-scope trade talks that the Trump administration has called for, as well as the significant trade deficit held by the U.S. with the EU. Panjiva's data for U.S. merchandise exports and imports show the latter was worth $179.7 billion in the 12 months to May 31 compared to $147.6 billion in 2016. That has repeatedly drawn the attention of President Trump, who has repeatedly stated that Europe is "worse than China."

In the near term, the European Commissioner for trade, Phil Hogan, has recognized that they "could have a turbulent period in the context of the U.S. election," Bloomberg News reports, with a focus on the administration "threatening more tariffs on European products."

There are several tripwires, with U.S. adjustments to tariffs applied to EU imports in relation to EU subsidies for Airbus due to be finalized in August, as discussed in Panjiva's research of June 25. A second stage in that spat may not bubble up until the fourth quarter after a decision by the World Trade Organization to delay a ruling on an EU complaint about U.S. subsidies was delayed until September at the earliest, Reuters reports.

Content Type

Location

Language