S&P Global Platts — 24 Aug, 2020

The Reshaping of Sub-Saharan African Sugar Trade Flows

By Paola Luporini and Jonathan Dart

Fierce competition for the 1 million metric tons raw value Central African sugar market is altering trade flows within Sub-Saharan Africa.

The countries involved are landlocked sugar-deficit countries such as South Sudan, the Central African Republic, Chad, Niger and the Democratic Republic of Congo, which are highly dependent on flows across land borders.

S&P Global Platts Analytics estimates Sub-Saharan Africa as a whole could import 6.5 million mtrv of its 14.8 million mtrv consumption in the 2019-20 season (October-September).

SUB-SAHARAN AFRICA SUGAR CONSUMPTION

Center-South Brazil’s bumper sugar crop this season has meant more white sugar flows into Central Africa moving from west to east than in 2018-19 when India and Thailand were the main origins, meaning the bulk of flows were from east to west.

Within the east-west flows there has also been a change, with Sudan, the main sugar distribution hub in East Africa last year, giving ground to Somalia on routes into Central Africa. Platts Analytics estimates Somalia could re-export up to 680,000 mt this season, nearly three times more than last.

HORN OF AFRICA SUGAR EXPORTS

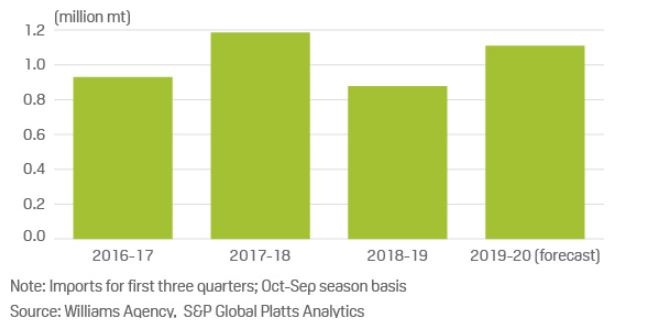

On the west-to-east route, CS Brazil is using gateway ports in Guinea and the Republic of Congo to move its sugar into Central Africa. West African white sugar imports from CS Brazil in 2019-20 so far are up 275,000 mt on the year at 1.2 million mt due to a wide open arbitrage.

WEST AFRICA WHITE SUGAR IMPORTS FROM CS BRAZIL

Go deeper: Request a copy of S&P Global Platts Analytics’ latest World Sugar Market Special Report

African competitors Uganda and Zimbabwe have also joined the fray for the Central African market. These two countries have to find new customers after Kenya banned all brown sugar imports.

Content Type

Segment

Language