S&P Dow Jones Indices — 26 Aug, 2020

Recalled to Life: The S&P SmallCap 600’s Persistent Outperformance after the Russell Reconstitution

By Berlinda Liu

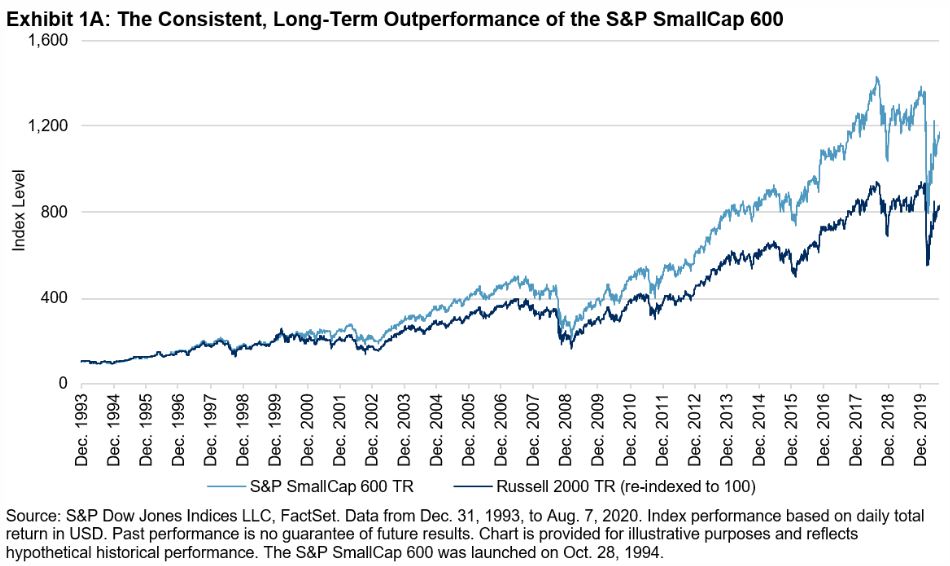

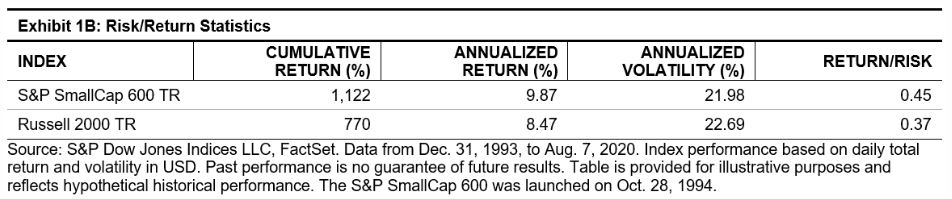

S&P DJI’s paper, A Tale of Two Benchmarks (first published in in 2009 and later updated in 2015 and 2019), showed that the S&P SmallCap 600® has structurally outperformed the Russell 2000, primarily benefiting from S&P DJI’s index inclusion criteria for profitability, liquidity, and public float. The paper also delves deeper into several secondary attribution analyses, including one of the most well-known market anomalies: the excess returns around the Russell reconstitution, which we’ll explore more deeply here.

As a brief review, index modifications to the S&P 500®, S&P MidCap 400®, and S&P SmallCap 600 are driven by changes in companies’ size, free float, corporate actions, new IPOs, and meeting inclusion criteria. These are constantly monitored by the Index Committee, and index changes are made throughout the year on an as-needed basis.1

In contrast, the Russell indices originally rebalanced on a quarterly basis, then on a semiannual basis, before moving to the current annual rebalance in 1989. In response to long-standing criticism regarding excessive turnover and significant price volatility on the rebalance day, starting in 2004, Russell published provisional indices, moved the day of the annual rebalance within June, and used NASDAQ’s (then-new) Closing Cross mechanism for determining effective prices.2 Later changes included quarterly IPO additions.

However, these changes failed to address the underlying inefficiency stemming from potential front-running of the rebalance trade that remains a several months-long process. Rather than disentangle the complex pre-inclusion effects, we’ll focus on what happens after the rebalance, as this is of most relevance to passive index portfolios.

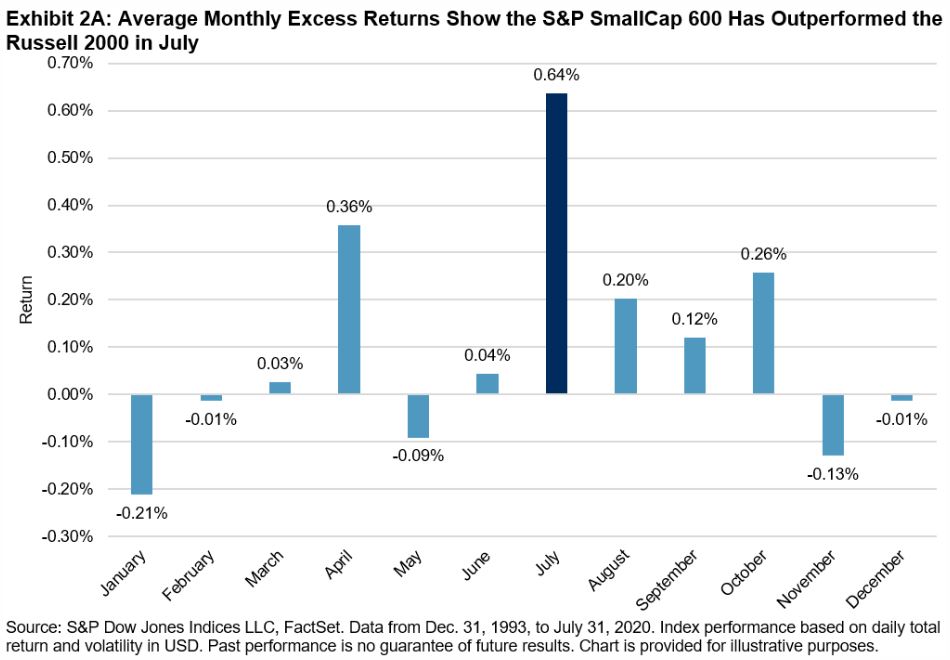

Exhibit 2A shows the differences in the average monthly returns of the S&P SmallCap 600 and the Russell 2000. The particularly notable average July outperformance of the S&P SmallCap 600 is 0.64% (t-stat = 2.92), as components entering the Russell 2000 at artificially elevated levels mean-revert. As a result, the S&P SmallCap 600 has outperformed the Russell 2000 in July for 19 of the 27 years observed (70.4%).

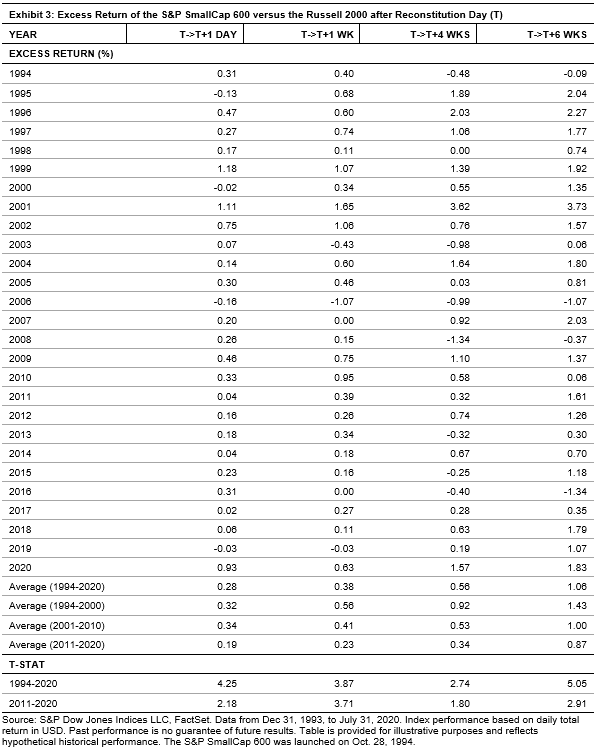

This reversion does not happen instantly on one trading day either, as would happen for a momentary closing imbalance. Just as the reconstitution is in reality a several months-long process, the unwind has a long tail. Exhibit 3 illustrates the excess returns measured from the rebalance date to selected intervals afterward. While the dislocations have been less extreme in recent years, especially closer to the reconstitution date, a conspicuous gap persisted and continued to widen even after one month.

While fundamental index construction factors have contributed significantly to the S&P SmallCap 600’s persistent outperformance versus the Russell 2000, the annual reconstitution continues to drive a secondary trading-driven inefficiency every July. Passive index portfolios often show little tracking error to the benchmark in the era of hyper-liquid markets and low commissions, but may still regularly pay these invisible costs to arbitragers based on their choice of index.

1 It is important to note that these indices (and the committee) seek to reflect the U.S. equity market in its entirety, including sector coverage, rather than mechanically select the largest companies in order. For more details, please refer to the S&P U.S. Indices Methodology.

2 Matturri, Alex, “2004 Russell Reconstitution Recap,” Northern Trust, July 2004.

Content Type

Location

Language