S&P Global Platts — 20 Apr, 2020

From the chaos of the coronavirus pandemic can come a new order for LNG markets

By Joseph Ira

Amid the coronavirus outbreak, the ephemeral nature of energy markets makes it difficult to offer certainty regarding our mainstays of forecasting: supply, demand, inventory, or price.

How much the new normal will be different from the old normal will not be revealed anytime soon, but in the case of global gas and LNG markets, it’s constructive to focus on structural problems that existed well before anyone ever heard of “social distancing.”

In gas markets, the problems heading into the coronavirus era were the same we will have as we leave it – the lack of demand growth and the problematic role of long-term contracts in the future of the gas business. Here’s where we can make lemonade out of lemons and create opportunity out of adversity.

As we speak, force majeure clauses are being invoked throughout the entire LNG value chain. Buyers are postponing or cancelling contracts, and producers are doing the same with the building of new liquefaction capacity. Whether or not these invocations are legally valid is not the issue. What matters is that the dispute can be used as leverage for how gas will be priced in the future.

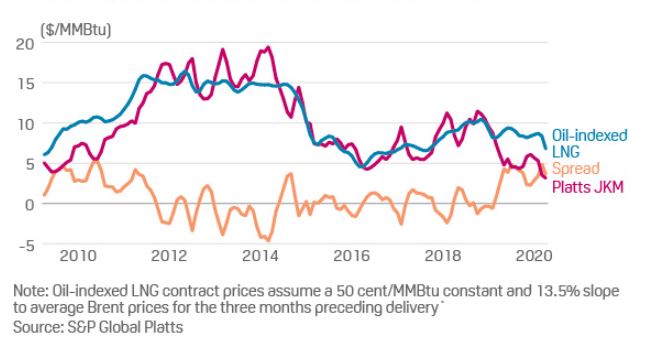

One thing the coronavirus has revealed is that using oil indexation for gas pricing is just as dysfunctional on the way down as it is on the way up. Movements in oil markets do not reflect global gas balances in any way.

OIL INDEXATION IGNORES GLOBAL GAS BALANCES

If anything, oil and gas have an inverse price relationship now that US LNG production has become a key marginal supplier to the market. Therefore, the price of oil-indexed pipeline gas or LNG bears no resemblance to the present or the future – only the past. Demand losses are vastly different between two commodities that barely intersect at the point of consumption.

Transformational moment

The opportunity is at hand for both buyers and sellers to have a moment of clarity on the flawed nature of their existing oil-indexed contracts, in order to create a transformational moment for the gas and LNG business.

Two thirds of all existing long-term LNG contracts will be expiring by 2027. At present, sellers are having trouble coaxing buyers into re-signing them and, if anything, the recent force majeures by Chinese and Indian buyers will have only made this harder.

The situation is not dissimilar to 2009, when long-term oil indexed pipeline contracts in Europe began to falter during the recession. In Europe, the solutions to this problem were massive and wide ranging. Some redesigned deals traded less contract volume liftings in the prompt for gas contract extensions on the back. Other deals shifted to spot indexation entirely, but kept the volume and length of the contract in place. Finally, a plethora of hybrid deals emerged that included both oil and spot gas indexation with shorter contract lengths, or more frequent price reopeners.

What made sense then does not make as much sense this time around. In 2020, we have well-functioning spot gas markets around the world that can act as a basis for spot gas indexation of long-term contracts. Transforming long-term contracts from oil to spot indexation can and will take many forms. Reasonable deals could be structured on a prompt, lagged, or forward curve basis using spot gas prices. The smart play would be to use this period of transformation to avoid force majeures, extend contract lengths, re-sign old deals, or – dare we say – sign new deals.

The issue for buyers is not necessarily making the long-term commitment, as long as both the price is right and the flexibility is in place to trade out unwanted volumes. It would also help to have lower levels of downward quantity tolerance on monthly nominations.

Sellers will need to treat these contracts as more of a partnership than an offtake agreement. Linking pipeline gas or LNG to a benchmark that reflects the value of the product will enable the parties to avoid the kind of disputes we now encounter. Spot indexation will help reduce contract renegotiations and the need for price reviews by cutting down on oil/gas price distortions. Contracted parties will see their positions as less penalized by price movements if the spot market is driving value and not another commodity such as oil, whose volatility can be driven by entirely alien market forces.

Go deeper: Learn more about S&P Global Platts Analytics

Sellers will continue to struggle with the issue of cost. Despite the incredible work being done by upstart developers such as Tellurian and Venture Global LNG, the capital outlay remains a formidable barrier to entry for projects requiring debt to finance. These projects cannot go forward without deals in place. As for the majors and national oil companies, moving to spot indexation on long-term contracts would mirror changes made over the last 40 years in the oil business. Term contracts in oil are not particularly long, but they do utilize well known spot indices such as Dated Brent or WTI.

LNG contracts will play a role in the future of the gas business, but their length needs to be tied to the reality of the present. This means more flexibility in terms of volumes and more capability to hedge against unforeseen risks, such as a global pandemic. The European spot market did indeed exist in as meaningful a way before the 2009 recession, but it really hit the mainstream once contract terms deteriorated and liquidity improved along the forward curves of NBP and TTF. We expect the same to be true for Platts JKM in the months and years ahead.

Spot indexation is the best method for bridging this divide, so we can finally retire a connection to oil markets that served the birth of LNG well, but no longer provides relevance during this next stage of development.