S&P Global — 26 Apr, 2021

Daily Update: April 26, 2021

By S&P Global

Subscribe on LinkedIn to be notified of each new Daily Update—a curated selection of essential intelligence on financial markets and the global economy from S&P Global.

As the global community aims to accelerate decarbonization, some industries are set to benefit sooner than others from shift to the hydrogen economy.

Because it already maintains much of the infrastructure needed to produce hydrogen, the industrial gas sector will be one of the first to fully adopt hydrogen over the next two decades—closely followed by oil refining, chemical, and fertilizer industries, according to new S&P Global Ratings research. This shift will be dependent on leading industrial gas players increasing their investments in blue and green hydrogen facilities, and represents a critical opportunity to strengthen revenue and earnings over the long-term.

Utilities may prioritize hydrogen for electricity storage after 2030, depending on what portion of power output renewables ultimately account, according to S&P Global Ratings. Electric vehicles, however, may not see the same opportunities this decade and steel producers have a long way to go.

Economies are eyeing hydrogen as a bridge fuel to power their energy transitions from fossil fuel generation to renewable sources. While the majority of hydrogen currently in production is generated from fossil fuels—most commonly grey hydrogen made from natural gas—market participants are focusing their technological development largely on blue and green hydrogen, created from natural gas through carbon capture and renewable energy, to drive emissions-reduction efforts. Corporates slated more than $2.5 trillion in investment in hydrogen through 2050, according to the Hydrogen Council, a CEO-led initiative of companies working to develop hydrogen for the energy transition.

Hydrogen’s current standing as more expensive to produce than natural gas has stymied its democratization. But experts believe the costliness of the equipment needed for production and the price of the energy itself will decrease in the coming years and thus remove barriers to entry. The first large-scale hydrogen products currently in planning are expected to launch by 2030.

“The competitiveness of green hydrogen compared with grey hydrogen depends on cost reduction and scaling of production technology. But CO2 pricing also plays a decisive role. The higher the CO2 price for grey hydrogen, the faster green hydrogen becomes a more lucrative option,” S&P Global Ratings said. “Closing the cost gap isn't achievable yet. However, we think a steep decline in green hydrogen costs is possible by 2030 through three channels: the levelized cost of energy for renewable power (estimated to account for 50%-60% of the total cost), capital investment costs of electrolysis plants (30%-40% of total costs), and capacity factors.”

Manufacturers of industrial-scale renewable power generation equipment and engineering groups offering green energy and electrolysis technology-related solutions and services are likely to benefit most from green hydrogen over the long-term, according to S&P Global Ratings. The clean fuel option could disrupt the fertilizer industry and diminish its emissions by 2030 if the industry makes efforts to evolve; improves its widespread operating conditions; is supported by positive regional regulatory frameworks; collaborates across its value chain; and has access to lower green ammonia production costs.

Overall, “H2 adoption on a wider scale will require different technologies, for green (fueled by renewables) and blue (with CO2 capture and storage). Green H2 production costs are likely to drop, but not before 2030, rivalling grey hydrogen manufacturing costs over time,” S&P Global Ratings said in its report. “Whether clean H2 will be widely adopted over the next two decades therefore hinges on supportive net zero policies, a steep decline in production costs from electrolysis, and ample renewables.”

Today is Monday, April 26, 2021 and here is today’s essential intelligence.

The Credit Cycle

Listen: The Essential Podcast, Episode 36: Winter is Coming, or Perhaps Not — Stimulus and the Risk of U.S. Inflation

As the outlook for the economic recovery from the COVID-19 crisis brightens, market participants are closely watching the shape and speed of the rebound. While many are concerned about the risk of rapidly rising inflation as the Treasury yield curve steepens, commodity prices surge worldwide, and stimulus money fills U.S. consumers’ pockets, such fears may be overblown. S&P Global Ratings Global Chief Economist Paul Gruenwald joins the Essential Podcast to discuss the risk of unanchored inflation and benefits of orderly reflation in the wake of the U.S.’s $1.9 trillion fiscal stimulus package and proposed $2 trillion infrastructure package.

—Listen and subscribe to the Essential Podcast, from S&P Global

Default, Transition, and Recovery: Four U.S. Defaults Push 2021 Global Tally To 32

At this point in 2020, 2019, and 2018, global corporate defaults totaled 40, 42, and 31, respectively. By region, the U.S. is leading the default tally, with 20 out of 32 defaults in 2021, followed by Europe with eight. Among the U.S. defaults, oil and gas leads the tally, with four, followed by the retail and restaurants, and media and entertainment sectors, with three each.

—Read the full report from S&P Global Ratings

Banking Sector Under Pressure

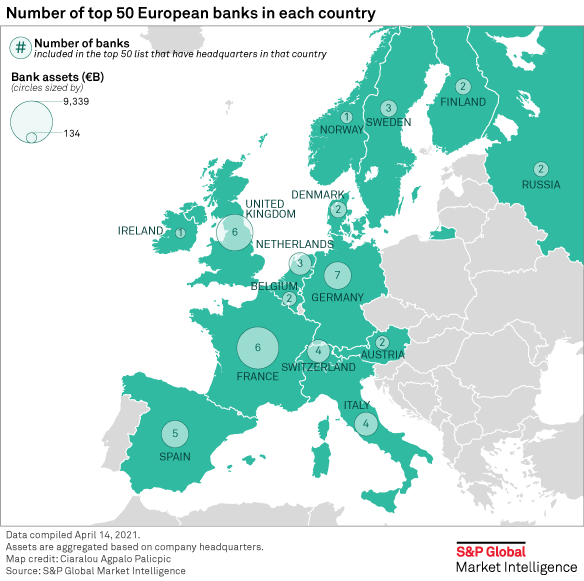

Europe's 50 Largest Banks By Assets, 2021

BNP Paribas SA overtook U.K.-based HSBC Holdings PLC as Europe's biggest lender by assets in a year marked by market turbulence caused by the coronavirus pandemic, according to S&P Global Market Intelligence.

—Read the full article from S&P Global Market Intelligence

APAC's 50 Largest Banks By Assets, 2021

Banks from China and Japan secured their positions as the largest lenders in Asia-Pacific by total assets in 2021, driven by loan or investment growth amid stronger economic recovery compared with other major markets since the pandemic.

—Read the full article from S&P Global Market Intelligence

The World's 100 Largest Banks, 2021

In a year marked by the COVID-19 pandemic, the largest Chinese financial institutions maintained their positions as the world's biggest banks by assets, S&P Global Market Intelligence's annual global bank ranking shows.

—Read the full article from S&P Global Market Intelligence

Technology & Media

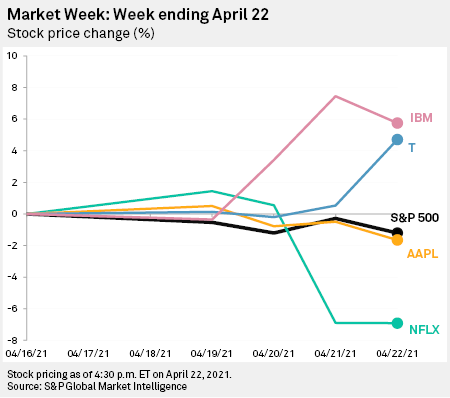

Netflix Craters On Subscriber Miss; New Ipads, Macs Steal iPhone's Thunder

With earnings season in full swing, investors last week mulled the new path forward for many tech and entertainment companies in a post-pandemic world. Shares in Netflix Inc. cratered by nearly 7% after the Silicon Valley darling on April 20 reported a massive slowdown in subscribers for the just-ended period, even though the company exceeded Wall Street estimates on the bottom line. Turning to Apple, the tech giant this week unveiled a refreshed iPad Pro and iMac equipped with the company's inaugural in-house developed M1 chip. Chris Rogers, supply chain analyst with Panjiva, a unit of S&P Global Market Intelligence, said the use of the company's proprietary semiconductor technology across several products may help Apple simplify its supply chain.

—Read the full article from S&P Global Market Intelligence

Affordability Of Global Mobile Services Barely Changed In 2020

Withstanding the impact of the pandemic, mobile users across the 48 markets covered by Kagan, part of S&P Global Market Intelligence, spent approximately 1.29% of their real personal disposable income on mobile services in 2020.

—Read the full article from S&P Global Market Intelligence

Listen: Next in Tech, Episode 12: Semiconductor Transformation

Are we going back to the future with semiconductors? 451 Research founders John Abbott and Nick Patience join host Eric Hanselman to flash back to some history that seems to be repeating itself in the processor battles we see emerging today.

—Listen and subscribe to Next in Tech, a podcast from S&P Global Market Intelligence

ESG in the Time of COVID-19

Listen: Platts Future Energy: UK Hydrogen’s Blue Vision

The UK's hydrogen production landscape is littered with big natural gas-based CCS projects – why is this, and what does it say about renewable hydrogen's immediate prospects? S&P Global Platts’ Zane McDonald, Jeff McDonald and Henry Edwardes-Evans discuss projects, prices and policies with a little help from Ryse Hydrogen's Jo Bamford.

—Listen and subscribe to Platts Future Energy, a podcast from S&P Global Platts

Less Rhetoric, More Action Emerges As Consensus Point At Biden's Climate Summit

The second day of the Leaders Summit on Climate convened by President Joe Biden kicked off April 23 with a clear message homing in on the need for international cooperation to combat climate change and a general consensus that rhetoric needs to be matched with swift action.

—Read the full article from S&P Global Platts

U.S. Hikes Climate Targets; Cites International, Market Momentum In Face Of Policy Divide

The US committed April 22 to reducing economywide greenhouse gas emissions by 50%-52% from 2005 levels by 2030, as some of the world's top emitters also reaffirmed or raised their ambitions to cut emissions at the start of a two-day climate summit hosted by US President Joe Biden.

—Read the full article from S&P Global Platts

Japan's New Climate Pledge To Boost Renewable, Nuclear Share In 2030 Energy Mix

Renewables and nuclear power are set to account for at least 50% of Japan's generation mix by 2030-31 (April-March), following the premier's "ambitious" new greenhouse gas emissions reduction target, Minister of Economy, Trade and Industry Hiroshi Kajiyama said April 23.

—Read the full article from S&P Global Platts

China To Curb Coal Demand Growth In Economic Plans As Part Of Climate Targets

China will curb coal consumption in its economic plans spanning the next 10 years, President Xi Jinping said April 22 at US President Joe Biden's global climate summit. Xi also affirmed China's existing targets on peak carbon dioxide emissions before 2030 and carbon neutrality before 2060.

—Read the full article from S&P Global Platts

The Future of Energy & Commodities

Listen: Commodites Focus: From Boom To Superboom: Are Suez Canal Misfortunes To Blame For Impending Port Delays?

Is the recent six-day Suez Canal blockage causing a spike in container box freight? And are the canal's misfortunes the only culprit for impending port delays, or the tip of the iceberg? It may be all too easy to blame the Ever Given incident for the latest logistical issues, rate hikes and arbitrage impacts on agricultural, metals and petrochemical commodity markets. S&P Global Platts Americas shipping managing editor Barbara Troner examines the container market with Platts experts Greg Holt in Houston and George Griffiths in London.

—Listen and subscribe to Commodities Focus, a podcast from S&P Global Platts

Written and compiled by Molly Mintz.

Content Type

Theme

Location

Language