S&P Global Market Intelligence — 28 Mar, 2020

COVID-19 The 451 Research Take

Introduction

The 451 Research analyst team is working to understand and assess these impacts to the technology industry specifically and the economy more broadly, providing in-depth insight across all impacted technology sectors that can help leaders navigate a path through the crisis. In this report, we offer a higher-level view of how the pandemic may impact key segments of the technology industry overall, including some recommendations for IT and business leaders looking to be responsive to this exceptional situation. All relevant research will be posted to our COVID-19 microsite.

The 451 Take

The rapid spread of COVID-19 may in part be a function of the global, connected economy, but it's also clear that modern technology is already playing a key role in helping organizations cope with this extraordinary and unique situation. From the obvious role that tech is playing in enabling home-based working, keeping at-home children schooled (and entertained) and helping families in isolation keep in touch with their loved ones, we also believe technology will be deployed in increasingly creative and innovative ways – perhaps acting as a catalyst for further adoption and more substantial growth. We already expect to see a surge in the use of contactless payments and mobile wallets to help enable social distancing, for example.

The Work-from-Home Explosion

The outbreak and growing threat of COVID-19 has significant implications across the board for business leaders needing to minimize the risk of employee infection, job disruption, reputational and compliance risks, employee disaffection and productivity loss, disruptions to strategic planning efforts, and general business continuity.

A comprehensive approach is needed, with key areas that focus on effectively communicating to employees; compliance with laws pertaining to discrimination, labor law, disclosures and ethics, and payroll; changes in benefits and PTO policies to mitigate the new pressures on the workforce; methods to ensure recruitment of talent needed for business continuity; the right tooling and governance policies to ensure effective management of more remote and distributed workforces; and adjustments as needed within strategic planning processes to maintain agility as circumstances change.

Specifically around the almost-overnight shift to remote working for many of those businesses that have generally been supportive of it, there likely will not have been significant thought around how to support prolonged remote working at scale, as opposed to occasional remote working by some of their employees. In other words, for the vast majority of companies now instituting large-scale remote working policies, there are new and significant cultural, operational and technical challenges to getting it right.

Although much of the talk has been around collaboration, conferencing and other communications tools, the real challenge with mass remote working at scale won't be enabling conversation as much as driving engagement around asynchronous work. In particular, providing visibility, transparency and accountability to support employees' focus and keep them aligned. Conversation should be a support, not a replacement, for those efforts.

Clearly, this challenge goes beyond standard conferencing and collaboration tools. While businesses should be wary of introducing too many new tools into their employees' armory – their key stated pain point as reported in our surveys is having to use too many apps – they might look to work management tools for the effective tracking of work; collaborative and immersive workspaces for bringing documents, data and conversations together; and innovation management platforms and employee engagement tools to unite and keep the workforce vested.

Security Implications

The widespread move to home working for a large part of the workforce for many organizations has direct implications for security. In addition to the multitude of new phishing attacks and attempts to exploit, for example, the distraction of healthcare IT teams who must focus on critical availability for medical and clinical reasons, organizations are now faced with a fundamental change in how they manage secure remote access, as well as how they can maintain visibility and control over security concerns.

Techniques predicated on visibility throughout an enterprise network become far less useful when substantially increased remote access is aggregated through a single, or few, VPN concentrators. Where before an organization could segment user networks, much policy or enforcement-relevant visibility is now lost when users all come into a single access point.

Just as troubling may be the vastly increased use of SaaS and cloud services for collaboration applications that enable workers to work and meet together when they can no longer gather in person. Each one of these applications may have its own point of access. When users reach them directly from their home networks, enterprise visibility and policy-based control for each of these connections may be lost and difficult to regain.

This, however, may introduce new opportunities for emerging trends in securing remote access. Implementations of 'zero trust' architectures may be called upon for user authentication that depends less on what network a user is on, and more on a demonstration of attributes such as user identity, endpoint, intended target, and the context from which access is sought.

Enterprises may seek out Identity as-a-Service (IDaaS) vendors to extend these capabilities at scale. Emerging concepts such as SASE (secure access service edge) that combine access security with SD-WAN may be spurred by this trend, while CASB (cloud access service brokers) may be sought to bring coherence to policy control across multiple SaaS and cloud resources in new ways. We explore these possibilities in our report on the security aspects of the stampede to remote work, Securing 'Social Distancing': Coronavirus, the Work-from-Home Explosion and Security.

A Swing to Digital Experiences

It's difficult to meet rising customer expectations during normal times, but situations such as pandemics wreak further havoc for many. Businesses have invested heavily in mobile application development and social media engagement technology, and a few even have self-service chatbots, but customers are still frustrated. Call centers can't keep up, websites are experiencing outages, and information shared online, in emails and on social media, is inconsistent.

The impact of store closures, ill-timed ad campaigns, and out-of-context messaging show how difficult it still is to act in real time across the customer journey. It's at this moment when we need to focus on digital experiences to remain relevant in the eyes of our customers. All businesses are fighting for smaller amounts of available discretionary dollars.

According to our Macro-economic March 2020 monthly consumer spending report, we see a big dip in overall spending, with 33% of consumers spending less over the next 90 days than the previous 90 days. As expected, areas hardest hit are travel, restaurants and consumer electronics. With 72% of our respondents also stating that the economy is going to worsen over the next 90 days, up from 28% in February, business leaders need to focus on remaining relevant to customers.

In our report, Digital Experiences are Front and Center in Coping with Coronavirus, we covered the top five insights to keep in mind as we navigate uncharted waters. There are lessons to be learned from these perilous times because digital experiences are now a catalyst for new technology investments. Bottom line: we need to pay closer attention to the digital experience. According to our VoCUL, Connected Customer Q3 data, 76% of consumers will likely switch as a result of poor website or mobile app performance. Additionally, 61% stated that a negative online experience makes them less likely to shop with a provider in the future.

There is a tremendous cost associated to not acting now. 451 Research's analysis demonstrates that at a minimum, there is at least $500bn in revenue opportunity in the US alone related to improving digital experiences, ranging from personalization improvements to mitigating abandoned shopping carts and other customer friction points. As consumers shift spending to online, businesses need to invest in new digital tools to work in a transformative way that ensures data, insights and key technologies connect people with information and processes, leading to a better experience for customers and, ultimately, business growth.

Driving Contactless Payments

The coronavirus outbreak is occurring during the largest and most aggressive period of contactless card issuance in US history. Large credit and debit card issuers are making multimillion-dollar investments to reissue their portfolios, and have already put more than 300 million cards into the US market with dual-interface (e.g., chip and contactless) capabilities. Their objective is largely to displace cash usage by increasing the attractiveness of cards as an alternative for low-value transactions.

Somewhat serendipitously for card issuers, cash is quickly coming under fire as a high-risk vehicle for spreading the coronavirus, given its widespread use and inherent person-to-person qualities. Card marketers at US financial institutions should look to the coronavirus as a uniquely simple and effective messaging opportunity that can be harnessed to encourage contactless card take-up. This could be particularly useful for converting the two in five cardholders that we find possess a contactless card but are not yet using the tap-to-pay capability.

Over the next several months, we expect opportunistic card issuers, wallet providers and payment networks to build marketing messaging around the sanitary benefits of contactless payments. We advise focusing first on major metro areas, especially in those like New York that are undergoing a transition to open-loop contactless ticketing in their public transit systems.

Infrastructure Impacts

5G/telecom

In the telecom sector, the COVID-19 virus has mobilized an entire industry to focus on two goals:

- Bolstering broadband infrastructure capacity, and the availability to support unprecedented consumer, remote worker, government/public safety and enterprise demand.

- Compassionate measures to ensure the consumers affected by COVID-19 have the access they need without encumbrances, including data caps, late fees and service discontinuation.

This disaster will stress-test network infrastructure, and in some markets accelerate the need for 5G standalone architectures for both performance and cost savings. In fact, surviving the coronavirus will place a magnifying glass on potential 5G use cases that a year ago may have seemed far-fetched, such as remote medical procedures and consultations, and 100% automated and robotic plants and warehouse systems.

AR/VR will apply to a number of daily usage contexts (driven by our difficult experience with social distancing). These include social interactions, gaming, virtual travel, experiences, exploring, distance learning, dating, business transactions, training and field working.

Business continuity/disaster recovery

Quarantine situations like those being initiated for managing COVID-19 are fundamentally similar to many other business continuity/disaster recovery (BC/DR) scenarios, and illustrate the need for a BC/DR plan that addresses the interruption of access to key IT personnel and systems. In the case of COVID-19, most datacenters are low-population areas with tight access control, so the concern is less about spreading the illness, and more about adjusting to a potentially depleted IT workforce.

In the physical datacenter environment, we recommend implementing a BC/DR plan that can be followed in the absence of key administrative personnel with significant remote monitoring and command and control (with multiple connectivity options). Increasing the overall automation of commonly needed services and functions will also see an overall elevation.

For the knowledge-based workforce outside the datacenter, we recommend ensuring availability of reliable and secure internet connectivity for SaaS, remote desktop and on-premises applications. We recommend provisioning and training IT teams with cloud-based collaboration tools. We also recommend mandatory VPN usage, strong data protection for local storage, and consideration of adopting enterprise file sync and share services.

Application and infrastructure performance

For many businesses, applications and services will become the only potential for revenue at a time when social distancing recommendations have shut down revenue streams from most kinds of physical stores and in-person events. In this environment, performance is more important than ever – an application that is slow or unavailable could represent the loss of the only source of revenue a business might have. Our 451 Research Voice of the Connected User Landscape report found that 67% of respondents said they would be somewhat or very likely to switch brands or providers due to poor performance of an online app or service.

We expect this overreliance on digital properties to elevate the value of application and infrastructure monitoring in organizations. Vendors in the sector should be able to maintain or grow business, in line with the overall growth of digital properties resulting from the implications of the COVID-19 virus. We recommend that enterprises plan to continue their investments in monitoring tools.

Cloud Impact

At times like this, the scalability of the cloud really comes into its own. As the behavior of the populace changes, we can expect some web applications to explode with traffic, while others might dwindle to near nothing. News websites are likely to spike as worried citizens look for information; e-commerce sites might receive lower hits as consumers wait for more optimistic times (or may have to do what some retailers have done, shut down their online stores entirely). Scalable cloud applications should be able to grow and shrink to meet this changing demand automatically. For those suffering from lower hits, scaling down at least saves a bit of cash – a silver lining in challenging times. For those experiencing a surge, the cloud lets websites continue to perform under pressure.

Crucially, this scaling can be configured automatically with no need to forecast or plan capacity. With personnel challenges, this automation can make a big differences. Six months ago, not one enterprise could have possibly forecasted a global pandemic that would impact not just their capacity, but their whole raison d'etre. Many private clouds will sit unutilized in datacenters, while others will be overwhelmed as demand exceeds the steady-state capacity expectation. With a public cloud, the cloud provider, not the enterprise, is responsible for capacity. Enterprises operating hybrid IT environments can also burst to meet increased capacity demands – but the ability to scale down is limited, given the fixed-capacity nature of their dedicated private cloud resources.

Unfortunately, for enterprises that haven't already built scalable cloud-native applications, it is too late. Enterprises that were prepared will be best placed to make the most of tough times. It's the same with business continuity planning – if you haven't planned before the event, your options now are limited. However, enterprises should take a fresh look at their IT deployments to determine whether adding or removing resources can help meet demand or save costs, respectively. We are confident that the hyperscalers have planned for eventualities such as this, and have the capacity and processes to deal with enterprises facing the unexpected.

The transition of physical interactions to virtual ones, during and following COVID-19, will increase the demand for more agile approaches to software and service development, enabling organizations to respond to changing conditions more quickly. This requirement will increase the need for organizations to make operations and a culture of responsibility pervasive, to use smaller, more loosely joined teams, and to re-shore activity to be closer to the business. Momentum around cloud-native engineering approaches using DevOps processes will accelerate to support this. In general, suppliers that can take out cost, reduce risk and take out humans from noncritical operations with automation should also be cautiously optimistic about their future.

Datacenter Impacts

COVID-19 has highlighted the mission criticality of the multi-tenant/leased datacenter industry, with more workers than ever relying on remote services delivered out of the cloud. Media and content providers, as well as network service providers, will experience increased demand for services, leading to increased peering and bandwidth requirements, and new conversations around disaster recovery.

If they were not already, governments are starting to consider datacenters alongside utility providers in Europe as integral to keeping the activities of economies, hospitals and society – from dissemination of information to online shopping – in working order. This has placed increased importance on providers' business continuity plans.There are many measures the MTDC industry is taking to keep datacenters running, from restricting visitor access and site tours to only those required to rotating staff in shifts and keeping MTDC staff separate from customers. This is on top of basic hygiene such as sanitation, and in some facilities, kits to test for fever prior to datacenter entry. Many providers learned lessons from New York with Hurricane Sandy back in 2012. They have instigated regular, almost daily, customer communication, and are acting with transparency.

In some markets, providers are undertaking wider discussions across the industry to ensure a unified approach to 'keeping the lights on.' Construction projects and new builds are still taking place in many markets for now, but providers say they are concerned about supply chain and staffing pressures as the virus takes hold and further border controls are enacted. They warn this could delay many new build projects through 2020, and even into 2021. Such restrictions impact mechanical and electrical equipment, as well as the servers required for service expansion by customers. Providers are also expecting new customer activity to slow as well as longer sales cycles, as major decisions around technology migrations are delayed.

The Role for AI/ML

AI will have a major part to play in the detection of future pandemics, and in the eventual creation of a remedy and vaccine for COVID-19, even if it didn't manage to predict the outbreak this time. This will happen because of advances in AI, but also because of the masses of data being created.

We have seen a few good visualizations of how the virus is spreading across the world in the past few weeks, but none are bold enough to actually predict its future path. However, once we are through the worst – and have amassed huge amounts of data – machine learning will be used to spot patterns to help us learn how future coronaviruses might spread.

The US government, along with academic institutions and technology companies, has just announced the COVID-19 Open Research Dataset, known as CORD-19, which will be an open dataset usable by AI researchers. There have been attempts to predict pandemics, such as the one led by USAID (US Agency for International Development) – the Predict project – and we expect such initiatives to get more funding and focus in the future. Google's Kaggle has also launched datasets and competitions to predict the factors that impact the transmission rate of COVID-19.

Getting a new drug to market is a notoriously long, difficult and expensive process; however, if a drug is already licensed for human use and can help treat COVID-19, then licensing it for treatment of the virus could take a matter of months, rather than many years. Ascertaining the efficacy of any drugs requires enormous amounts of trawling through documentation, which is something machine learning is very good at, and we know pharmaceutical companies are pursuing this path.

Related to that is the clinical trial process, where machine learning can also help by identifying patients who are suitable for clinical trials. This is known as the trial matching process, and technologies such as natural language processing are being used to identify patients for trials by analyzing disparate sets of medical data strewn across multiple sources, rather than just relying on the structured data in electronic medical record systems – resulting in much faster trial matching to get clinical trials up and running more quickly.

M&A Impacts

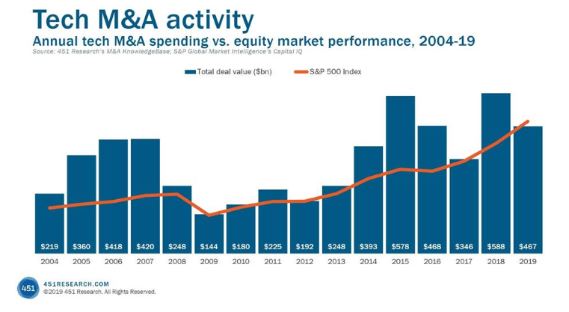

Given the longstanding correlation between Wall Street and M&A, it's a pretty sure bet the coronavirus pandemic will drag down tech acquisition activity. (After all, both markets run on confidence – a commodity, like toilet paper and bleach, that's awfully hard to find in these shelter-in-place days.) But unlike stocks, where twitchy traders react to bad news instantaneously, the disruption in the tech M&A market won't be fully evident for some time.

A look back at the last decade's financial pandemic, the Credit Crisis, provides at least a rough timeline for the lag between economic/financial calamities and when they show up in the M&A totals. Most of the confidence-shattering events of the Credit Crisis – such as the bankruptcy of Lehman Brothers and the collapse of AIG – took place in 2008. As liquidity dried up and business ground to a halt that year, the S&P 500 plummeted nearly 40%, erasing trillions of dollars of value from stocks around the globe.

Yet for investors and businesses, the worst economic downturn since the Great Depression turned upward in short order. The recession officially ended in 2009, and Wall Street's bull market began its historic gallop. (The S&P 500 returned about 25% in 2009, kicking off a nearly uninterrupted rise that saw the index almost quadruple over the next decade.)

Unlike those markets, tech M&A took much longer to recover. After bottoming out in 2009, tech acquisition spending remained exceptionally weak for three additional years. (From 2009 to 2012, tech acquirers averaged less than half the annual spending they had in the two years immediately leading up to the recession, according to 451 Research's M&A KnowledgeBase.) Our data shows it was only in 2013 that the value of global tech deals regained 2008's level. In other words, a two-year economic recession caused an M&A slump that lingered painfully for a half decade (see Figure 1 below).