23 Mar, 2020

COVID-19 Daily Update: March 23, 2020

By S&P Global

Governments globally are grappling with the combined economic and humanitarian losses of the coronavirus outbreak as the total number of infected people surpassed 372,500 today. While 13,500 cases have recovered since S&P Global’s last COVID-19 Update on March 20, the death toll between now and Friday rose by more than 5,000 people, according to Johns Hopkins University data.

“For 2020 [the outlook for global growth] is negative—a recession at least as bad as during the global financial crisis or worse. But we expect recovery in 2021,” Kristalina Georgieva, the International Monetary Fund's Managing Director, said today in a conference call with G20 finance ministers and central bank governors.

United Nations Secretary-General Antonio Guterres today called a global ceasefire of armed conflict in the face of the coronavirus outbreak. “It is time to put armed conflict on lockdown and focus together on the true fight of our lives. To warring parties, I say: pull back from hostilities. Put aside mistrust and animosity. Silence the guns; stop the artillery; end the airstrikes. This is crucial to help create corridors for life saving aids. To open precious windows for diplomacy. To bring hope to places among the most vulnerable to COVID-19,” Guterres said in a video statement shared on social media.

Prime Minister Boris Johnson announced a stay-at-home order for the United Kingdom, drastically restricting citizens’ movements beyond shopping for basic necessities, exercising once a day, seeking medical help, and traveling to and from work when necessary. Europe is still strained by the pandemic; today, France exacted tougher lockdown rules, Ireland reported the country’s greatest daily rise in new cases, and the number of new cases in Italy is dropping. Italy's government moved to extend the shutdown of the country yesterday by ordering closure of all non-essential industrial and commercial activities until April 3. The situation that Italy has seen is unfolding in a similar fashion in Spain, where the economic effects are estimated to have around a 10-day lag to Italy.

In the U.S., markets slid as the Federal Reserve expanded its efforts to support businesses and Congress debated government rescue packages. The U.S. Senate failed for a second time to advance an economic stimulus package with Republican leaders unable to secure 60 votes in the face of Democratic opposition. Several Republican senators were unable to vote after one tested positive for the virus and others were in isolation for possible exposure. President Donald Trump has expressed impatience with the response to the rapidly spreading virus.

Markets continue to sink even as global action strives to stabilize them. Financial market turmoil in response to the pandemic is pressuring funding conditions while earnings for some sectors are expected to plummet under the strain of supply disruptions and tanking demand, according to S&P Global Ratings. Comparatively, S&P Dow Jones Indices reports that the market has turned sharply down since mid-February in response to the coronavirus pandemic, with the S&P 500® having fallen approximately 32% from its peak this year.

Oil futures opened lower Sunday evening, as global coronavirus cases continued to rise over the weekend and news broke that UAE's Emirates airline will suspend most passenger flights. Today, crude futures were lower in mid-morning trade in Asia as news of more and more countries going under lockdown weigh on the overall economic outlook. Meanwhile, Saudi Aramco vowed there will be no disruption in its oil and gas supplies to customers even as international borders close and transportation venues are cut off.

S&P Global Ratings lowered its 2020 oil price assumptions for the second time in a month. U.S. producers are likely to be hurt the most by lower oil prices. Analysis by S&P Global Platts shows that margins are turning negative on the drop in gasoline demand, and global refiners began to cut capacity to meet the lower demand and delayed planned work to manage the spread of COVID-19.

The coronavirus outbreak has prompted a widespread drag to supply chains, slowed logistics, left many firms in the dark over its total impact, shone a spotlight on expedited deliveries, and signaled that earlier shortages will reverberate for weeks or months.

Today is Monday, March 23, and here is essential insight on COVID-19 and the markets.

CREDIT MARKETS

VIDEO OF THE DAY

The COVID-19 Fallout: Quantifying first-cut impact of the pandemic<.b>

The Novel Coronavirus (Covid-19) has cast a long shadow over a much-anticipated mild recovery in the Indian economy in fiscal 2021, with the World Health Organization (WHO) declaring it a pandemic. External risks to global growth has increased significantly now. S&P Global foresees a recession in the US and the Eurozone, and has its forecast for China’s growth slashed to 2.9% from 4.8% announced on March 5. Domestically, some hit to consumption demand because of social distancing is likely, though it is too early for that to reflect in data. Currently, the other downside to growth is also due to the financial sector stress now percolating to private sector banks.

In view of this, CRISIL has cut its base-case gross domestic product (GDP) growth forecast for fiscal 2021 to 5.2%, from 5.7% announced recently. This factors in the huge uncertainty because of Covid-19, with risks to the forecast tilted downwards. The forecast will be reassessed continuously as new information becomes available. A serious downside to our base case can emerge from two developments. One, the pandemic is not contained by April-June 2020 globally, and makes the global slowdown more severe. And two, it spreads rapidly in India, affecting domestic consumption, investment, and production. These would further hurt confidence and the financial markets.

—Read the full report from CRISIL, an S&P Global company

Default, Transition, and Recovery: The Global Recession Is Likely To Push The U.S. Default Rate To 10%

We expect the U.S. trailing-12-month speculative-grade corporate default rate to rise to 10% within the next 12 months, from 3.1% in December 2019, as a global recession is now here amid the coronavirus pandemic. Financial market turmoil in response to the pandemic is pressuring funding conditions while earnings for some sectors are expected to plummet under the strain of supply disruptions and tanking demand.

In our pessimistic scenario, a protracted period of fighting to contain the virus and reduced effectiveness of stimulus measures could lead to a longer recession, pushing the default rate to about 13%. The oil and gas sector is likely to be particularly hard hit during this time--oil prices have fallen below $30 per barrel amid expanding supply following the standoff between Saudi Arabia and Russia. A quick resolution between the two parties is not expected.

—Read the full article from S&P Global Ratings

U.S. Corporate Debt Market under Pressure

Since mid-February, the market has turned sharply down in response to the coronavirus pandemic. The S&P 500® has fallen about 32% from its peak this year. Equity volatility shot up, as VIX® went from historical lows to the 70-80 range, which was last seen in November 2008. The 10-year U.S. Treasury Bond yield reached 0.32% intraday before it bounced back above 1%, as the market expected more debt issuance with drastic fiscal measures to combat the economic slowdown. How has U.S. corporate debt weathered this market storm so far?

S&P Dow Jones Indices shows the average credit spread of the U.S. corporate bond market in the context of post-2008 global financial crisis (GFC). The recent move has put spreads at the widest since the GFC, and still much tighter than the peak level during the 2008 GFC when the investment grade spread reached over 500 bps and high yield over 2000 bps.

How did corporate bonds with different credit quality perform during this market stress? S&P Dow Jones Indices charts the spread difference between spreads of investment grade versus ‘BBB’ and ‘BB’ versus ‘B’. The widening of spreads between rating buckets has been consistent with the direction of spread widening, and the fact that the spread between ‘BB’ and ‘B’ has reached a new post-GFC high is very concerning. In fact, the weighted average price of leveraged loans dropped to 77.06 on March 19, 2020, a new low since the rally after 2009. Market participants may now wonder about the funding and default risk ahead.

—Read the full article from S&P Dow Jones Indices

COVID-19 Will Batter Global Auto Sales And Credit Quality

S&P Global Ratings is further lowering our forecasts for global light vehicle sales as the coronavirus pandemic escalates and global growth heads sharply lower. We now project global sales will decline by almost 15% in 2020 to less than 80 million units. We expect global automakers and suppliers will face intense credit pressures, which will test their liquidity management and the headroom in their credit metrics.

While China appears to be starting to rein in the coronavirus outbreak, Europe and the U.S. are testing their capacity to contain the virus' spread. S&P Global Ratings acknowledges a high degree of uncertainty about the rate of spread and peak of the coronavirus outbreak. Some government authorities estimate the pandemic will peak between June and August, and we are using this assumption in assessing the economic and credit implications. We believe measures to contain COVID-19 have pushed the global economy into recession and could cause a surge of defaults among nonfinancial corporate borrowers. As the situation evolves, we will update our assumptions and estimates accordingly.

—Read the full article from S&P Global Ratings

CHART OF THE DAY

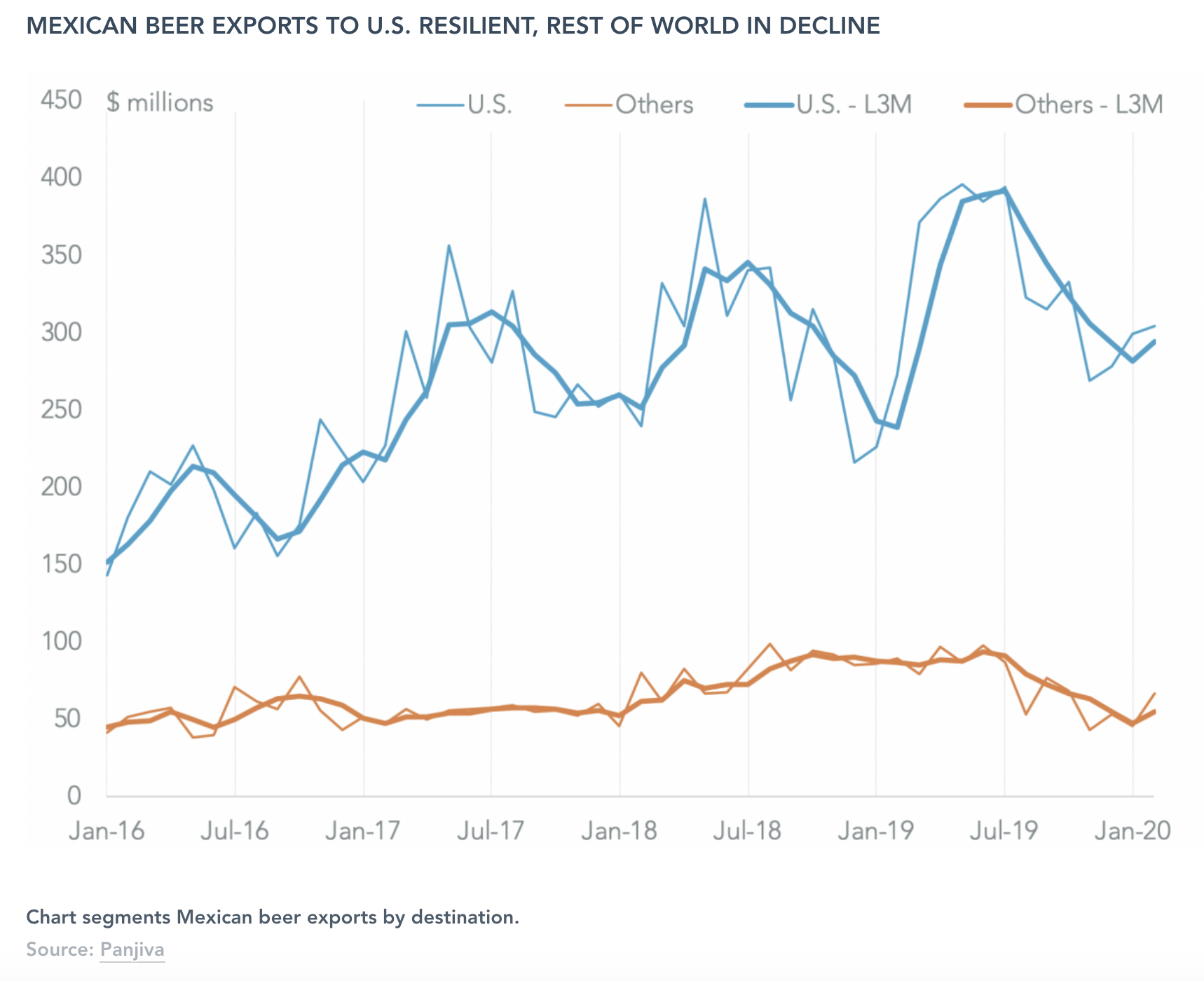

Coronavirus not the only malady facing Mexican beer exporters

Government actions around the world in response to coronavirus, including the U.S., are leading to widespread closures of pubs and bars – raising the prospect of reduced beer sales through that route, though drink at home sales may pick up. As discussed in Panjiva’s research of March 16, the spread of coronavirus is being felt acutely in both the supply and demand side of the consumer goods industries.

There’s already been a notable impact on the brewing industry. Panjiva data shows that Mexican beer exports have generally been resilient so far with a 2.2% year over year expansion in shipments in February following a 10.4% surge in January. Yet, that was supported by strong exports to the U.S. which rose by 11.4% in January while shipments to the rest of the world slumped 26.0% lower.

—Read the full article from Panjiva, part of S&P Global Market Intelligence

We’re not there yet – 18 coronavirus lessons from supply chain and financial data

This report takes two approaches to analyzing the fallout from the SARS-CoV-2 / COVID-19 coronavirus outbreak on global trade and corporate supply chains. The first draws on over 50 reports from Panjiva Research to identify 11 themes emerging on an event-driven basis. The second takes a more programmatic approach to combining stock price performance and supply chain characteristics to identify seven examples of differentiated corporate performance.

TSince news regarding the outbreak of SARS-CoV-2 / COVID-19 coronavirus in Hubei province, China in mid-January Panjiva research has published over 50 short-form reports looking at the issue across a wide range of industries. We’ve identified 11 themes emerging from our analysis so far: the drag to supply chains has been widespread, logistics has slowed down rapidly, many firms don’t yet know the impact, tariff lessons are coming in useful, expedited deliveries are becoming more important, second order effects are beginning to be felt, retailers are winning on sales but may lose in supplies, healthcare drawbridges are drawn up, earlier shortages will reverberate for weeks or months, it’s starting to get better in places, and the post coronavirus bounce back could mark a return to the same old problems.

—Read the full article from Panjiva, part of S&P Global Market Intelligence

Small insurers may face insolvency if virus curve doesn't flatten — US regulator

A failure to contain the coronavirus epidemic could put pressure on smaller health insurers in the U.S. and push some to insolvency, Virginia Insurance Commissioner Scott White said. Referring to efforts to "flatten the curve" of coronavirus cases, White said, "To the extent the flattening does occur, I think it's safe to say there will be few if any immediate solvency issues for the industry. The question is what happens if the flattening does not occur in the near term."

Speaking during a virtual National Association of Insurance Commissioners meeting March 20, White, who chairs the NAIC's financial condition committee, said the healthcare system could be overwhelmed with patients. He compared the current virus to the Spanish flu, which began in the spring of 1918, lasted for more than two years and was blamed for some 50 million deaths. If the flattening does not occur, "it's likely that some of the small health insurers might become financially stressed, perhaps even become insolvent," he said.

—Read the full article from S&P Global Market Intelligence

E-commerce drives China's stay-at-home economy in coronavirus aftermath

The new coronavirus outbreak has significantly changed consumer behavior in China and could intensify the rivalry between Alibaba Group Holding Ltd. and Tencent Holdings Ltd. in the low-priced online grocery segment, but the broader outlook for the year remains grim as customers shun high-priced discretionary goods. As the country shifted to what has been dubbed a stay-at-home economy, consumers ordered fewer restaurant takeouts and cooked more, bought more home cleaning and personal hygiene products, and ordered fewer fashion and discretionary items, according to an analysis of data released by the Chinese government and e-commerce companies. Sales of items such as yoga mats, pajamas and kitchen utensils also surged.

Alibaba and Tencent-backed JD.com Inc. reported that online sales of grocery, fresh produce and consumer essentials grew manifold during the quarantine, driving up the country's online retail sales of physical goods by 3% to 1.123 trillion yuan in the first two months of the year.

—Read the full article from S&P Global Market Intelligence

COVID-19 presents snag for Deutsche Bank restructuring plans

The new coronavirus outbreak will weigh on Deutsche Bank AG's restructuring efforts as the market turmoil triggered by the pandemic and its economic impact will leave almost none of the group's businesses unscathed in 2020, according to analysts. The German group said in its 2019 earnings report released March 20 that its ability to meet financial targets could be "materially adversely affected" due to a prolonged economic downturn triggered by COVID-19, the disease caused by the virus. The bank confirmed its 2020 targets for adjusted costs of €19.5 billion, a common equity Tier 1 ratio of at least 12.5% and a leverage ratio of 4.5% but said those do not include COVID-19 effects.

The overall outlook for the European banking sector is gloomy with all institutions likely to face severe short-term revenue pressure, but banks with preexisting profitability issues will be the most vulnerable to the virus-induced hit, analysts said.

—Read the full article from S&P Global Market Intelligence

TRACKING THE SPREAD AND ECONOMIC IMPACT OF CORONAVIRUS

The global recession is here and now

Geographic Distribution of Confirmed Coronavirus COVID-19 Cases, Mar. 22, 2020

Source: John Hopkins CSSE, S&P Global Ratings. Note that French Guiana in South America is mapped as part of France.

Copyright © 2020 by Standard & Poor's Financial Services LLC. All rights reserved.

There are now six countries with more than 10,000 cases – Italy, Iran, Spain, Germany, the U.S. and France - and other countries are on trajectories likely to bring similar case counts soon. 62 countries already have in excess of 100 cases. Europe has now become the epicenter of the outbreak, with the U.S. on course to be similarly affected. If there is some good to be found, it is that the daily new case rate has fallen to near-zero in China, where the virus first took hold. The social and economic consequences of COVID-19 have consequently become much more severe and we now forecast a global recession this year, with 2020 GDP rising just 1.0%-1.5%. Global recession, combined with the collapse in oil prices and extreme volatility in capital markets, will inevitably have severe implications for credit markets. In S&P Global Ratings' view, this will likely mean a surge in defaults, potentially reaching a double-digit speculative-grade default rate for nonfinancial corporates in the U.S. and a material increase to high single digits in Europe over the next six to 12 months.

The chart above provides an updated and interactive view of confirmed cases globally, using data provided by the Center for Systems Science and Engineering at John Hopkins University. It also provides an estimated reduction in 2020 GDP growth relative to S&P Global Ratings's previous baseline forecast for countries more exposed to the economic and confidence shock resulting from the outbreak.

—Read the full article and engage with more interactive data visualizations from S&P Global Ratings

OIL & ENERGY MARKETS

U.S. Senate again fails to advance aid package with SPR, airline relief

The U.S. Senate failed for a second time Monday to advance an economic stimulus package to respond to the coronavirus pandemic, with measures including $3 billion for crude purchases to fill the Strategic Petroleum Reserve and $58 billion in relief for the reeling airline industry.

Preliminary motions to start debate on the legislation failed Sunday and Monday, with Republican leaders unable to secure 60 votes in the face of Democratic opposition. Several Republican senators were unable to vote after one tested positive for the virus and others were in isolation for possible exposure. The Trump administration has asked Congress for $3 billion to buy US-origin crude to fill the government's emergency oil stockpile.

—Read the full article from S&P Global Platts

Italy, Spain further restrict activity, quashing power demand in both markets

Italy's government Sunday moved to extend the shutdown of the country by ordering closure of all non-essential industrial and commercial activities until April 3. The energy industry as whole is among those exempted due to its strategic nature, along with food and heat supplies among others, according to Sunday's decree. The decree singled out refining, power generating, chemicals, rubber, plastics and aluminum as sectors that would be allowed to continue operations under the new decree, while other industries not covered are permitted to continue working remotely.

The situation that Italy has seen is unfolding in a similar fashion in Spain, where the economic effects are estimated to have around a 10-day lag to Italy. Spain is also mulling extending its lockdown period and tightening its measures against the virus, with a likely extension until April 11. The country has already passed a decree to suspend cuts to interruptible contracts as industrial demand falls off. Large swathes of industry have already closed, including the country's largest auto plants, with total demand dropping as a result.

—Read the full article from S&P Global Platts

Oil seen at $25-$30/b as US likely to be victim of price war: S&P Global Ratings

S&P Global Ratings lowered its 2020 oil price assumptions for the second time in a month, and said US producers are likely to be hurt the most by lower oil prices. The 2020 price assumptions were lowered $10/b, to $25/b for WTI and to $30/b for Brent, according to a March 22 statement. Assumptions for 2021 and 2022 were not changed. S&P Global Ratings joins a number of organizations that are reassessing oil price forecasts as prices continue to tumble despite multi-trillion stimulus measures announced around the world.

—Read the full article from S&P Global Platts

PODCAST OF THE DAY

Listen: Coronavirus forces jet market collapse

COVID-19 has crushed demand and prices of jet fuel around the world. What can be done with all that extra jet fuel, and what are the prospects for airlines as they struggle to stay viable? S&P Global Platts reporters Gary Clark and Francesco Di Salvo discuss this challenging market on S&P Global Platt's Oil Markets podcast with Joel Hanley.

—Listen to the Oil Markets podcast episode S&P Global Platts

Shell, Total pull initial levers to mitigate oil price crisis

Two of the largest integrated oil and gas majors are slashing capital spending budgets to help stave off short-term bloodletting expected from the plunge in global oil prices and the contraction in demand brought on by the coronavirus pandemic. Lower-for-longer crude price scenarios have prompted Total SA and Royal Dutch Shell PLC to start pulling initial levers, with both announcing plans March 23 to cut capital expenditures and suspend share buybacks. Shell will slice 2020 spending by at least $5 billion, to $20 billion or lower; trim underlying operating costs by $3 billion to $4 billion per year over the next 12 months; and delay the next $1 billion tranche of its massive $25 billion repurchase program.

—Read the full article from S&P Global Market Intelligence

Coronavirus threatens to derail major US EPA energy and climate rollbacks

Following a record-long 35-day government shutdown early last year, President Donald Trump's administration was already running short on time to finish high-priority environmental rollbacks before the November 2020 elections. Now the coronavirus outbreak that is sweeping across the nation is also threatening to derail some of the most important pieces of Trump's deregulatory environmental agenda by causing workforce disruptions and court delays.

The evidence is already beginning to mount in federal court filings. On March 20, lawyers representing the U.S. Environmental Protection Agency and a coalition of states, public health organizations and environmental groups jointly asked a federal appeals court to extend the briefing schedule in a pivotal lawsuit challenging the repeal and replacement of the Obama-era Clean Power Plan.

"Some counsel actively involved in the briefing for coordinating petitioners – including those located in the San Francisco Bay Area – are subject to 'shelter in place' orders prohibiting activity outside the home other than enumerated essential purposes such as purchasing food," state petitioners told the U.S. Court of Appeals for the District of Columbia Circuit.

—Read the full article from S&P Global Market Intelligence

Refinery margin tracker: Global refining margins take a severe hit on falling gasoline demand

Refining margins are turning negative on the drop in gasoline demand and global refiners began to cut runs to meet the lower demand and delayed planned work to manage the spread of COVID-19, an analysis from S&P Global Platts showed Monday. Atlantic Basin refiners announced run cuts as some margins dipped into negative territory, a result of the sharp fall-off in gasoline demand resulting from widespread stay-at-home mandates keeping drivers off the road.

—Read the full article from S&P Global Platts

As oil prices tumble, US policymakers debate how to deal with Saudi Arabia

The collapse in global oil prices has US policymakers scrambling for ways to save the domestic oil sector, but disagreement is brewing on whether to work with Saudi Arabia for market balance or pursue penalties against the OPEC kingpin for plans to significantly ramp up its crude production in the coming months.

"Energy is a key part of the diplomatic dialogue between the US and Saudi Arabia, and the US today should be talking with the kingdom about what steps can be taken to support the global economy in the midst of a historic economic crisis," Jason Bordoff, a former energy adviser to US President Barack Obama and director of the Center on Global Energy Policy at Columbia University, told S&P Global Platts Monday. "This is a moment when the kingdom can demonstrate its commitment to being a responsible swing supplier.

In the span of just a few hours Friday: Texas Railroad Commissioner Ryan Sitton floated the idea of an international supply cut pact to OPEC Secretary General Mohammed Barkindo; Commission Chairman Wayne Christian dismissed the idea; and nine Republican senators asked the Department of Commerce to launch an anti-dumping case against Saudi Arabia following its price war with Russia. Saudi Arabia and Russia were flooding the market with an "unprecedented" amount of crude, the senators wrote to Commerce Secretary Wilbur Ross.

—Read the full article from S&P Global Platts

Saudi Aramco vows stable oil supplies even as borders, transit routes shut

Saudi Aramco vowed there will be no disruption in its oil and gas supplies to customers even as international borders have closed and transportation venues cut off.

"We have developed emergency and prevention plans in all areas of our business to ensure the ongoing of our business so that we can meet the needs of our customers around the world," CEO Amin Nasser said in a statement published Saturday on the state-run Saudi Press Agency. Aramco is closely monitoring the health and safety of its employees and facilities, Nasser said. "We have been carrying out continuous preventive plans in all our business areas, in addition to detailed emergency plans and leading medical support services, in order to reduce risks, ensure the best possible care and curb COVID-19 infection," he said.

—Read the full article from S&P Global Platts

Italian steel mills to close under coronavirus measures, ArcelorMittal's Taranto exempted

Italian steel mills will have to shut down most operations under a government decree issued Sunday tightening restrictions to fight the spread coronavirus. The government has ordered the suspension of industrial and commercial activities that are not essential by March 25. Market sources said that although most mills would not be allowed to continue production, some are trying to secure the requisite permission from local prefects to carry on. Unions have promised to fight such moves and say they are ready to call a huge strike to prevent plants staying open.

—Read the full article from S&P Global Platts

European toluene continues to test new lows, plunges 45% so far in March

The price of European toluene has dropped by around 45% since the start of this month, with most of the losses coming during the week of March 9, after OPEC+ members failed to agree on further production cuts. Platts Toluene TDI has plunged by $265.25/mt since the last day of February, to be assessed at $311.25/mt on Friday, suppressing market liquidity and sending market participants to the sidelines.

This was attributed to sharp losses in upstream oil prices and the spread of coronavirus pandemic outside Asia, making it harder for market players to pinpoint the correct outright price for the materials. The resulting lack of liquidity kept market participants on the sidelines waiting for market to stabilize to gain more clarity on its state.

—Read the full article from S&P Global Platts

UAE's Emirates to suspend most passenger flights, hitting Dubai aviation industry

UAE's Emirates, the world's biggest long-haul airline, will suspend most passenger flights as of March 25, operating mainly cargo, as one of Dubai's main economic pillars takes a hit from the outbreak of the coronavirus. Emirates, which used to fly to over 160 destinations, is implementing a slew of measures, including salary cuts to stay afloat, it said in a statement on Sunday.

"As a global network airline, we find ourselves in a situation where we cannot viably operate passenger services until countries re-open their borders, and travel confidence returns," Sheikh Ahmed bin Saeed Al Maktoum, chairman and CEO of Emirates Group, said in the statement.

—Read the full article from S&P Global Platts

Written and compiled by Molly Mintz.

Content Type

Location

Language