S&P Global Platts — 9 Jun, 2020

Commodity Tracker: 4 charts to watch this week

Highlights

A recovery in Chinese independent refiners’ oil imports tops this week’s pick of trends in energy and raw materials markets. EU carbon markets, the relationship between US rig counts and tubular steel prices, and LNG supply to Europe are also on the agenda.

1. Saudi crude supply to Chinese independent refiners soars in May

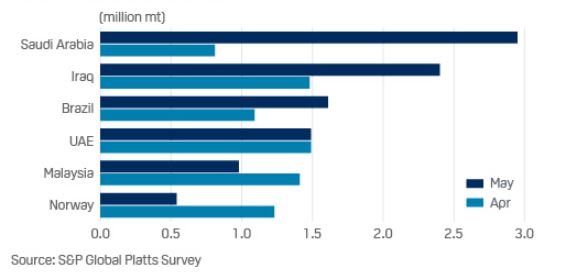

CHINA INDEPENDENT REFINERS RAMP UP CRUDE IMPORTS

FROM MIDDLE EAST IN MAY

What’s happening? China’s independent refiners ratcheted up crude imports in May by 71.1% on the year to a record high 4.42 million b/d, sending a bullish signal to the global oil market that the recovery in Chinese energy demand is on track. The independent refining sector’s crude imports from Saudi Arabia, Iraq, Oman and UAE increased 62.5% on the month to 7.78 million mt in May, accounting for about 41.6% of the total arrivals for those independent refineries, a monthly survey by S&P Global Platts showed June 3. Supply from Saudi Arabia jumped more than threefold from April to 2.95 million mt.

What’s next? Major Middle Eastern crude producers and Russia would draw support from the latest Chinese import data, as rapid energy demand recovery in the country would provide incentives for the major crude suppliers to reconsider production cuts in Q3. OPEC and its allies agreed on June 6 to extend the coalition’s 9.6 million b/d output cut agreement through July. The cuts – originally 9.7 million b/d including Mexico – had been scheduled to taper to 7.7 million b/d in July through the rest of the year. The independent sector’s bullish Middle Eastern crude import figures, coupled with recent sharp recovery in Dubai crude benchmark price structure may also prove effective in raising official selling prices (OSPs) for Middle Eastern crude grades flowing to Asia, industry officials and market participants said.

2. EU carbon market eyes evolving policy as price rebounds

EUA NEWREST-DECEMBER PRICE (Eur/mt)

What’s happening? EU carbon dioxide allowance prices have rebounded above Eur20.00/mt from their March lows of below Eur15.00/mt – seemingly defying a very bearish demand picture. A severe slump in demand due to the coronavirus lockdowns in Europe has combined with an already cheap natural gas picture. This means industrial sector demand for allowances is extremely low at the same time that cleaner gas-fired electricity plants continue to keep more emissions-intensive coal off the power grids in Europe, curbing utility hedging demand. However, the relative resilience of carbon prices is partly linked to the supply side: carbon market reforms are coming, and market participants are aware that EU regulators want to agree tougher 2030 emissions targets as well as tapping the carbon market to help deliver a low carbon economy by 2050.

What’s next? While analysts and traders say a drop back below Eur20/mt cannot be ruled out in the short-term – even as low as Eur15/mt – any significant price dips are likely to continue to attract buy-side support, given market reforms that could tighten supply in future. Policy levers include steepening the decline in the annual carbon cap from 2021-2030 and revising the quantitative rules governing the Market Stability Reserve, which starting cutting the overall supply of allowances in January 2019. This process is expected to kick off after the summer, with the EC set to ramp up the 2030 emissions goal beyond the current 40% cut below 1990 levels to at least 50%.

3. US tubular steel prices slump amid falling oil and gas rig count

US OCTG PRICES FALL &100/ST AS DRILLING ACTIVITY PLUMMETS

What’s happening? The US oil and gas rig count fell by 22 in the week ended June 3, according to Enverus, and has fallen by 527, or 63%, since March 4. Since falling by $100/st from the start of March, US oil country tubular goods (OCTG) prices remained flat at the start of June, as recent supply cuts were at least partially offsetting the demand loss. The monthly S&P Global Platts domestic OCTG assessment remained flat June 1 at a midpoint of $800/st for June.

What’s next? The rapid recovery in crude prices in recent weeks to above the $30/b level has prompted some producers to scale back curtailment plans, suggesting the bottom may be in sight for rig count declines, which would help to support US OCTG pricing.

Go deeper: Podcast – US shale starts to return, but how sustainable is it?

4. Lower LNG deliveries to Europe could support hub prices

EUROPEAN LNG REGAS RATES FALL LATE MAY/EARLY JUNE

What’s happening? LNG regasification in Europe has begun to fall sharply from sustained highs over much of 2020, with regasification rates having dropped by 30% since the start of June compared to the May average. LNG regasification rates have been strong all year despite the low price environment, as there was little sign previously of supply cuts from market participants and Europe remained the destination of choice for LNG produced in the Atlantic Basin.

What’s next? European hub prices have been at a solid discount to prices in both Asia and North America in recent weeks, and with dozens of US LNG cargoes having been cancelled recently, shipping rates have eased lower, reducing the cost of moving the commodity over longer distances. If the trend for lower LNG supply to Europe persists over the summer, it could help lift European gas prices from their recent record lows.

Reporting by Philip Vahn, Daisy Xu, Frank Watson, Justine Coyne and Stuart Elliott

Content Type

Theme

Location

Language