S&P Dow Jones Indices — 22 Mar, 2021

A Guide to S&P Decrement Indices

By Tianyin Cheng and Izzy Wang

INTRODUCTION

Decrement indices have gained popularity as the underlying assets of equity-linked structured products in Europe and Asia. According to Structured Retail Products, among the 318 products across asset classes in France that matured or autocalled between April 2018 and March 2019, more than 32 were linked to decrement indices.

One of the reasons behind this recent popularity is the low interest rate environment that has emerged since the 2008 Global Financial Crisis, which has posed challenges for structured product issuers to design attractive products. This environment triggered a search for new underlying assets or strategies that might deliver cheaper optionality. Decrement indices aim to provide a solution to this challenge. S&P DJI has developed a flexible, transparent, and rules-based decrement index framework, which features:

Globally accepted, independent underlying indices such as the S&P 500®; Transparent methodology based on the S&P DJI decrement framework; and

Customization options in underlying index and decrement parameters.

How Decrement Indices Work

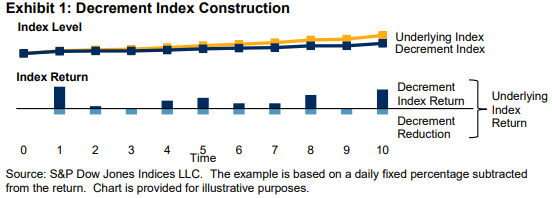

A decrement is an overlay applied to an underlying index. It is constructed by periodically deducting a predefined fee, either in the form of a fixed percentage or index points, from the underlying index (see Exhibit 1).

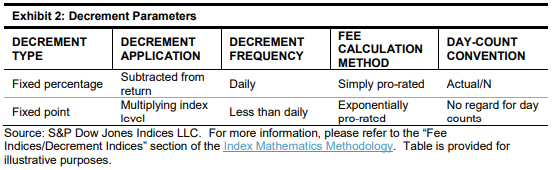

Given an underlying index, decrement indices can be calculated in different ways, depending on which parameters are chosen (see Exhibit 2). All the parameters can be customized. Decrement type and application are the most important parameters, as they primarily determine the amount of decrement deduction and how it is applied to an underlying index.

Decrement Type

The performance reduction applied to an underlying index can be either fixed percentage or fixed point. The logic of the fixed-percentage decrement is that dividend yield tends to be stable over the long term. During the past 10 years, the trailing 12-month dividend yield for the S&P 500 was relatively stable, at about 2%. On the other hand, a fixed-point deduction assumes a relatively high level of stability in dividend amounts in the short term, as companies are inclined to maintain more stable dividend policies compared with their earnings.