Crisis As Opportunity? COVID-19 Economic Recovery Policies Could Help or Hinder the Energy Transition

By Matthew Williams, Marion Amiot, Trevor D'Olier-Lees, Beth Ann Bovino, and Shaun Roache

Highlights

The European, U.S., and Chinese economies all reacted to the COVID-19 economic crisis with large monetary stimulus, but not all recovery policies will accelerate the energy transition.

The EU recovery fund, agreed in July, dedicated €225 billion to the energy transition, to be invested in the next three years.

The U.S. federal government has not provided any new support for green initiatives in stimulus measures to date beyond current tax incentives. The November election outcome will be pivotal for future climate change policies.

In China, warning signs abound that the energy transition has stalled as policy stimulus ripples through the economy even as a new commitment is made to achieve carbon neutrality by 2060.

The COVID-19 pandemic has taken a heavy economic toll on the global economy. We forecast global GDP will contract by 3.8% this year, compared with a 0.1% contraction in the 2009 global financial crisis. While all major economies reacted in the short term with large monetary stimulus, not all will accelerate the energy transition as a consequence. In the EU, which targets a net-zero carbon economy by 2050, policy support is significantly pushing renewables’ growth in Europe. The recovery fund approved by the European Commission in July 2020 dedicated €225 billion to the energy transition, to be invested in the next three years. However, China's transition to a low-energy-intensity economy, fueled increasingly by renewables, is likely to stall in 2020 and 2021 as policy stimulus ripples through the economy. In India, while the plunge in activity will reduce energy use, policymakers are unlikely to focus on the energy transition until the economy regains its footing. The U.S. federal government, meanwhile, has not provided any new support for green initiatives in stimulus measures to date beyond the current tax incentives. State mandates and ESG concerns continue to be the main impetus of U.S. installations so far, but the outcome of the November elections will be clearly a pivotal moment for policy decisions on climate change.

EU Countries Will Use Recovery Plans To Accelerate Toward Carbon Neutrality

Contributor: Marion Amiot, Senior Economist, S&P Global Ratings, + 44 20 7176 0128, marion.amiot@spglobal.com

The European economy has experienced its worst recession since World War II this year because of measures to contain the spread of COVID-19. Eurozone GDP was down 15% in the second quarter of 2020 year on year. The large scale of the crisis triggered unprecedented fiscal and monetary policy support. Governments are now focusing their efforts on speeding up the recovery through fiscal stimulus. And given the challenges of climate change, they have identified the energy transition as a key area to inject support.

Already before the crisis, EU countries had agreed to speed up the fight against climate change with the Green Deal set of policy initiatives aiming to make Europe climate-neutral by 2050, as well as the Green Taxonomy initiative. In spite of some pushback against environmental regulation from industries at the onset of the crisis, the EU now intends to use its post-pandemic recovery plan to reinforce its fight against climate change (see "The EU's Drive For Carbon Neutrality By 2050 Is Undeterred By COVID-19," published April 29, 2020, on RatingsDirect). In this plan, agreed in July, EU countries pledged that 30% of the Next Generation EU Fund's €750 billion fiscal plan and the EU multiannual budget would target climate-friendly projects. This is more than the 25% agreed in the Green Deal in January. This also means there are now more funds allocated to mitigating climate risk than before the crisis. The additional €225 billion coming from the recovery plan corresponds to 1.7% of 2019 EU GDP.

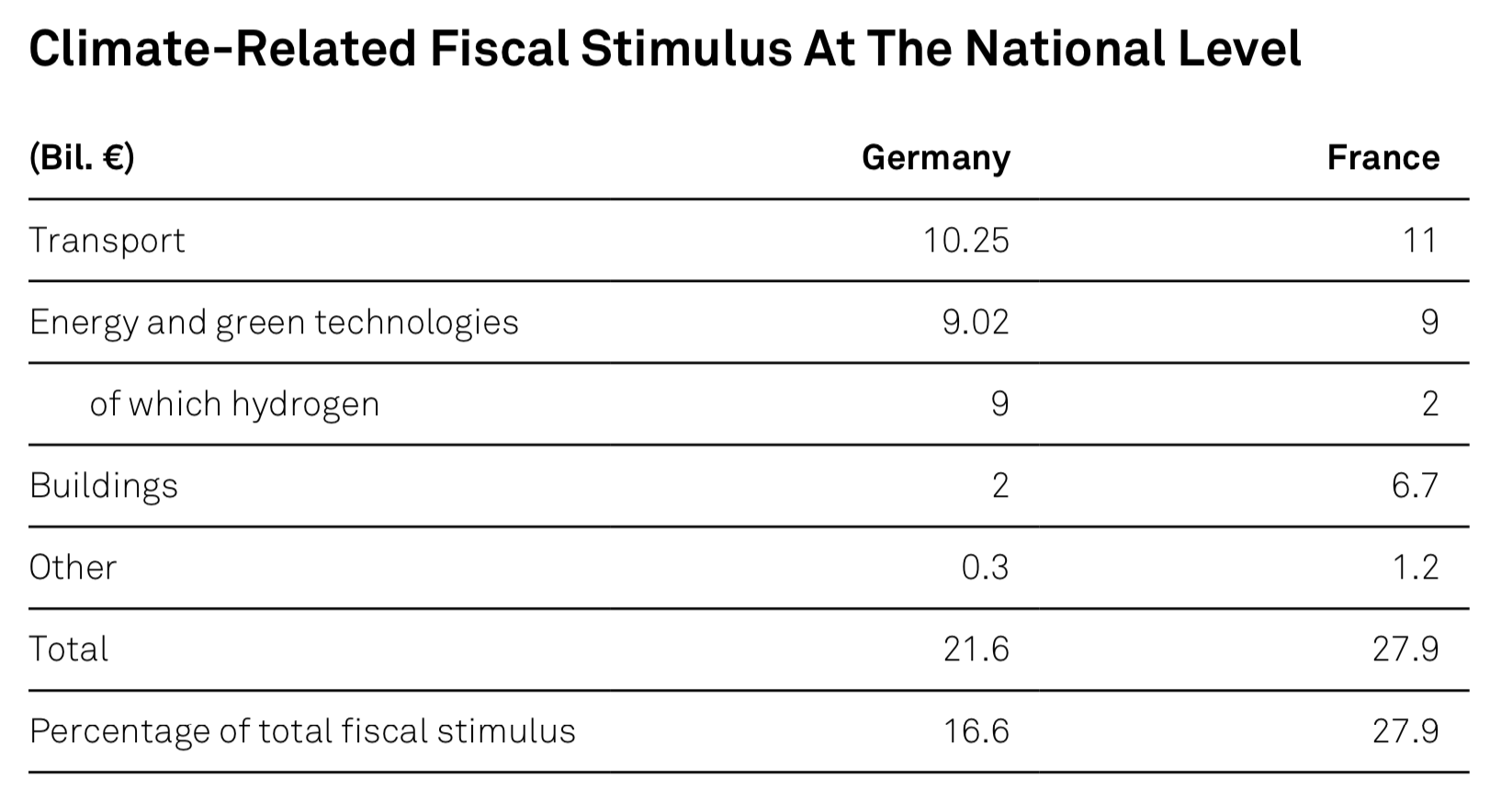

At the time of writing, most governments have yet to disclose the details of their fiscal stimulus, but from what has been announced so far, it seems that national governments will go beyond what the EU is asking in terms of greening the economy. Both France and Germany are allocating more resources to the ecological transition than will be made available to them through the EU’s Next Generation recovery fund. France is planning to spend €28 billion of its €100 billion on mitigating climate risk, Germany around €22 billion of its €130 billion (see table 1).

Although not all climate-friendly fiscal stimulus will go to the energy transition, it is one of the three main pillars of the EU climate-friendly investment strategy, alongside building improvements and transportation. This is because in order to reach the goal of carbon neutrality by 2050, EU countries are having to move to cleaner energy sources. Countries that are more reliant on coal for energy or generally produce less output per unit of CO2, such as Poland and the Czech Republic, are likely to spend more of climate-friendly investments in the energy transition. This difference is already visible between France and Germany, with France putting one-third of its climate-related investments into the energy transition and Germany one-half.

A key feature of fiscal stimulus during crisis times is its multiplier effect, which is larger than during normal times. In other words, every euro invested by governments in the energy transition will stimulate investments from the private sector in this domain. According to research by the IMF, this fiscal multiplier is around 2x after one year and about 3x after five years for the aggregate economy in the eurozone. Germany’s and France’s fiscal plans assume that around one-third of the climate-friendly EU investments will be invested to support the energy transition (around €75 billion). With a multiplier effect of 3x in five years, private funds attracted from public investments in greener energy would add up to €150 billion, giving significant support to the energy transition in the EU.

In The U.S., A Green Strategy For Recovery Is In The Balance

Contributors: Matthew Williams, Analyst, Emissions and Clean Energy, S&P Global Platts Analytics; Trevor D’Olier-Lees, Senior Director, S&P Global Ratings, (1) 212-438-7985, trevor.dolier-lees@spglobal.com; and Beth Ann Bovino, U.S. Chief Economist, S&P Global Ratings, (1) 212-438-1652; bethann.bovino@spglobal.com

The impact of the COVID-19 pandemic in the U.S. has been profound, with the number of cases topping over 6 million. More than one-half of the 22.2 million workers who lost their jobs remain unemployed, and the unemployment rate is over twice its pre-pandemic rate. Second-quarter GDP plunged by 31.7%, the largest drop since 1947. While the number of reported cases is lower than its July peak, regional hotspots still persist in some areas, such as the South and Midwest states. While we expect the U.S. economy to grow in the third quarter, we don’t expect it will reach pre-crisis GDP levels until fourth-quarter 2021. In environmental terms, the pandemic will cause the largest absolute reduction in CO2 emissions. Yet, absent policies that encourage green solutions, these emissions are set to rise again as the economy recovers. As such, the spotlight is on Washington in this pivotal election year, where economic recovery, job creation, and climate change are key topics of focus.

Green-flavored recovery policies as a response both to economic crisis and climate change concerns are not new for the U.S. In the midst of the Great Recession and public concerns foreshadowing the 2009 United Nations Framework Convention on Climate Change, then-President Barack Obama signed the American Recovery and Reinvestment Act (ARRA) into law in February 2009. The stimulus was estimated at $830 billion, of which $90 billion was allocated to environmental investments such as renewables, energy efficiency, and green infrastructure.

On the one hand, such policies have been shown to provide economic benefits. The International Energy Agency report “Green Stimulus after the 2008 crisis: Learning from successes and failures," published in June 2020, noted that "evidence suggests that the macroeconomic benefit of green stimulus programs ranged between 0.1% and 0.5% of GDP for around two years, depending on the size of the stimulus program". Furthermore, while accounting for only about 10% of the ARRA’s funding, the tax policies and grants provided under the act were instrumental in accelerating the deployment of photovoltaic (PV) solar and onshore wind, vital for the overall energy transition.

On the other hand, given the capital-intensive nature of the energy sector, there is some debate on the trade-off between near-term GDP boosts and near-term job growth. Priorities in Washington this time around may center more on near-term job creation, which could drive stimulus funds to support sectors like health care and transportation. Furthermore, the ARRA had some unintended consequences in that Chinese manufacturers scaled up solar wafer and module manufacturing in response to strong policy-driven pipelines, which in turn lowered prices. This led to closures of some U.S. PV businesses, which were unable to compete.

There are stark contrasts between the two candidates in the forthcoming presidential elections in terms of infrastructure policy and stimulus proposals. In July, Democrat Joe Biden updated his existing climate plan, calling for $2 trillion in spending for sustainable infrastructure over four years, including roadways, buildings, broadband, and clean energy. While this spending would boost economic output, the implementation of emissions and clean energy standards to complement the spending would be more effective in reducing emissions than spending alone. The plan advocates for standards that target a carbon-free power sector by 2035 and net-zero emissions for all new commercial buildings by 2030. Federal legislation would be required to enact these specific policies and a simple 51-seat Democratic majority in the Senate will likely not be enough for some of Biden’s more ambitious proposals. Democratic senators who represent carbon-intensive states might be more reluctant to support legislation that incentivizes clean energy over traditional fossil fuels. The larger the majority, the easier time his administration will have enacting its platform.

In the case of a Trump second term, the U.S. would expect a continued push for tax cuts and deregulation alongside further attempts to streamline the infrastructure permitting process. However, a platform consisting mainly of tax breaks and deregulation may not necessarily be enough to overturn the decline in infrastructure investments in general--both within the energy and non-energy sectors--because tax equity availability has become scarce.

Post-COVID Recovery In China Means More Energy, More Carbon

Contributor: Shaun Roache, Asia-Pacific Chief Economist, S&P Global Ratings, (65) 6597-6137; shaun.roache@spglobal.com

The two economies that will shape the way that Asia-Pacific’s COVID-19 recovery affects the global energy transition are China and India. We expect China's transition to a low-energy-intensity economy, fueled increasingly by renewables, to stall in 2020 and 2021 as policy stimulus ripples through the economy. Still, President Xi has recently signaled a bold intention for China to become carbon neutral by 2060. India’s economy has been hit by an enormous shock that will impose large, permanent damage. While the plunge in activity will reduce energy use, policymakers are unlikely to focus on energy transition until the economy regains its footing.

Focusing on China, we expect that the energy intensity of China's economy will be little changed this year compared to 2019. Based on what we know for the first eight months of the year, total consumption of energy has edged higher compared with the same period in 2019. This compares with our estimate of real GDP, which is about 1% lower for the same period, causing the ratio of energy to GDP to edge up. Official estimates also suggest a slight uptick in energy intensity.

China's progress toward an energy mix less reliant on fossil fuels has also stalled since COVID-19 struck. Renewables are contributing more to power generation, aided by exceptionally heavy rainfall and hydro and the rush for installation of wind and solar power capacities in the run-up to grid parity. However, rising industrial energy use offsets this effect. This is especially true for steel firms, which are heavy coal users.

China’s policy stimulus throws trend off course

The stimulus of 2020 is not an exact replay of 2009--it is certainly smaller--but there are echoes of the past. The most important is the reliance on debt-financed infrastructure investment to support the economy. Investment in roads, rail, and airports consumes a lot of steel, cement, and bulk commodities, which means more energy use, especially from fossil fuels.

S&P Global Platts estimates that new airport and railway projects approved this year, combined with projects approved in 2016-2019 which are now proceeding as access to funding has been eased this year, should contribute to about 23 million metric tons of Chinese steel demand in 2020--an almost one-quarter rise on 2019. Overall infrastructure investment, including investment in power generation, will be up by about two percentage points of GDP compared with the five-year average through 2019.

This infrastructure push, together with a buoyant post-COVID property market and a pick-up in auto production, has meant that steel, other metals, and raw materials have led the manufacturing recovery. Industry accounts for more than 40% of total coal consumption, including coal used in electricity generation. Steel and non-metallic minerals production alone account for about 15%, where it is mainly used as a fuel and reductant in cement kilns and blast furnaces.

Coal comes back

CChina is edging back towards coal. In 2014, during a time of overcapacity and large financial losses in China’s coal sector, the National Energy Agency (NEA) began restricting local governments from adding to new coal capacity over a three-year horizon. The NEA has eased these restrictions for the past three years and again in 2020. Partly in response, local governments are approving more coal power projects: about 19.7 gigawatt (GW) of capacity was approved in first-half 2020, the highest rate in recent years.

The National Development and Reform Commission (NDRC), an economic planning body, and the NEA still aim to cap total installed coal power capacity at 1,100GW by the end of 2020. Given new capacity coming on stream, this would mean shuttering inefficient capacity of 7.33GW nationwide this year, a target which is lower than the 8.66GW set in 2019. It’s uncertain if the regulator may lift the cap on coal power, as suggested by the industry association, to about 1,300GW by 2030 to meet demand.

It is not all coal, though. In early September, the State Council approved two new nuclear reactors that should be ready in 2025 and 2026. Investments in renewable energy, especially wind power, also remain strong in the run-up to the rollout of grid-price parity, which will remove subsidies for utility-type solar and onshore wind-power projects from 2021. China has been gradually phasing out the subsidies for renewables after robust growth during the 13th five-year plan. In the first half of 2020, investment in the generation sector grew 73% year on year, driven by a 190% surge in wind power. Wind accounts for just over 6% of power generation so far in 2020.

New infrastructure holds promise in getting China back on track

China has committed to becoming carbon neutral by 2060. We expect the plan to call for more investment in infrastructure to eventually help in lowering energy intensity and reduce carbon emissions. These investments include high-speed rail, data centers, and rapid 5G rollout, all of which may foster more efficient private transport and more digitalization. While this will boost demand for electricity, a rising share of renewables in power generation should result in less fossil fuel consumption in the power sector. So far this year, 25 province-level regions, accounting for over 90% of China’s GDP, have included new infrastructure in their government work reports for 2020, although it is likely to remain a small share of overall infrastructure spending.

Energy security over energy transition?

China's strategic response to less predictable geopolitics will move energy security near the top of the policy agenda. China imports over 70% and 43% of its crude oil and natural gas, respectively. About 90% of oil imports arrive by sea and much of this traverses through the potential chokepoint of the Malacca Strait and the South China Sea. Digitalization means more electricity demand and coal is a reliable and cheap source of primary energy for power generation. Indeed, China is rich in coal with about 13% of global reserves. We expect policies promoting the use of more renewables, but it's too early to count coal out.

Warnings signs abound that the energy transition has stalled in the country, but this must be considered alongside its new commitment to achieve carbon neutrality in 2060. We will learn more when the 14th five-year plan is released in March 2021.

This report does not constitute a rating action.

Content Type

Theme

Location

Language