S&P Dow Jones Indices — 9 Jun, 2020

Gold’s Time to Shine

This article is reprinted from the Indexology blog of S&P Dow Jones Indices.

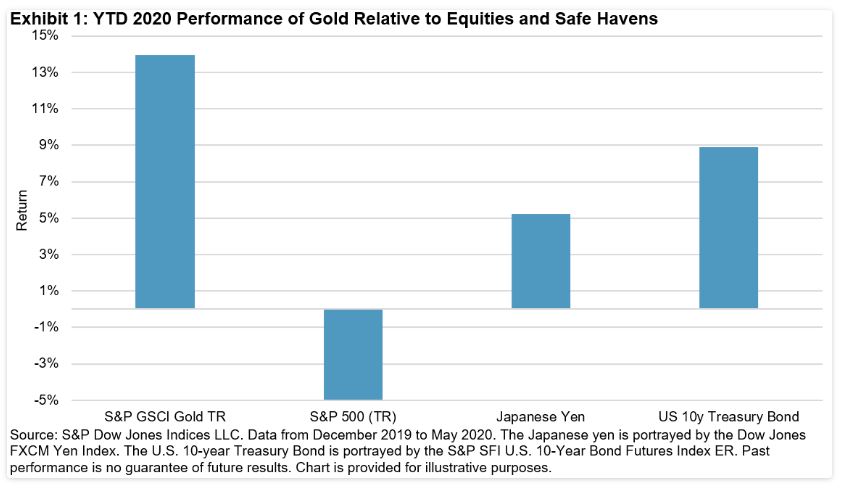

The first half of 2020 has been gold’s time to shine. The double-digit YTD gains outpaced equities and other safe-haven assets during these uncertain recessionary times. As of May 29, 2020, the S&P GSCI Gold was up 13.94% YTD. Unprecedented global fiscal and monetary stimulus measures have significantly increased sovereign debt levels, leading to concerns of currency devaluation. Historically, such environments have been constructive for gold as a globally recognized store of value. Low to negative global real yields and gold’s low correlation to other assets add to the positive catalysts in the current environment.

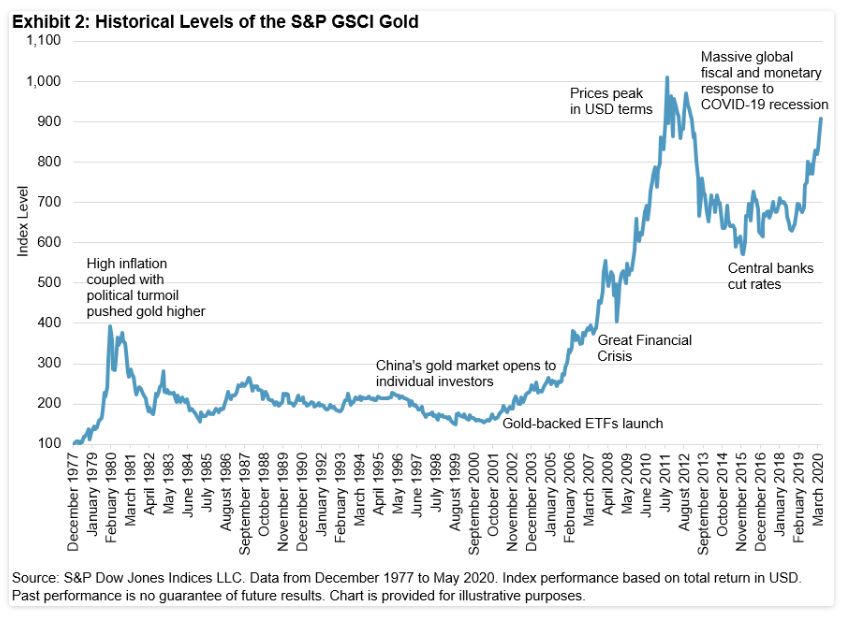

It has not been an entirely smooth ride this year, with some volatility along gold’s path to outperformance, as was highlighted in a blog by Fiona Boal. A rhyming pattern appeared along the lines of the 2008 during the Global Financial Crisis, in which a need for liquidity forced market participants to sell gold holdings before reloading and returning gold back to an upward trend (see Exhibit 2).

This year’s backdrop of the potential for a pandemic-induced global recession comes as the China-U.S. trade war restarts. There is a deglobalization of supply chains, creating a less-inclusive global economy. Uncertainty in the near term seems to be the only certainty in 2020.

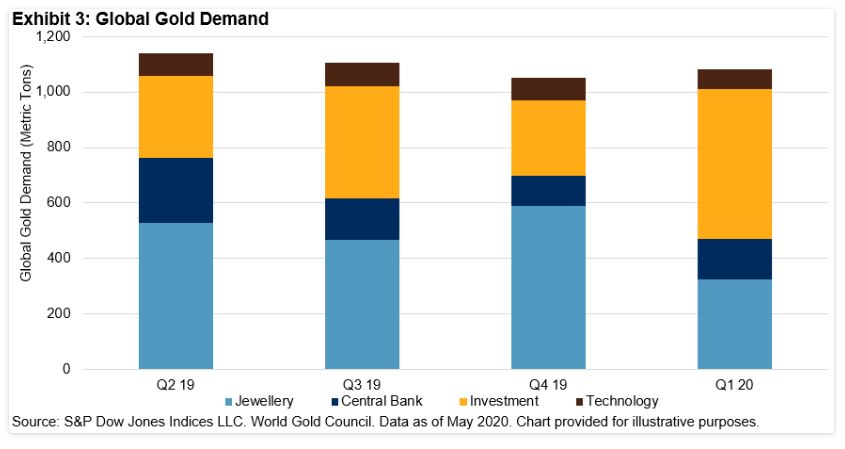

This year is also different from a demand perspective as it relates to gold. According to the World Gold Council, first quarter 2020 jewelry demand was the lowest in over 10 years, while first quarter investment demand was the highest since the first quarter of 2016 (see Exhibit 3). Preliminary data suggests the second quarter of 2020 is shaping up to be a continuation of this trend, with reduced consumer spending on non-essential jewelry purchases combined with record flows into gold exchange-traded products.

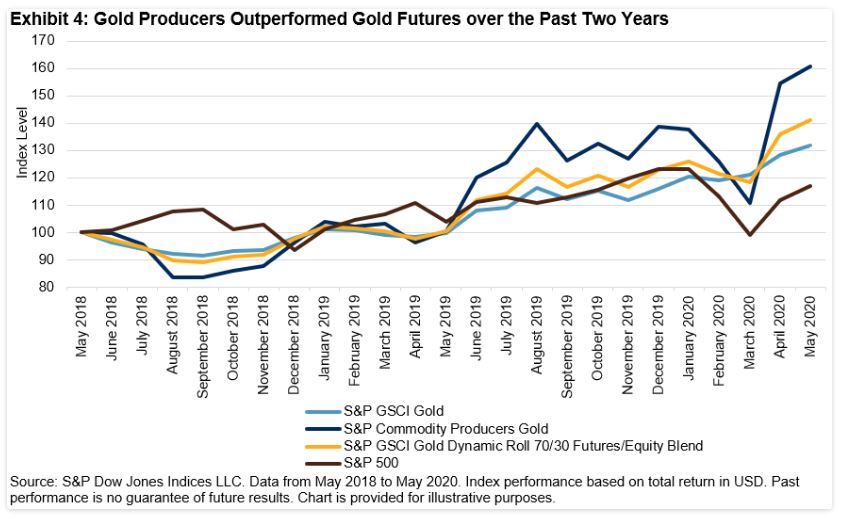

As of May 29, 2020, the S&P Commodity Producers Gold Index returned 16% YTD. The environment is particularly attractive for these companies, with potential M&A activity ahead due to fewer large-scale discoveries of gold deposits. Once discovered, it can take 15 years to reach successful ore production. Fewer discoveries and near-term mine suspensions by governments due to COVID-19 make the precious metal that much scarcer. There was a fifth consecutive quarterly decline in global gold mining prior to any of the recent pandemic-related shutdowns.

In 2019, S&P Dow Jones Indices launched a 70% futures and 30% gold equities blended index, the S&P GSCI Gold Dynamic Roll 70/30 Futures/Equities Blend, to allow participation in the gold market across asset classes. We also offer many additional gold-related indices to meet the needs of market participants. To learn more, visit https://spdji.com/landing/investment-themes/commodities.

Content Type

Location

Language