S&P Global — 9 Oct, 2020

Daily Update: October 9, 2020

By S&P Global

Subscribe on LinkedIn to be notified of each new Daily Update—a curated selection of essential intelligence on financial markets and the global economy from S&P Global.

The Organization of the Petroleum Exporting Countries, known as OPEC, believes oil demand will increase through 2040. Their outlook is at odds with market participants who project oil demand could peak as early as this decade.

The intergovernmental group forecasts oil demand to grow 20.5% in the next four decades, to 109.3 million barrels a day by 2040, when global oil demand will peak, according to its annual World Oil Outlook. OPEC anticipates that demand will gradually decline in subsequent years, to 109.1 million barrels a day in 2045.

This is the first time OPEC has forecast when oil demand will top out, according to S&P Global Platts.

As oil demand “grow[s] at relatively healthy rates” through 2045, OPEC sees oil accounting for more than 27% of the world’s energy mix—taking greater space than gas’s 25% share and coal’s 20%.

"With a longer perspective, we’ll see the growing importance of renewables and natural gas in meeting future demand," OPEC Secretary General Mohammed Barkindo said in the report. "Nonetheless, oil will continue to account for the largest share of the energy mix by 2045, providing a stable foundation for addressing global energy needs for years to come.”

Other market participants have different outlooks. Energy multinational BP modeled three scenarios where the market never recovers its pre-pandemic activity. In BP’s “business as usual” scenario, where governments, technologies, and societal preferences continue to evolve as they have done so in the recent past, oil demand peaks and plateaus in the early 2020s. The consultancy DNV GL believes that despite the world’s struggle to combat climate change, global oil demand may have peaked last year, ahead of the pandemic.

"We are not on the right track yet," Liv Hovem, DNV GL's CEO of oil and gas, told S&P Global Platts of the global community’s progress in limiting global warming to 2 degrees Celsius. “We need 8% emission reductions every year, similar to 2020, up to 2050, in order to reach the 1.5-degree target. COVID has given us 1-2 years more to solve the problem, that is all."

In contrast, the S&P Global Energy Transition Research Lab believes peak oil could come in 2035 as the pandemic permanently changes long-term demand.

Still, while overall oil consumption is unlikely to return to pre-crisis levels until late-2022, the current weakened demand isn’t meaningful enough to substantially accelerate oil’s peak.

“For oil demand to peak by 2025, drastic changes would need to occur to business and consumer behavior, including near full adoption of working from home, reshoring of supply chains, and widespread electrification of road transportation,” the Lab said in a recent report.

Today is Friday, October 9, 2020, and here is today’s essential intelligence.

Uncertainty in the Global Economy

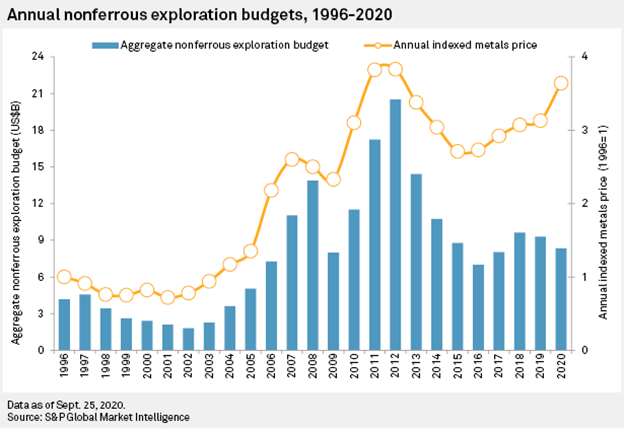

COVID Restrictions Push Exploration Budgets Down 11% In 2020

Newly released 2020 global exploration budget data from S&P Global Market Intelligence's Corporate Exploration Strategies, or CES, series shows that exploration sector optimism that began to appear in the second half of 2019 was snuffed out by the COVID-19 pandemic, resulting in a second year of decreasing budgets in 2020. Preliminary analysis of budgets gathered for 2020 exploration shows that the estimate of the total annual global nonferrous exploration budget has fallen 11% year over year to $8.7 billion from $9.8 billion in 2019.

—Read the full article from S&P Global Market Intelligence

Turning Over A New Lease: Uncertainty Looms Over Listed Retail Landlords' Income

If there were any doubts as to how listed retail landlords felt about turnover-based rents, European mall giants Unibail-Rodamco-Westfield and Klépierre made sure to dispel them during their first-half earnings calls in August. Within hours of each other, Unibail CEO Christophe Cuvillier and Unibail CEO Christophe Cuvillier made it unmistakably clear to their occupiers and the wider European retail sector that, despite the damage COVID-19 lockdowns had inflicted on many tenants, their companies would not be forced into leases based purely on turnover.

—Read the full article from S&P Global Market Intelligence

Biden Tax Plan Could Mean Increased Tax Liabilities For Insurance Underwriters

Insurance companies may face higher tax liabilities in the future should former Vice President Joe Biden win the upcoming presidential election and get his proposed changes to the corporate tax structure passed through Congress, according to an S&P Global Market Intelligence analysis. The Democratic presidential nominee's tax plan calls for raising the corporate tax rate to 28%, from the 21% rate established by the 2017 Republican tax overhaul, as well as doubling the tax rate to 21% from 10.5% on Global Intangible Low-Tax Income, or GILTI, earned by foreign subsidiaries of U.S. companies.

—Read the full article from S&P Global Market Intelligence

The Future of Credit

From Crisis To Crisis: A Lookback At Actual Recoveries And Recovery Ratings From The Great Recession To The Pandemic

The sudden recession and its impact on credit quality has been unprecedented in speed and depth--a deterioration not triggered by an asset pricing bubble or fundamental economic factors, but by a global health pandemic. The impact of COVID-19 containment measures, plus disruptions in the oil markets, has caused a sharp drop in revenues and earnings for companies in consumer-facing sectors, and the resulting recession has affected companies across the board.

—Read the full report from S&P Global Ratings

Inside Global ABCP: Issuance Growth Tempered As Economic Recovery Takes Shape

Asset-backed commercial paper (ABCP) outstanding in the U.S. peaked between March and April as alternative funding sources for liquidity became scarce and the term market was relatively inaccessible during that time. However, as some market liquidity returned, volumes have decreased from this peak. We expect growth in new seller activity to improve and issuance from recently launched conduits to gain momentum amid COVID-19-related uncertainties. In Europe, the Middle East, and Africa (EMEA), ABCP outstanding declined in the first six months, although committed funding amounts increased, indicating that long-term interest remains positive.

—Read the full report from S&P Global Ratings

University Challenge: Will International Students Keep A Distance From English Universities?

The pandemic is likely to disrupt the enrollment of overseas students, which would tighten the screws on English universities' finances. As reported in April 2020, S&P Global Ratings expects the COVID-19 pandemic to slash enrollment figures of international students for academic year 2020. Over the past years, as government grants steadily fell, English universities turned to international students to sustain their revenue and performance. They will need take decisive action to address the financial effects of a dearth of overseas student enrollments. Maintaining performance across the sector will rely on individual management teams adjusting their cost structures, while preserving the quality of teaching.

—Read the full report from S&P Global Ratings

U.S. High-Yield Issuance Blasts Past Prior Years to Set New Record

U.S. high-yield issuance reached $345.6 billion for 2020 through Oct. 7, marking a new annual record for the asset class, according to LCD. The figure topples 2012's $344.8 billion from its long-standing position in the top slot. Year-to-date volume is currently outpacing 2019's full-year sum of $272.6 billion by 21%.

—Read the full article from S&P Global Market Intelligence

Listen: Take Notes: U.S. Structured Finance Issuance Volume Picks Up The Pace

Take Notes hosts Tom Schopflocher and James Manzi give an update on U.S. structured finance issuance. Issuance returned to form in September, reaching $54 billion, the highest monthly total so far in the year. While 2020 year-to-date issuance is still down 21% year over year, it looks like the annual total will eclipse S&P Global Ratings’ revised midyear forecast.

—Listen and subscribe to Take Notes, a podcast from S&P Global Ratings

ESG in the Time of COVID-19

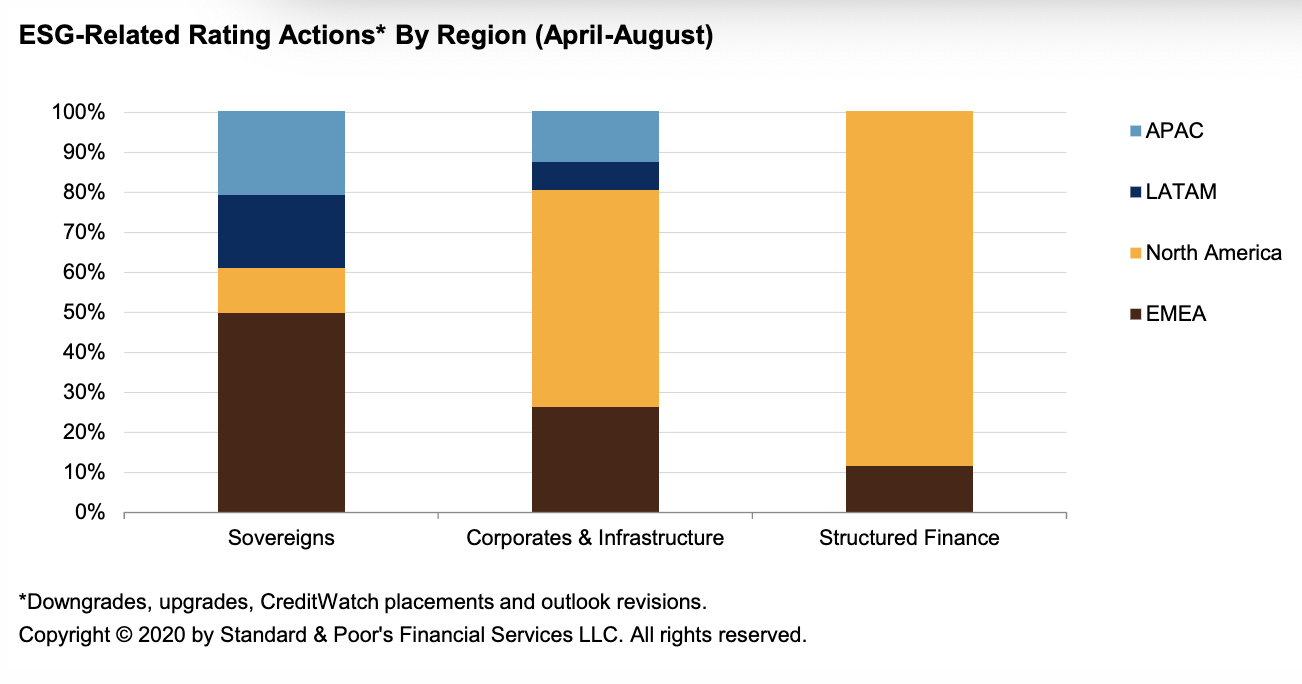

The ESG Pulse: Better Climate Data Could Provide Foundation For Understanding Physical Risks

Total environmental, social, and governance (ESG)-related rating actions reached 1,945 during April-August (of which 666 were downgrades). Of the 296 downgrades in July-August, 199 related to CreditWatch resolutions on U.S. commercial mortgage-backed securities (CMBS) transactions. These structured finance rating actions reflected S&P Global Ratings’ revised valuations and credit views on the underlying assets (malls and hotels).

—Read the full report from S&P Global Ratings

Greenhouse Gas and Gold Mines Nearly 1 Ton of CO2 Emitted per Ounce of Gold Produced in 2019

Gold mines emitted on average 0.8 tonnes of CO2 equivalent for every ounce of gold that was produced in 2019; however, stark differences exist both regionally and across open pit versus underground mining methods.

—Read the full article from S&P Global Market Intelligence

Net Zero Emissions Targets Create Investment Opportunities – Mark Carney

Investors are set to benefit as most companies are forced to readjust their strategies, and consider how they will achieve net-zero emissions post-COVID-19, UN climate change envoy Mark Carney told listeners at the virtual British Pvt. Equity and Venture Capital Association Ltd. summit on Oct. 8. Carney, who is the U.K.'s finance adviser to COP26, the next UN Climate Change Conference to be held in Glasgow in 2021, said countries' pledge to get to net zero emissions is a great opportunity. "Society has set the objective. Capitalism then says, 'OK, you've got an issue, you've got an objective, we'll find you the solution.'"

—Read the full article from S&P Global Market Intelligence

EU Parliament Backs 2050 Climate Neutral Law

The European Parliament adopted its negotiating mandate on a proposed EU climate law Oct. 7, seeking carbon neutrality by 2050 and confirming amendments it made to raise the bloc's nearer-term 2030 emissions reduction target to 60% below 1990 levels, the parliament said Oct. 8.

—Read the full article from S&P Global Platts

UK Renewables Claim 44.6% Market Share In Q2 As Offshore Load Factor Rises

Renewables' share of UK electricity generation climbed to 44.6% in the second quarter, up nine percentage points on the year, government statistics showed Oct. 8. The record quarter was largely due to a drop in total electricity generation from non-renewable sources as the coronavirus lockdown hit overall demand, pulling gas and coal units off the system.

—Read the full article from S&P Global Platts

Analysis: Asia's Maiden Hydrogen Trade Flow Routes To Feature Australia, Northeast Asia

Asia may witness some of the initial hydrogen trade flows from Australia to Japan and South Korea, the two countries in the region that have rolled out long-term plans for the clean fuel, which analysts and market participants said have to be largely met through imports. Even though the actual trade flows may be years away and there are multiple hurdles to clear, energy traders and analysts told S&P Global Platts that Australia's ambition to be a key hydrogen export hub would mean that Japan and South Korea would be aiming to source a substantial portion of their needs from the Pacific region.

—Read the full article from S&P Global Platts

US stock volatility spikes after Trump calls off stimulus talks – risk monitor

Another turbulent day in U.S. politics caused the stock market's volatility gauge to spike again Oct. 6, after President Donald Trump tweeted that he was ruling out another stimulus package until after the Nov. 3 election. The CBOE Volatility Index, or VIX, jumped from 28.0 to 29.5, its highest level since Sept. 10. A reading of 30.0, a historically high level, has preceded average daily movement of 1.3% in the S&P 500.

—Read the full article from S&P Global Market Intelligence

Columbia Gas Settlement Tackles Safety, Climate Change, Environmental Justice

A settlement over the 2018 Merrimack Valley disaster seeks not only to facilitate a $1.1 billion takeover of Columbia Gas of Massachusetts, but also aims to advance the state's climate and social justice agenda.

—Read the full article from S&P Global Market Intelligence

The Future of Energy & Commodities

Watch: Market Movers Asia, Oct. 5-9: Asian refiners eye Middle East crude OSPs, Trump's COVID-19 recovery

The highlights in Asia this week on S&P Global Platts Market Movers, with Digital Editor Barbara Lorenzo Caluag: Asian refiners expect slight increase in Middle East crude prices; progress of Trump's COVID-19 recovery to dominate market direction; fundamentals in Asia's transportation fuel markets seen muted in Q4; benchmark Glencore-Tohoku coal price talks seen bumpy; and India extends 5% GST waiver on export freight.

—Watch and share this Market Movers video from S&P Global Platts

OPEC Predicts Wave Of Oil Refinery Consolidation As Capacity Will Outpace Demand

The coronavirus pandemic will slow the pace of refinery expansions, but the market will still see significant overcapacity in the years ahead, OPEC said Oct. 8 in its latest long-term outlook. OPEC expects about 3.8 million b/d of new refining capacity to come online by 2022, it said in its World Oil Outlook. While that growth will slow down significantly after that, the market will not require that much capacity, OPEC said, with about 2.5 million b/d of refinery closures expected by 2025, mostly in Europe, the US and Canada.

—Read the full article from S&P Global Platts

ANALYSIS: Asia-Pacific Tankers' Freight Outlook Weak For Q4 On Poor Demand

Asia-Pacific tankers' freight will likely remain weak during the final quarter of 2020 due to subdued demand and even the usual Northern Hemisphere winter and floating storage is unlikely to provide significant support. According to market participants S&P Global Platts spoke with in Seoul, Tokyo, Singapore, Mumbai, Oslo and Copenhagen, the current quarter looks challenging for both dirty and clean tankers freight. This year, the odds are stacked up against a strong winter market, though a few abnormal disruptions to seaborne logistics will provide volatility, said Copenhagen-based Peter Sand, BIMCO's Chief Shipping Analyst.

—Read the full article from S&P Global Platts

Analysis: Singapore Bunkering Standards Usher In Era Of Transparency, Cost Savings

Singapore's two new bunkering standards -- Singapore Standard 660:2020 and Technical Reference 80:2020 -- launched on Oct. 7 and related to mass flow meters will increase transparency and provide further quality assurance in the maritime industry, which is already reaping the benefits of productivity enhancements and cost savings after the implementation of TR 48 in mid-2016, industry sources said.

—Read the full article from S&P Global Platts

Listen: U.S. Crude Exports Face Reversal Of Fortune Amid COVID-19 Pandemic

With global demand destruction and COVID-19 continuing to impact US production, the expected trajectory of US crude exports is vastly different than just a few months ago. Before the pandemic, S&P Global Platts Analytics expected US crude exports to end 2020 at a run rate of nearly 4 million b/d, rising past 6 million b/d by the mid-2020s, but with demand loss for now putting a cap on WTI at about $40/b, Analytics now expects exports to fall below 2 million b/d by mid-2021.

—Listen and subscribe to Oil Markets, a podcast from S&P Global Platts

Written and compiled by Molly Mintz.

Content Type

Location

Language