S&P Global — 2 May, 2022 — Global

Daily Update: May 2, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Slower Growth In China Poses Risks To Global Economy

China’s slower economic growth may signal trouble for global GDP in the months ahead.

Stringent coronavirus lockdowns in Shanghai and elsewhere in China have made manufacturing activity sluggish, depressed business sentiment, hurt consumers’ confidence and spending, sent the renminbi plunging, constricted energy imports and exports alongside diminished demand, and risked supply chain disruptions worldwide. While China was the first country to recover from the first wave, the resurgence of COVID cases in the country and Beijing’s strict “zero-tolerance” approach add uncertainty to its outlook. China’s National Bureau of Statistics reported first-quarter GDP growth of 4.8%. But the International Monetary Fund cut its full-year growth forecast for China to 4.4%—far below the government’s target of 5.5% that S&P Global Economics, which expects GDP growth in China just shy of 5%, already perceived as ambitious.

S&P Global Ratings believes the Shanghai government can overcome the lockdown paralysis, but expects China’s zero-COVID approach will bring sharp implications for its technology and automotive industries. Meanwhile, the country’s slowing GDP growth and the effects of lockdowns, among other factors, are raising risks to the ratings on China's government-related entities. Slower growth in China would have ripple effects not only across the country itself and Asia-Pacific region—but also on global GDP overall.

“A sharper-than-expected slowdown in China remains a key risk to growth for emerging markets (EMs), but its impact would depend on the drivers of such slowdown, as well as the ensuing policy reaction,” S&P Global Ratings Latin America Senior Economist Elijah Oliveros-Rosen and Asia-Pacific Economist Vishrut Rana said in research published last week. “Weaker growth in China would have important implications beyond EMs, given the size of the economy and its impact on global trade and global financial conditions, which would also indirectly affect growth in EMs through those channels. A Chinese economic slowdown could be consumption-driven, investment-driven, or both (a hard landing), and each of those would have different implications for EMs and the rest of the world.”

The sluggish economic growth is already affecting financial market participants—testing the resilience of Chinese banks, which suffered lower profit growth in the first quarter and now amid current conditions may see their earnings potential hinge on their ability to increase loans, according to S&P Global Market Intelligence. Reporting a 21% year-over-year decline in first-quarter revenue to HK$4.7 billion on April 27, the stock exchange operator Hong Kong Exchanges said it expects trading to remain muted and acknowledged how it is “not immune to global market sentiment.”

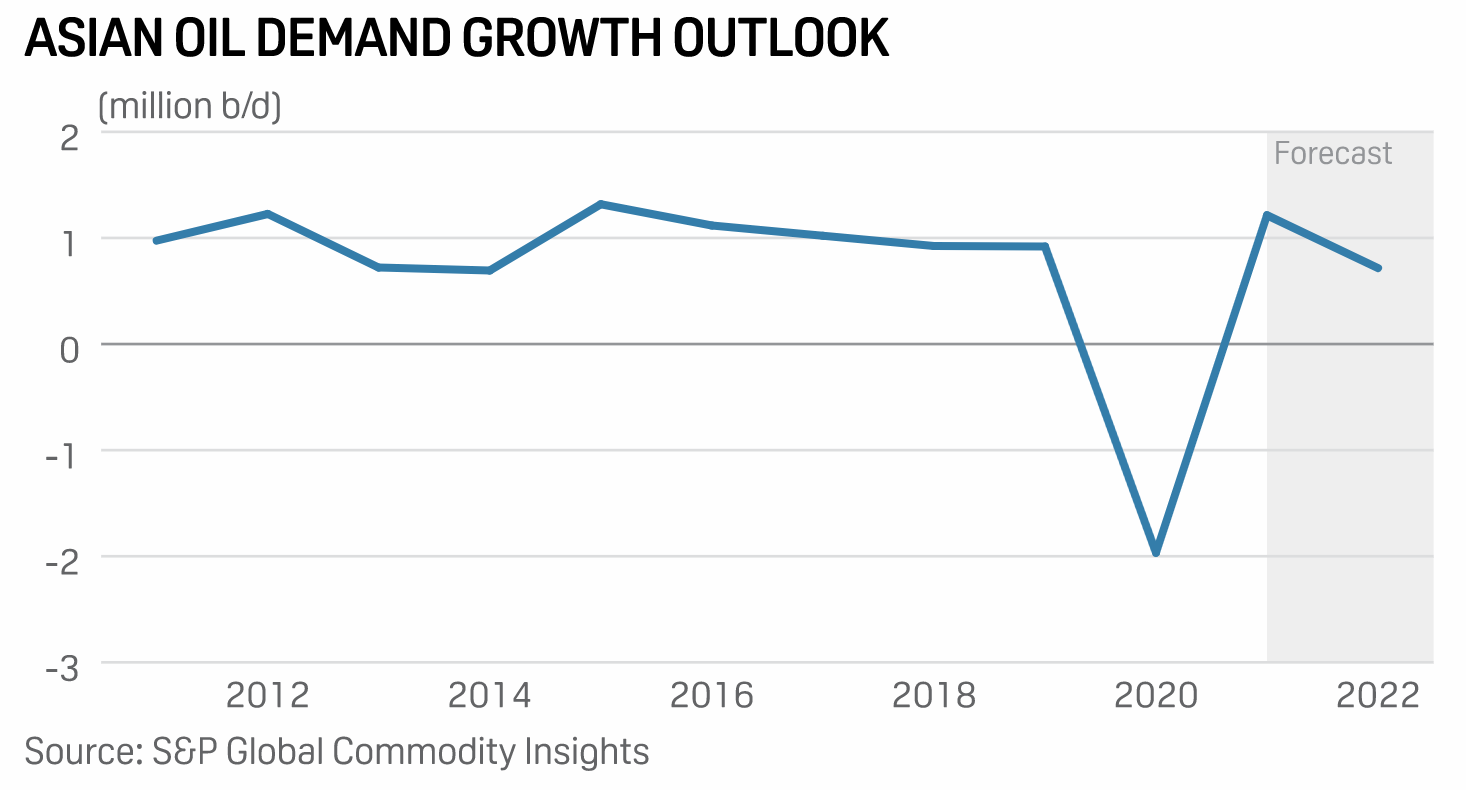

China's ongoing COVID crisis is one of the key events driving commodity markets, according to S&P Global Commodity Insights. The lockdowns in Shanghai, which is the world’s largest production hub, have stalled containerized exports and compounded port congestion. China’s steel inventories hit 13-year highs, but lockdowns continue to disrupt supply chains and logistics. In response to China’s aggressive approach to its COVID surge, analysts believe Asia's overall oil demand outlook for 2022 is starting to darken, and China's oil demand growth may, in a best-case scenario, remain flat this year with a possibility of slipping into negative territory. An April 26 S&P Global Commodity Insights analysis found that China's crude throughput likely reached a two-year low in April after state and independent refiners slashed their runs.

“We have revised down China's oil demand to almost no growth this year, owing to the demand loss in Q2,” Wang Zhuwei, S&P Global Commodity Insights' Asia oil analytics manager, said. “It remains uncertain whether demand loss in the se will be compensated by demand recovery in [the second half of the year]. That will increase the possibility of further downward revisions.”

Today is Monday, May 2, 2022, and here is today’s essential intelligence.

Written by Molly Mintz.

Economy

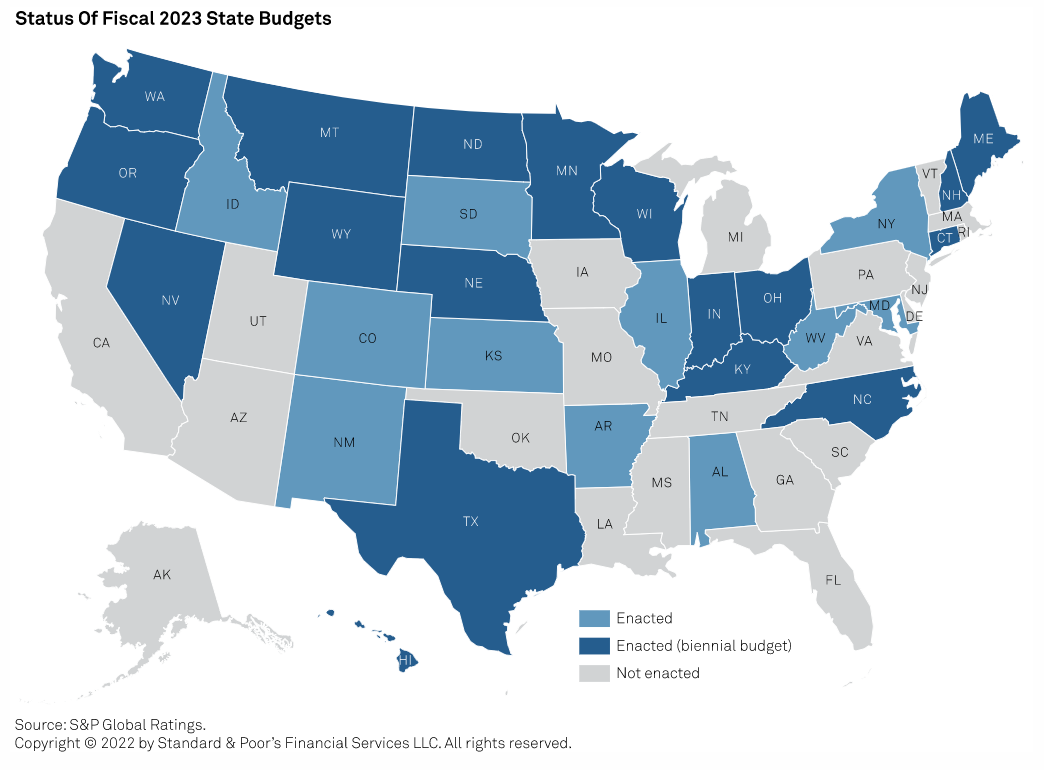

Slower Growth Ahead: Revenue Surpluses Boost U.S. State Budget Flexibility, For Now

In S&P Global Ratings' view, state budgets have benefited over the past year from an economic environment boosted by federal stimulus injections, low bond interest rates, and pent-up consumer demand. Accordingly, state revenues have largely been reported as better than forecast and have remained strong even in the wake of generationally high inflation levels. This legislative cycle, states are choosing how to direct excess revenues. Most have already allocated the received American Rescue Plant Act (ARPA) funds in a structurally balanced manner, allowing for state budget priorities to focus on items other than the critical infrastructure projects funded by ARPA.

—Read the full report from S&P Global Ratings

Access more insights on the global economy >

Capital Markets

Private Equity Expanding To Renewable Tech Beyond Wind, Solar

Private equity firms invested $21.5 billion in the U.S. renewable energy sector in 2021, with over $6 billion of capital flowing to wind and solar projects, according to a recent report by the American Investment Council. Over the past decade, private capital has "sponsored more than 1,000 U.S. clean-tech companies, investing almost $150 billion," according to the American Investment Council, a lobbying and research organization representing the private equity and growth capital investment industry. Those investments include conventional renewables like wind and solar, along with agricultural technology such as sustainable food management, waste management, and water management.

—Read the full article from S&P Global Market Intelligence

Access more insights on capital markets >

Global Trade

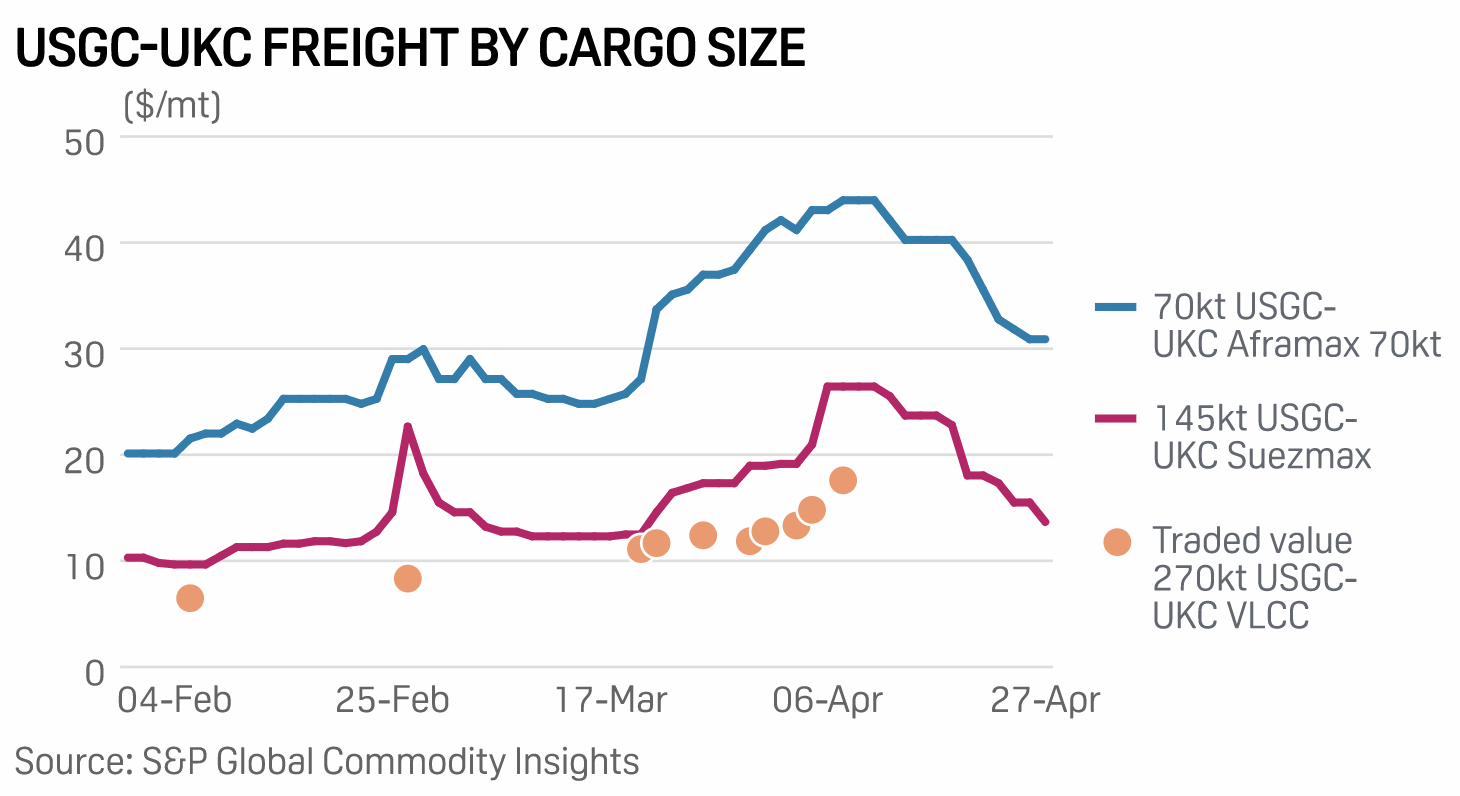

Trans-Atlantic Crude Export Drive Prompts Tanker Class Intertrade, Sinks Rates

Increased competition between Suezmax and Aframax tankers on the U.S. Gulf Coast-Transatlantic runs prompted rates to fall 48.3% and 29.3% from the crude export-driven freight spike seen in early April. Charterers looking to cover trans-Atlantic crude stems were heard to have been looking at both Suezmax and Aframax options, all of which ultimately chose a Suezmax vessel and fixed at Worldscale 80. "Suezmaxes are taking the cake on USGC inquiry," a shipbroker said. Repsol placed the Maran Helen on subjects for a USGC-Spain run, loading May 10-12; Vitol placed the Selena on subjects for a USGC-TA run, loading May 5-7; and Suncor placed the Navion Gothenburg on subjects for a USGC-TA run, loading May 7-8.

—Read the full article from S&P Global Commodity Insights

Access more insights on global trade >

ESG

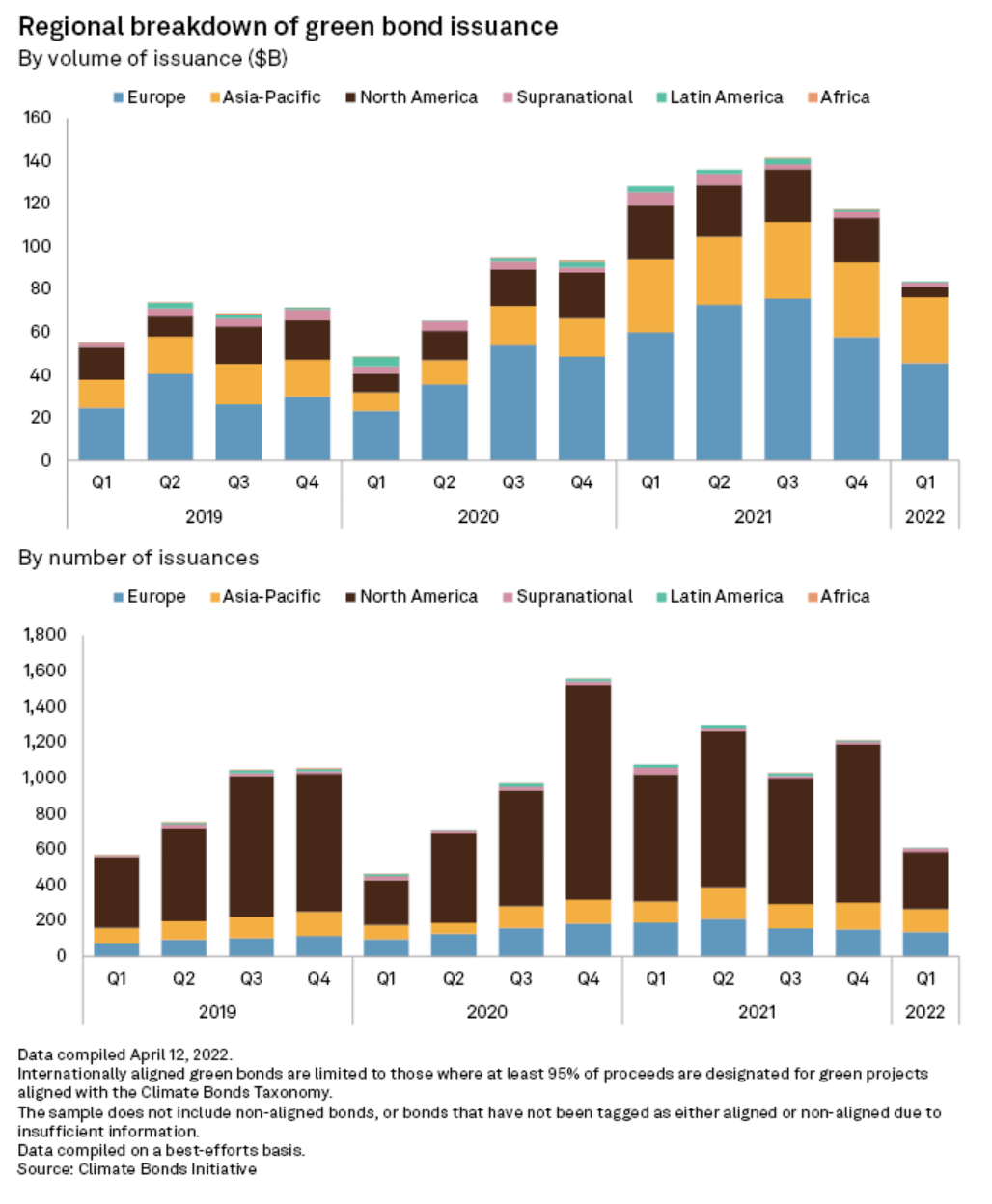

Global Green Bond Issuance Slows Amid Rising Interest Rates, Inflation

The global green bond market faces a lull, as rising interest rates sidelined issuers and investors in the first quarter of 2022. As most central banks hike interest rates to tame inflationary pressures, financing costs for green bond issuers have increased and created uncertainties for investors, analysts said. "The rising-rate environment impairs bond returns and primary issuance, and because the higher credit quality of the green bond market renders it very sensitive to changes in interest rates, the green bond market is down," said Mitch Reznick, head of sustainable fixed income for Federated Hermes, an investment manager.

—Read the full article from S&P Global Market Intelligence

Energy & Commodities

Asia's Oil Demand Revival Bears The Brunt Of China's Endless Lockdowns

Asia's oil demand outlook for 2022 is starting to look dimmer than what it was a couple of months earlier, as China's strict lockdowns aimed at battling the resurgence of the COVID-19 pandemic overshadow positive oil demand signs emerging from the rest of Asia. While most Asian governments are easing restrictions, aiding a sustained recovery in oil demand, China is pursuing a zero-COVID-19 policy that has led to a drop in the appetite for transportation and other fuels in Asia's largest oil consumer.

—Read the full article from S&P Global Commodity Insights

Access more insights on energy and commodities >

Technology & Media

Fuel For Thought — Pace Of Change: Energy And Mobility, Climate, And Innovation

The global energy and mobility industry is at a critical inflection point. Meeting ambitious emissions targets while also delivering energy and mobility for a growing world economy will require new thinking, innovation, and a transformation of a system that supports the $90 trillion world economy. Further complicating this picture are rising geopolitical tensions and nationalism, growing trade friction, supply chain bottlenecks, economic headwinds, and the ongoing pandemic.

—Listen and subscribe to Fuel for Thought, a podcast from S&P Global Mobility