S&P Global — 22 Feb, 2022 — Global

Daily Update: February 22, 2022

By S&P Global

Start every business day with our analyses of the most pressing developments affecting markets today, alongside a curated selection of our latest and most important insights on the global economy.

Emerging market economies are set to experience changing credit circumstances as geopolitical risks flare, inflation increases, interest rates rise, and financing conditions tighten.

During the coronavirus crisis, emerging markets (EMs) have suffered the worst of the pandemic’s health and socioeconomic implications, while developed economies have been able to administer more COVID vaccines and enjoy stronger rebounds. Nonetheless, EMs’ vaccination rates have picked up, mobility and activity have only been somewhat hurt by the spread of the omicron variant, and recoveries are moving forward.

But risks for EMs are rising. Geopolitical tensions are surging. Core inflation is expected to move higher. The U.S. Federal Reserve and other major central banks around the world are preparing to tighten monetary policy. Banks’ liquidity may be reduced and financing conditions could worsen, according to S&P Global Ratings.

“Financing conditions have tightened for EMs, both domestically and externally,” S&P Global Ratings said in its latest macroeconomic report on EMs. “This has been much more pronounced outside of Asia. Inflation has been rising in Eastern Europe and LatAm, prompting significant tightening by central banks and/or markets, driving yields higher. Inflation expectations in advanced economies have also driven markets to reprice dollar-denominated bond yields in most EMs. On top of rising benchmark yields, EM spreads have also been ticking up across the board. Factors contributing to this include geopolitical risk in EM EMEA and growth risks in Asia and LatAm.”

Fifteen banking systems across the largest EMs (Argentina, Brazil, Chile, China, Colombia, India, Indonesia, Malaysia, Mexico, the Philippines, Russia, Saudi Arabia, South Africa, Thailand, and Turkey) face particular risks this year from the volatile geopolitical environment and domestic policy uncertainty, elevated pressure on asset quality from higher interest rates, and some vulnerability to sudden changes in local or external funding sources, according to S&P Global Ratings.

“Inflation, lower and more expensive liquidity, and political and geopolitical risks will dominate the credit story for banks in EMs in 2022,” S&P Global Ratings Senior Director of Financial Services and Global Head of Islamic Finance Mohamed Damak said in a report last week. “The impact on banks could materialize through lower-than-expected business volumes, higher-than-expected deterioration in asset quality, or some deterioration in banks' funding profiles through 2022.”

Of all regions, credit conditions in EMs face the most risk from higher inflation. As uneven recoveries have developed across core emerging markets in the past year, some are stronger than others. Overall, emerging markets, which have seen turbulence during Fed tightening cycles, appear better-positioned to weather changing conditions than they were in previous cycles—despite the reality that tighter external conditions will pressure EM exchange rates and bond yields, according to S&P Global Ratings. But the combination of worsening financing conditions pressuring low rated corporations, restricted market access, and rising debt costs could increase defaults in EMs.

“Our baseline macroeconomic forecasts broadly anticipate orderly adjustments in interest rates across major EMs in response to the upcoming normalization of U.S. monetary policy. Domestic interest rates and exchange rates in EMs have been adjusting to the expected rise in rates over the last year—much of the action may already be behind us. By most metrics, except fiscal and debt dynamics, EMs tend to be equally or better positioned to face the upcoming Fed tightening cycle than in 2015,” S&P Global Ratings Lead Latin America Economist Elijah Oliveros-Rosen and Chief Emerging Markets Economist Satyam Panday said in a recent report. “The overall impact on each country will depend on many factors, including their policy response. Our analysis suggests that external imbalances will be the main channel of transmission of a faster-than-expected Fed tightening cycle for Argentina, Chile, Colombia, and Turkey, while fiscal imbalances will be the main channel for Brazil, India, and South Africa.”

Today is Tuesday, February 22, 2022, and here is today’s essential intelligence.

Written by Molly Mintz.

Economy

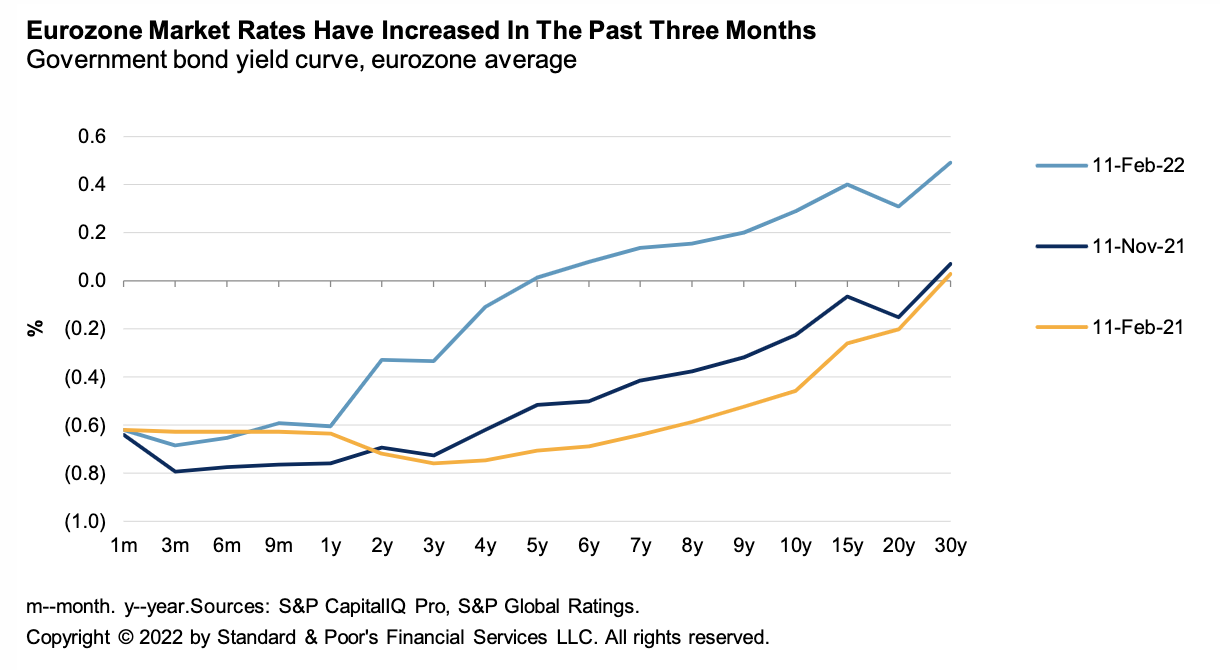

When Rates Rise: Eurozone Bank Earnings Will Too — Especially For Retail

The ECB could start preparing markets for a potential rise in policy rates later this year, which would provide a fillip to profitability for eurozone banks, amid strengthening economic growth and higher inflation. Our sensitivity analysis finds that a rate increase of 100 basis points would boost the sector's annual net interest income 7%-10%. If short-term rates turn positive, then the drag from floored deposits will disappear, most likely benefitting retail banks the most. However, a gradual rate increase would not be a cure-all for profitability, which hinges on banks continuing to transform their businesses and improve efficiency. Higher inflation could also further complicate the control of costs.

—Read the full report from S&P Global Ratings

Access more insights on the global economy >

Capital Markets

Listen: Take Notes: 2022 Latin America Structured Finance Outlook

The S&P Global Ratings Latin American team joins the latest episode of Take Notes to discuss the 2022 outlook for the Latin American Structured Finance market. S&P Global Ratings expects flat issuance relative to last year and stable collateral performance, continuing the trends from 2021. The episode goes into more detail about the major regional markets and asset classes that S&P Global Ratings expects will be most active in the coming year, as well as delving into the major risk factors it identified across the market.

—Listen and subscribe to Take Notes, a podcast from S&P Global Ratings

Access more insights on capital markets >

Global Trade

2022: What Drives The Global Iron Ore Markets?

Join S&P Global Platts as it discusses more about the 2022 driving forces behind the Global Iron Ore Markets during its upcoming webinar. The thought leadership webinar will address any questions about factors influencing demand and price of Iron Ore.

—Register for the webinar from S&P Global Platts

Access more insights on the global trade >

ESG

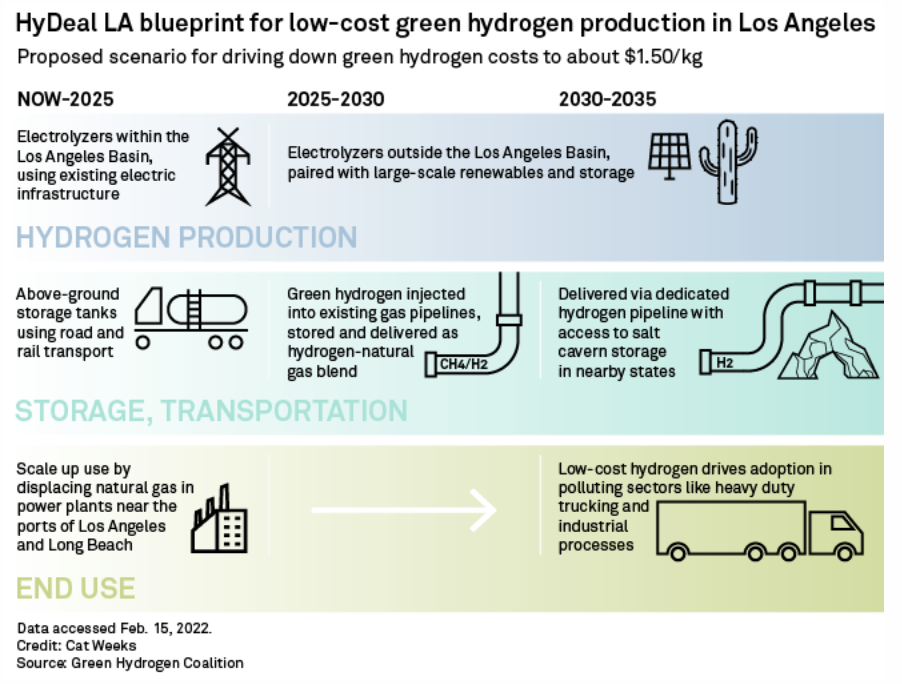

Update: SoCalGas Proposes Nation's Largest Green Hydrogen Infrastructure System

Southern California Gas Co. will seek to develop the nation's largest green hydrogen infrastructure system, a key part of a plan to establish a green hydrogen hub in the Los Angeles area. The proposed Angeles Link would deliver volumes of green hydrogen equal to nearly 25% of the natural gas currently distributed by SoCalGas, the nation's largest gas utility by customer count. The Sempra subsidiary said the project could significantly reduce demand for natural gas, diesel, and other fossil fuels across the Los Angeles Basin.

—Read the full article from S&P Global Market Intelligence

Energy & Commodities

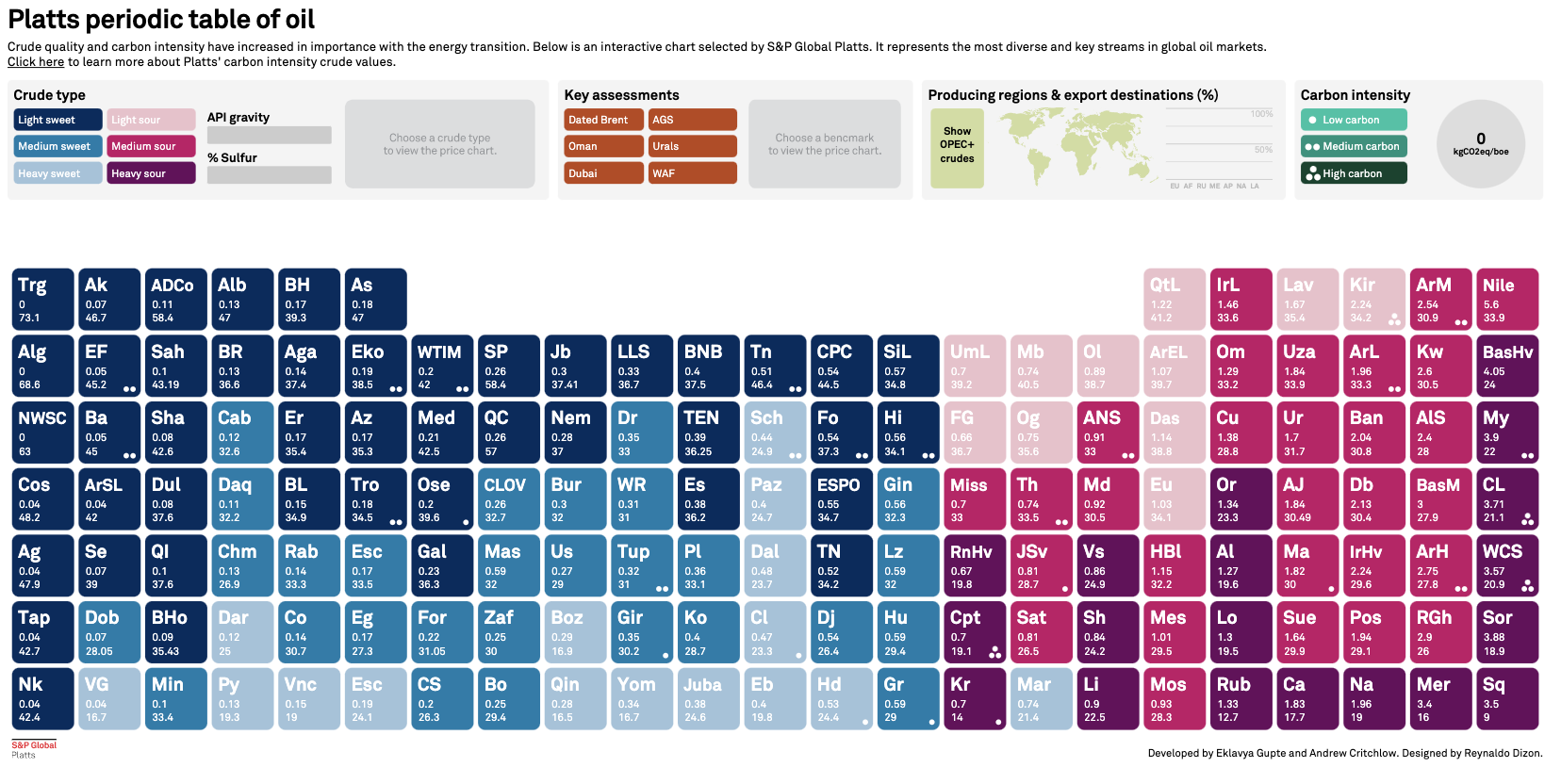

Interactive: Platts Periodic Table Of Oil — 4th Edition Adds Carbon Intensity Data

From the impact of COVID-19 on global demand to the long-term effect of energy transition on petroleum producers and refiners, crude quality has never been more important. Therefore the editorial team at S&P Global Platts has created a fourth edition of the interactive Periodic Table of Oil with new crude grades, carbon intensity values, a significant redesign, and new functionality to help customers plan and make more informed decisions in rapidly changing volatile markets.

—View the interactive from S&P Global Platts

Access more insights on energy and commodities >

Technology & Media

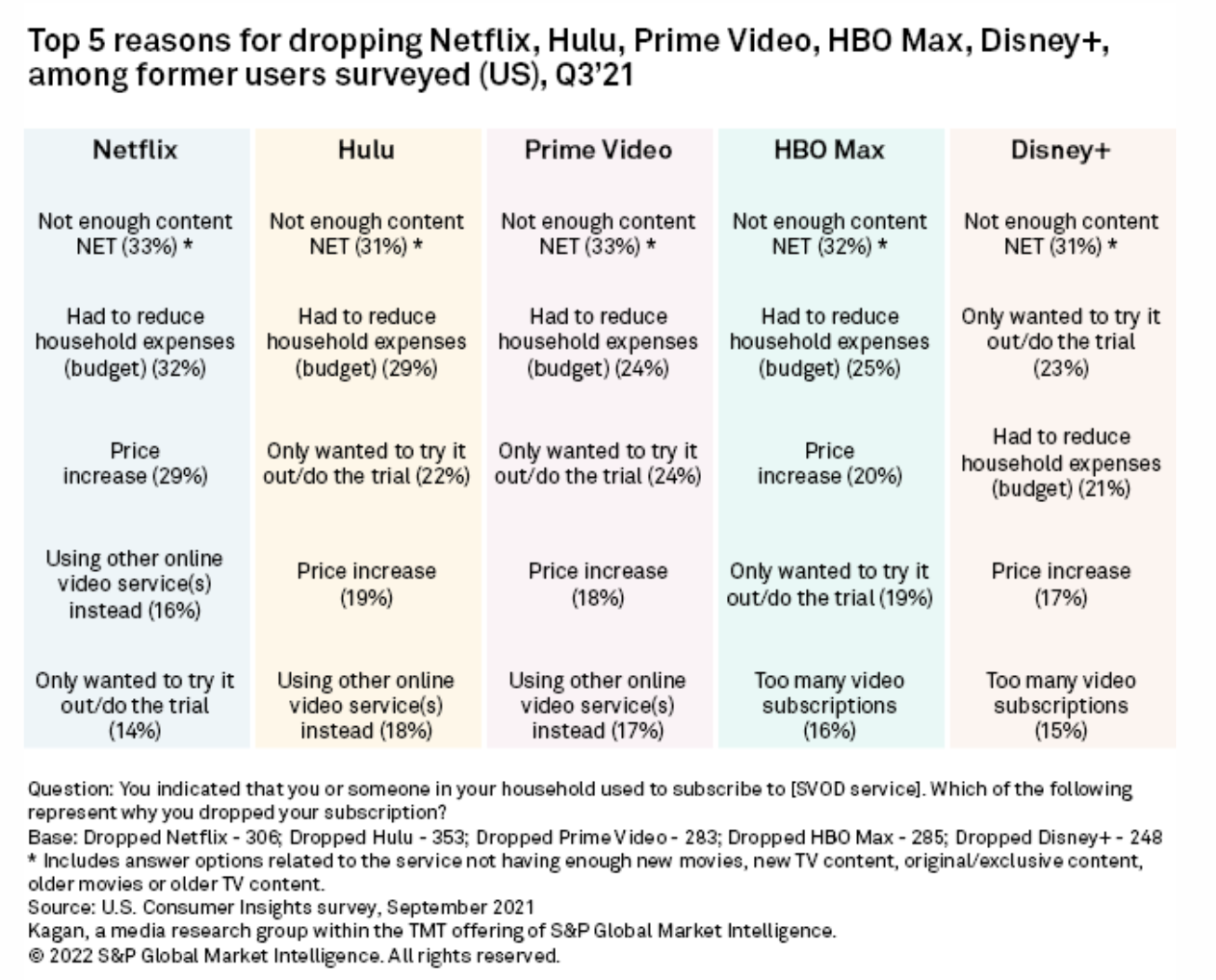

Lack Of Content Outstrips Household Budget In Driving SVOD Churn

Around a third of former subscribers to Netflix Inc., Walt Disney Co.'s Hulu, Amazon.com Inc.'s Prime Video, AT&T Inc.'s HBO Max, and Disney+ indicated that they dropped their subscriptions because of a lack of content. Besides content, according to data from Kagan's U.S. online consumer survey conducted in September, the most selected reason for dropping was reducing household expenses (budget), except among former Disney+ subscribers where that reason came in third. Instead, former Disney+ users were a little more likely to indicate they dropped because they only wanted to try out the service, at 23%, which was also a top reason among former users of Prime Video (24%), Hulu (22%), and HBO Max (19%).

—Read the full article from S&P Global Market Intelligence