Research — Apr. 22, 2026

Rare earth supply chains: Funding, policy and China’s edge

How governments and markets are reshaping rare earth supply

Rare earth elements (REEs) are central to modern manufacturing, clean energy, defense systems and advanced technologies. A series of recent S&P Global Market Intelligence articles examines how governments and markets are responding to risks created by highly concentrated supply chains — particularly China’s dominance across mining, processing and magnet production. Together, the analysis highlights a complex picture: rapid funding and policy support outside China, structural geological constraints, emerging recycling pathways, and the risk that today’s investment surge could lay the groundwork for future oversupply.

Key Takeaways

- Policy intervention is reshaping rare earth markets.

Governments are increasingly intervening through funding, strategic partnerships and industrial policy to reduce reliance on China, with a particular focus on securing magnet-grade rare earth elements critical for clean energy, advanced manufacturing and defense applications. - China’s geological advantage remains decisive.

Many non‑Chinese deposits are harder and more expensive to process, while China’s ionic‑adsorption clay deposits are easier to mine and are enriched in high‑value heavy rare earths, reinforcing its structural cost and processing advantage. - A surge in funding brings both opportunity and risk.

Rapid growth in public and private investment is accelerating rare earth projects outside China, but analysts warn this could create longer‑term oversupply if multiple projects reach production at the same time. - Recycling is growing but constrained.

Rare earth recycling is being promoted as a diversification pathway, yet outside China it remains limited by feedstock availability, logistics and economics, restricting its near‑term impact on supply security. - Diversification will be incremental.

While policy support and capital can speed development, geology, processing complexity and downstream integration continue to limit rapid change, suggesting gradual rather than transformative shifts in global rare earth supply chains.

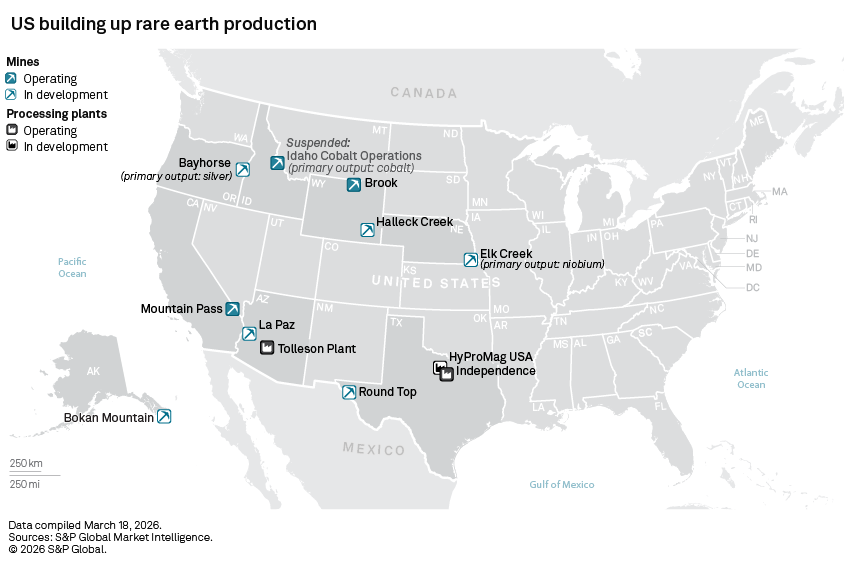

Policy and investment reshape magnet supply strategies

Government intervention has become a defining feature of the rare earth market. Policymakers increasingly view rare earth supply security as a matter of economic resilience and national security, prompting direct involvement through funding, strategic partnerships and industrial policy. Much of this attention is focused on magnet supply chains, as magnetic rare earths are essential for electric vehicles, wind turbines, industrial automation and defense applications. While these elements represent a smaller share of total rare earth volumes, they account for a significant proportion of market value and strategic importance.

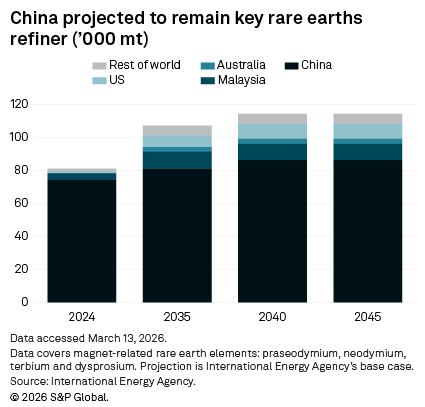

Geology reinforces China’s structural advantage

Despite growing policy support elsewhere, China’s geological endowment continues to underpin its dominance. Many rare earth deposits outside China contain lower‑value elements bound in hard‑rock mineral structures, making extraction and refinement more complex and costly. In contrast, China’s ionic‑adsorption clay deposits are easier to process and are enriched in high‑value heavy rare earths, giving Chinese producers a lasting cost advantage. Analysts note that these geological factors may limit how far subsidies and price incentives alone can rebalance global supply.

State intervention needed to reshape the rare earths market

Market forces alone have failed to diversify rare earth supply chains due to high capital costs, long development timelines and complex processing requirements. Governments are stepping in with industrial policy, funding mechanisms and strategic interventions to support projects that would otherwise struggle to compete with established Chinese producers, framing state action as necessary to reshape the structure of the rare earth market.

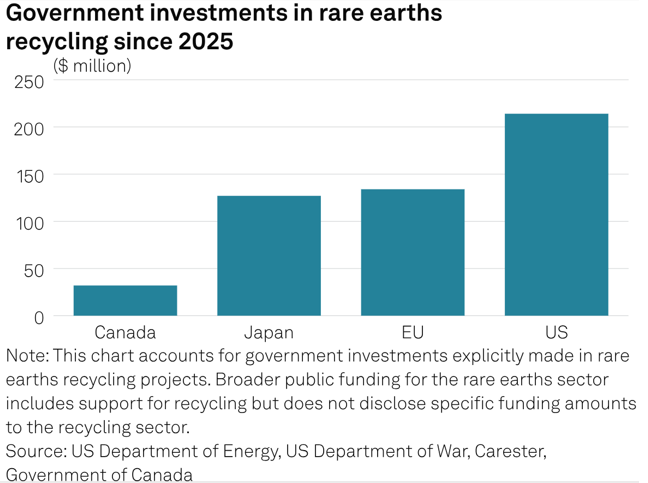

Fledgling rare earths recycling sector offers non‑China supply

Rare earth recycling is increasingly promoted as a pathway to diversify supply outside China. Western countries are investing in recycling infrastructure to recover rare earths from electronic waste and production scrap. However, S&P Global analysis shows that China’s lead in recycling is built on established feedstock networks and integrated processing systems. Outside China, limited access to production scrap, fragmented logistics and higher processing costs continue to constrain scalability, limiting recycling’s near‑term contribution to supply diversification.

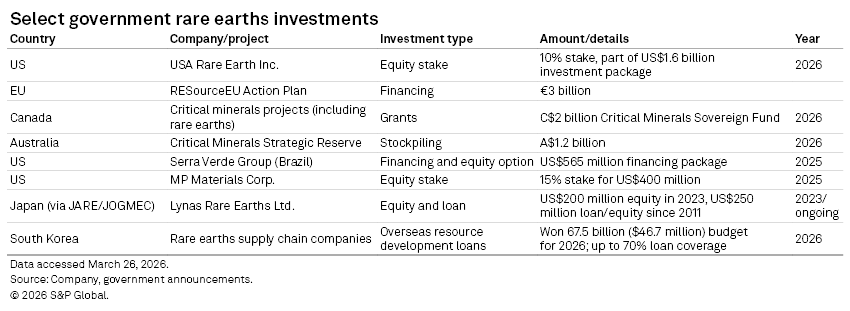

Rare earths funding boom could cause long-term supply glut

Public and private funding for rare earth projects outside China has increased rapidly as governments seek to reduce dependence on Chinese supply. Equity investments, price floors and long‑term offtake agreements are helping to bring new projects forward. While this influx of capital addresses near‑term supply vulnerabilities, analysts warn that it could also create the conditions for overcapacity in the longer term if multiple projects reach production simultaneously. Industry views diverge on whether a future glut will emerge, but the risk highlights the cyclical nature of commodity investment.

What this means for global rare earth supply chains

Taken together, the articles suggest that rare earth supply diversification will be incremental rather than transformative in the short term. Policy support and funding can accelerate projects, but geology, processing complexity and downstream integration remain binding constraints. As governments push for resilience, the balance between security, cost and long‑term market stability will shape how the next phase of rare earth development unfolds.

Why has funding for rare earth projects increased?

Governments and investors are accelerating funding to reduce reliance on China’s dominant rare earth supply chains, using tools such as equity stakes, price floors and long‑term offtake agreements.

Source: Rare earths funding boom

Could today’s funding boom create a rare earth glut?

Analysts warn that heavy investment could lead to longer‑term oversupply if many projects reach production simultaneously, even as shortages persist in the near term.

Source: Rare earths funding boom

Why is state intervention needed in the rare earth market?

Market forces alone have not delivered diversified supply due to high costs, long timelines and complex processing, prompting governments to intervene to reshape production and supply chains.

Source: State intervention needed to reshape rare earths market

Why does China retain a structural advantage in rare earths?

China benefits from ionic‑adsorption clay deposits that are easier to process and richer in high‑value heavy rare earths, while many deposits outside China are more complex and costly to refine.

Source: Rare earth geology tilts global playing field toward China

What makes rare earth magnets strategically important?

Rare earth magnets are essential for electric vehicles, wind turbines, industrial machinery and defense systems, making magnet supply chains a central focus of economic resilience policies.

Source: Policy, economic resilience drives new magnet supply chains

Can recycling provide non‑China rare earth supply?

Recycling offers a potential alternative supply source, but scaling outside China is constrained by limited feedstock, logistics challenges and higher costs.

Source: Fledgling rare earths recycling sector offers non‑China supply

Why is rare earth recycling more advanced in China?

China has established scrap collection networks and integrated processing systems that allow efficient recovery of rare earths from production waste and electronic scrap.

Source: Fledgling rare earths recycling sector offers non‑China supply

Will new magnet supply chains quickly reduce China’s dominance?

Diversification is expected to be gradual, as processing complexity and scale requirements limit how quickly new supply chains can compete with existing Chinese capacity.

Source: Policy, economic resilience drives new magnet supply chains

Where critical minerals intelligence fits

The dynamics explored across these rare earth analyses—from state intervention and geology to recycling constraints and funding‑driven market risk—underscore the need for timely, comparable and forward‑looking intelligence on critical minerals supply chains. Our S&P Capital IQ Pro Metals & Mining service brings together critical minerals data, analysis and research to help stakeholders track policy developments, project pipelines, supply risks and market signals across strategically important minerals, including rare earths. By connecting regulatory shifts, investment trends and structural constraints into a single view, the offering supports more informed decision-making in an increasingly policy-driven and geopolitically sensitive minerals landscape.

Location

Products & Offerings