09 Apr, 2026

RARE EARTHS: Rare earths funding boom could cause longer-term 'glut'

By Kip Keen

| MP Materials' Independence rare earths Source: MP Materials Corp. |

Rare earth elements have come under increasing focus owing to their criticality to defense equipment manufacturing and clean technology. China has monopolized this supply chain for over two decades and has not shied away from using it for geopolitical leverage, forcing others to think of a diversification strategy. This is the last part of a 5-part series in which Platts News explores the strategies under play and the challenges they face. Read parts 1, 2, 3, and 4.

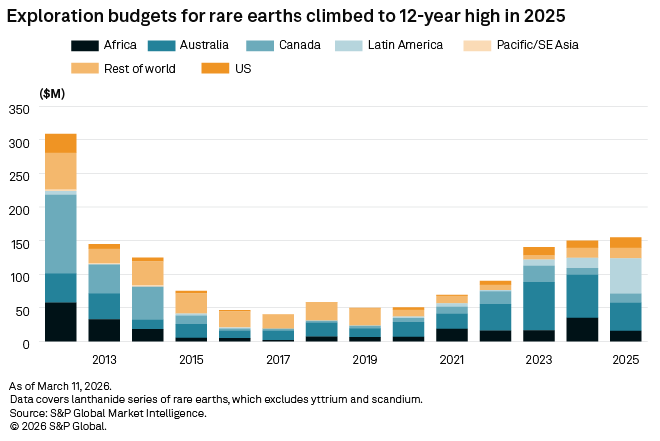

A flood of cash is reshaping rare earths supply chains outside China and seeding the market for possible oversupply years from now, analysts told Platts.

In the short term, growing demand and supply restrictions are set to drive a shortfall, according to experts. But with governments pursuing supply redundancy, and layering price floors and funding onto a niche metals sector, analysts said overcapacity is likely to blossom in the 2030s — though this was a view industry executives contested.

The race to build up production of rare earths materials beyond China comes as countries try to secure materials from domestic sources, or close trade partners, to armor defense sector supply chains, among other policy goals.

"A glut always comes for any commodity market where you're seeing a mass amount of investment like in this space," Jack Baxter, a metals analyst at Bloomberg Intelligence, told Platts, part of S&P Global Energy. "You want to build all the way up to the next marginal source of demand."

Deal mania

The deals have come fast and amounted to billions of dollars pouring into rare earths in just the past year.

Among larger ones, the US Defense Department took a $400 million equity stake in MP Materials in July 2025, promising a $110/kilogram price floor for neodymium-praseodymium (NdPr) and a decade-long magnet offtake commitment. The US Commerce Department followed with a proposed $1.6 billion funding deal for USA Rare Earth Inc. in January, and the company concurrently raised $1.5 billion in private sector financing. And, in February, the US International Development Finance Corporation committed $565 million to Serra Verde Group, a company that produces rare earths in Brazil.

Governments in the US, Canada, Australia and elsewhere are pouring money in rare earth projects and setting pro-rare earths policies to counter China's sway in the market.

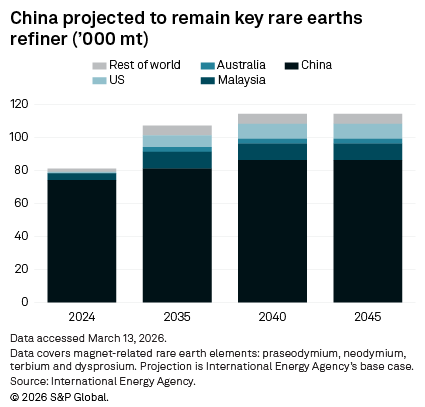

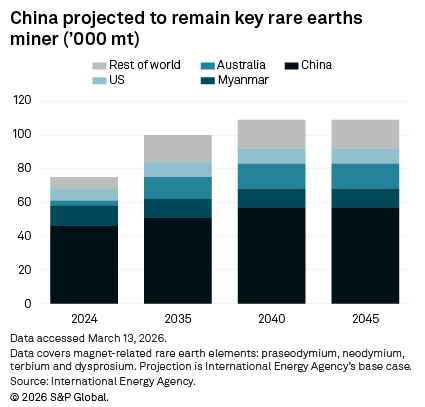

China controlled 91.3% of global processing and 61% of global mining for selected rare earth elements used in magnets in 2024, according to International Energy Agency data. Meanwhile, China has clamped down on rare earth exports, especially for those that could be used for military purposes, exposing a weak spot in global defense supply chains.

Building up rare earths production outside China is the only way to break that reliance, analysts and industry executives said. But oversupply is inevitable once the full weight of government policies and plans are in place across multiple markets, Nick Trickett, an analyst at S&P Global Energy Horizons, told Platts.

"We're headed towards a market where every major economy, alliance bloc and even sub-groups within blocs will want to build redundancy into supply because of geopolitical volatility," Trickett said. "That points to structural oversupply eventually."

Baxter said the most immediate oversupply risk is not in rare earth oxides — precursor materials for more refined rare earths products — but in magnet manufacturing. Announced US capacity of roughly 32,000 metric tons/year in the visible pipeline is approaching the country's estimated annual demand of around 40,000 mt, Baxter said. Meanwhile, those demand expectations were built on electric vehicle adoption forecasts that have since softened.

"The magnet space is one where you could probably see a glut more in the short term," Baxter told Platts.

One market expert expected a US glut to come on weaker than anticipated demand. Jack Lifton, co-chairman of the Critical Minerals Institute, projected US rare earth magnet market demand at between 13,000 and 20,000 mt a year, well below announced production.

"The actual stated demand size or capacity to be developed here of 40,000 [metric] tons a year is about twice as much as we'll ever need," Lifton said. "So a lot of these companies are going to fail."

Oversupply overblown

Still, some industry executives are not convinced emerging supply will overwhelm markets. They cited growing demand, difficulties facing new market entrants, exports, and a sector that has long been starved of cash and needs it now to fulfill policymakers' wishes.

"The capital that is coming in is really just a fraction of what is needed in order to meet the ex-China demand," Tim Johnston, a strategic advisor to REalloys Inc., said. "And so we don't sort of see the government or, to be frank, the private capital in the sector resulting in any sort of oversupply of materials. And in fact, we need more capital to build out more capacity in order to be able to truly build a robust at-scale commercial supply chain for these materials, ex-China, today."

On March 11, REalloys announced the planned construction of what it described as the largest heavy rare earth metallization facility outside China. Heavy rare earths like terbium and dysprosium are key components in high-performance rare earth materials that, notably, are used in the defense sector.

REAlloys' phase one facility, targeting operations in the first half of 2027, is designed to serve the US military's 2027 procurement ban on Chinese-origin materials, with output expected to cover what Johnston described as "a majority portion of the demand requirements for 2027 and 2028."

Forecasts for production of humanoid robots also point to astronomical demand for rare earths — if they materialize.

Mark Chalmers, president and CEO of rare earths and uranium producer Energy Fuels Inc., took a bullish long-term view on demand and doubted oversupply was a threat.

"The day that we're oversupplied is going to be a happy day for everybody," the CEO said.

Chalmers pushed back on demand pessimism, pointing to robotics, drones, the AI-driven data center build-out and the efficiency premium of motors that contain rare-earth magnets as demand drivers that did not exist at scale during the last rare earths boom, which peaked around 2012. The structural difference this time is real, and not all new rare earths companies will succeed, the CEO said.

"There are a lot of people that have big plans, but not necessarily the deposits and the skills to execute those plans," Chalmers said. "I think that those that have good assets, good technical skills and ability to execute will become the winners here, and those that don't — won't."

Energy Fuels is acquiring Australian Strategic Materials Ltd., in a deal expected to close in June. The acquisition will bolt on an operating metals and alloys plant in South Korea and the know-how to replicate it in the US, completing what Chalmers described as a fully integrated chain from mining to alloys. Energy Fuels produces rare earths at its White Mesa mill in the US, where it also has expansion plans.

Booming US capacity could also open up new markets for producers. Industry experts and executives pointed to exports as a possible release valve should the US start producing more rare earths products, such as magnets or alloys, than the domestic market needs.

"It's not like the US fills their demand, and then prices collapse," Bloomberg's Baxter said. "You also broaden the picture out to Europe, where you've seen a lot less investment momentum. There's an exit ramp for that material to be sold off into Europe."

Location

Products & Offerings

Segment