02 Apr, 2026

RARE EARTHS: Rare earth geology tilts global playing field toward China

| Monazite material at the Eneabba project in Western Australia. Source: Iluka Resources Ltd. |

Rare earth elements have come under increasing focus owing to their criticality to defense equipment manufacturing and clean technology. China has monopolized this supply chain for over two decades and has not shied away from using it for geopolitical leverage, forcing others to think of a diversification strategy. This is Part 2 of a 5-part series in which Platts News explores the strategies under play and the challenges they face. Read parts 1, 3, 4, and 5.

Rare earth mining projects outside China face significant economic challenges due to geological differences that make extraction and refining more expensive than Chinese operations, industry experts told Platts, part of S&P Global Energy.

Governments and companies are racing to build new supply chains of critical minerals essential for defense and next-generation manufacturing. Politicians, concerned about China's dominant position in mineral markets and its influence over trade, have turned to industrial policies to support mining projects, including equity stakes, price floors and strategic stockpiling.

However, China's geological advantages with its rare earth mines may outweigh

"The big economic challenge the rest of the world faces is deposit geology," Peter Cook, a geologist and policy analyst at Breakthrough Institute,

Geological advantage

Terbium and dysprosium are heavy rare earth elements used to improve the heat resistance of high-performance neodymium-iron-boron (NdFeB) magnets in electric vehicles and advanced robotics. Although manufacturers use these elements in smaller quantities than light rare earth elements, they are essential to magnets' performance and durability.

China produces most of its heavy rare earths from ionic-adsorption clays, which are mined primarily in southern China, according to the US Geological Survey (USGS). These resources are geologically distinct from the hard-rock REE-bearing deposits found elsewhere, making them easier and cheaper to extract.

"The ionic-adsorption deposits in China are unique in that the REE are weakly bonded to the clays and therefore can be processed quite easily compared to the more traditional deposits where REE are within mineral structures," Tony Mariano, a consulting exploration geologist, told Platts.

Compared to hard-rock rare earth deposits, like bastnäsite or monazite, adsorption clays also have lower concentrations of uranium and thorium — radioactive elements that pose contamination challenges and associated costs in rare earth mining — according to Cook.

China hosts the world's largest rare earth reserves, accounting for 44 million metric tons, or 51.8% of the world's total reserves, according to a USGS report from January. In comparison, the US is estimated to host 1.9 million tons of rare earth reserves.

China also produces light rare earths, such as neodymium and cerium, from two major operations: Bayan Obo and Maoniuping, the first- and third-largest REE-bearing carbonate deposits in the world, according to USGS.

"China simply has the most attractive geology for cheap extraction," Nick Trickett, head of short-term analytics for critical minerals

Closing the supply gap

Many countries outside China host rare earth deposits that mainly contain less valuable elements, such as lanthanum and cerium, which are in abundant supply, according to Cook.

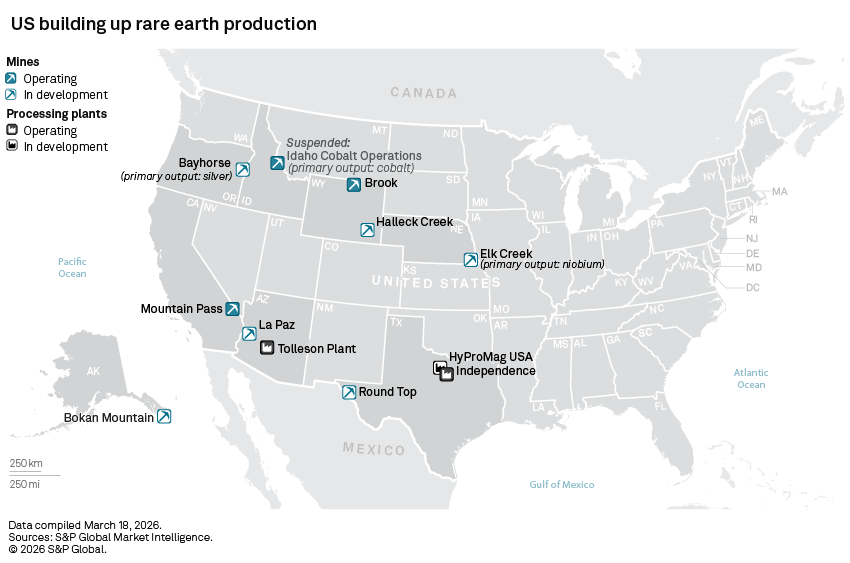

The only active rare earth mine in the US, Mountain Pass in California, hosts light rare earths, and its operator, MP Materials Corp., separates four light rare earths: neodymium, praseodymium, cerium, and lanthanum. Rare Element Resources Ltd.'s Bear Lodge project in Wyoming seeks to produce neodymium, praseodymium, samarium and terbium. The project entered the accelerated US permitting program, called FAST-41, in March.

New heavy rare-earth mines are under development or are soon to come online. Lynas Rare Earths Ltd.'s Mt Weld mine in Australia produces light and heavy rare earths, and the Serra Verde mine in Brazil hopes to ramp up production of heavy rare earth elements by the end of 2027.

MP Materials is pursuing the production of heavy rare earths through a new separation facility which will process the remaining unseparated portion of its ore. The company will begin commissioning the facility in mid-2026.

The geological advantage of Mountain Pass is that its mineral composition is well-understood, and the technology to process its ore has been well established, according to Mariano.

"Mountain Pass is a world-class REE mine, and prior to the China REE dominance, Mountain Pass supplied the world market with REE since the 1950's," Mariano said. The consultant noted that "there are other REE occurrences in the USA that are currently being evaluated for the heavy REE, which occur in minerals that can be economically processed, although not as easily as the ionic-adsorption clays."

A few good mines

In markets where only a handful of mines could shift the balance, government funding and technical support could be a game-changer for projects with the right geology.

"These markets are tiny in physical terms, and given how little capital is needed to make a material impact — opening 2-3 mines for some REEs would be enough to meaningfully shift balances — it's a race to de-risk investment," Trickett said.

Supply of neodymium, praseodymium, terbium and dysprosium will face significant shortages by 2030-35, according to Adamas Intelligence, as demand from EV motors and wind turbines rapidly outpaces production.

The US Defense Department has committed to a 10-year price floor for neodymium-praseodymium products from MP Materials, signaling a willingness to de-risk investment in these small but strategically vital markets. The US also plans to spend $12 billion on a critical minerals stockpile through "Project Vault," announced Feb. 3.

Government intervention is seen as essential, not only through financial guarantees but also via technical support and research partnerships, such as those offered by the Department of Energy and the US Geological Survey.

"Realistically, governments have to intervene and affect price formation through things like price floors because these are tiny physical markets worth very little in dollar terms with enormous leverage for the global economy," Trickett said.

This diversification will likely require continued government intervention and international cooperation to overcome the fundamental geological and economic challenges that have historically favored Chinese production.

"I don't think we will see any other rare earths projects in North America until the 2030s without government support," Chris Berry, founder and president at House Mountain Partners, told Platts.

Location

Products & Offerings

Segment