Research — March 6, 2026

Sandisk to benefit from the AI-driven memory squeeze as prices surge

By Himani Tyagi

A tightening in memory chip supply, driven by accelerating capital expenditure on AI infrastructure, is redistributing earnings across the semiconductor sector, pressuring end-market customers while improving pricing power and margins for memory manufacturers.

For smartphone chipmaker Qualcomm (NASDAQ: QCOM), constrained component availability and shifting capital allocation towards AI servers rather than handsets threaten to make 2026 a challenging year.

For SanDisk (NASDAQ: SNDK), however, the imbalance is proving beneficial.

NAND flash has become a critical enabler of AI workloads, supporting the vast data storage and retrieval demands of large language models and high-performance computing clusters. As hyperscalers accelerate investments in AI capacity, supply of enterprise solid-state drives (SSDs) has tightened, pushing up prices.

Unlike more diversified memory players such as Samsung (KRX: 005930), SK Hynix (KRX: 000660), and Micron (NASDAQ: MU), which are major suppliers of both DRAM and NAND, Sandisk is a pure-play NAND developer and manufacturer.

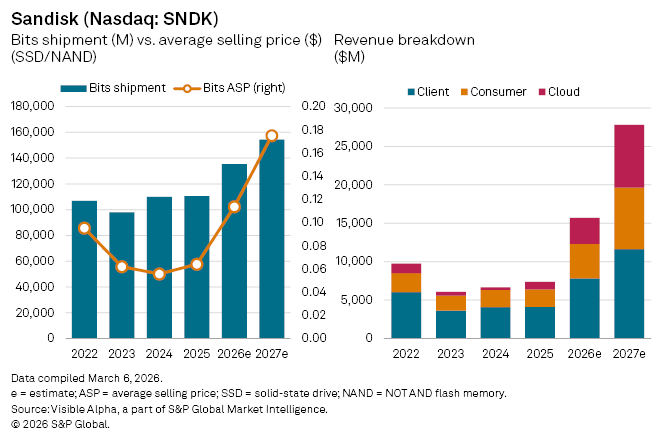

Visible Alpha consensus estimates point to sharp earnings jump for Sandisk driven by these market conditions. Sandisk’s NAND and SSD bit shipments are projected to rise 23% year-on-year to 135,434 million units in 2026, while average selling prices are expected to climb 77% to $0.11 per bit. The combination of volume and pricing power is forecast to drive total revenue up 113% to $15.7 billion.

Profitability is set to swing even more sharply. Net income is projected to reach $6 billion in 2026, compared with a $1.6 billion loss last year. Diluted earnings per share are expected to jump to $37.96 from a negative $11.32, underscoring the operational leverage inherent in memory markets when pricing turns favorable.

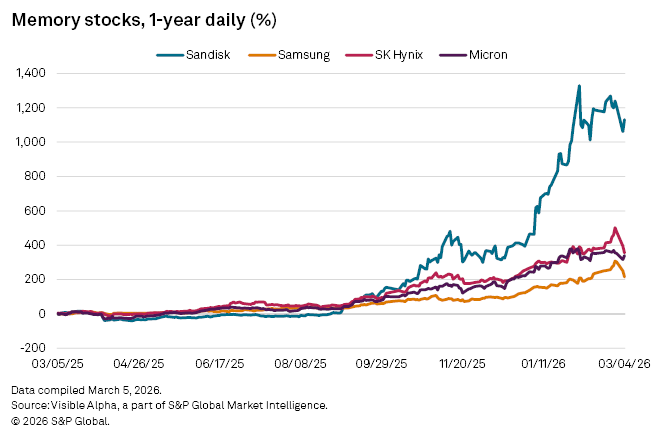

However, the buoyant earnings outlook has done little to shield memory stocks from broader market volatility. US-listed memory stocks have fallen in tandem with their South Korean peers amid concerns that a prolonged conflict involving Iran could drive up global energy prices. Higher LNG costs would directly affect chipmakers in South Korea, one of the world’s largest LNG importers and home to the fabs that produce a significant share of global memory supply, potentially raising operating costs across the industry.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment