Research — February 26, 2026

Qualcomm to see 2026 revenue drop as AI memory boom hits legacy DRAM supply

By Yamini Sharma and Ehteesham Ansari

Smartphone chipmaker QUALCOMM (NASDAQ: QCOM) faces a tougher fiscal 2026, with analysts penciling in declines in both sales and earnings as memory shortages ripple through the handset supply chain.

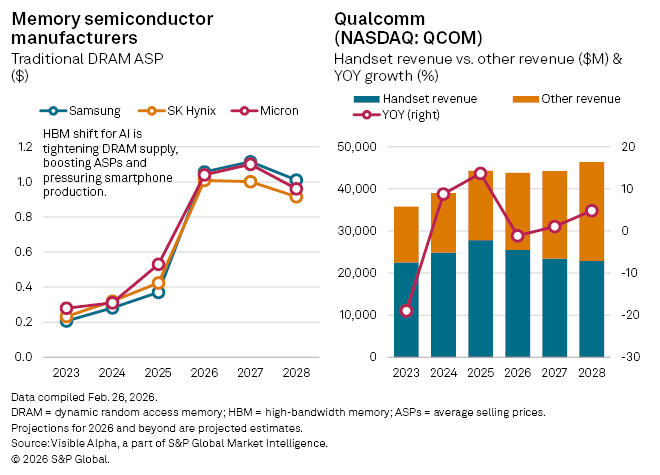

The constraint is an unintended consequence of the AI boom. Surging demand for high-bandwidth memory (HBM), a premium form of DRAM used in AI data centers, has prompted leading memory groups including Samsung (KRX: 005930), SK Hynix (KRX: 000660), and Micron Technology (NASDAQ: MU) to redirect manufacturing capacity away from conventional DRAM used in smartphones. The resulting squeeze in traditional DRAM supply has pushed up prices and constrained handset production volumes.

For Qualcomm, whose Snapdragon processors power a large share of the global Android ecosystem, that dynamic threatens its core franchise. Visible Alpha consensus estimates suggest handset revenues are expected to fall 8.2% year-on-year in fiscal 2026 to $25.5 billion. The segment accounts for roughly 58% of group sales, leaving the company exposed to any prolonged softness in smartphone output.

Overall revenues are forecast to edge down 1.2% to $43.8 billion in 2026, while net income is expected to decline 10% to $12 billion.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment