ECONOMICS COMMENTARY — 08 Jul, 2026

Global employment falls for second month in June amid subdued growth expectations

An increased rate of growth in global output and improved inflows of new business failed to generate a net increase in employment worldwide in June, according to the latest PMI survey data from S&P Global. We learn that high costs have stymied hiring, according to survey respondents, but a more important factor in recent months has been the lack of confidence in the outlook for business growth.

Global employment dips for second month in a row

Worldwide PMI survey data, compiled by S&P Global in association with J.P.Morgan, revealed a further diverging trend in June between rising output and falling employment.

Despite an ongoing expansion of global output in June, as measured across both goods and services, which was sustained by an accelerated rise in new orders worldwide, global employment fell slightly in June for a second successive month. Albeit by a small margin, the global employment trend over the second quarter as a whole has been the weakest since 2020, with an overall small decline recorded by the PMI.

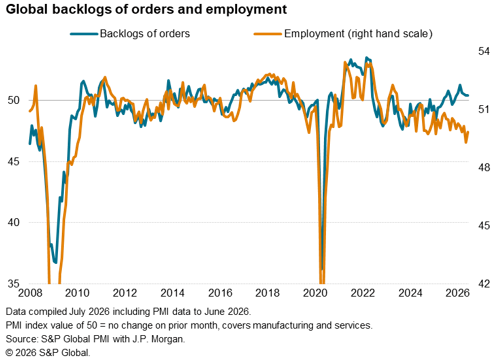

An even wider divergence has opened up in recent months between the global employment trend and backlogs of work. Despite companies reporting higher backlogs of uncompleted orders, which typically stimulates hiring, job losses have accelerated in recent months.

Rising sales fail to stimulate hiring in high-cost environment

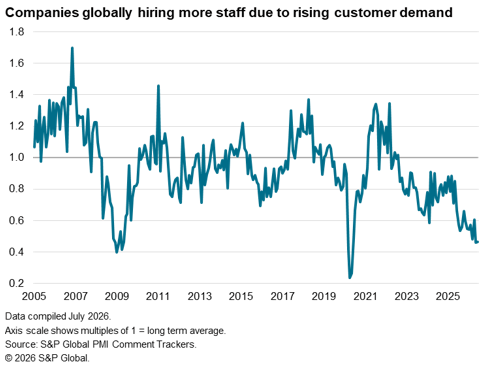

Worryingly, the proportion of companies reporting that rising demand has encouraged them to take on more staff is running at the lowest since the global financial crisis if the pandemic is excluded.

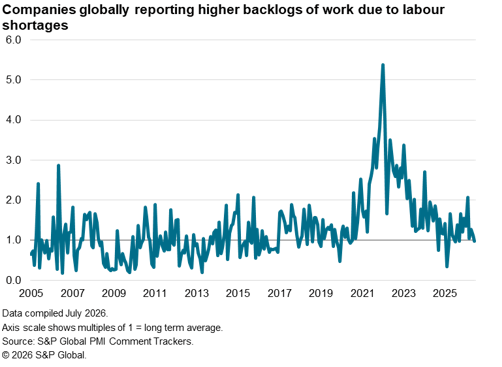

While staff shortages are by no means uncommon in some instances, notably being reported among US survey respondents in recent months, at the global level the number of companies reporting that backlogs of work are rising due to a lack of labour has fallen back to its long-run trend. This indicates that the divergence between strong demand growth and falling employment is not a function of reduced labour supply.

This lack of jobs growth in an environment of rising demand is instead being largely caused by two factors.

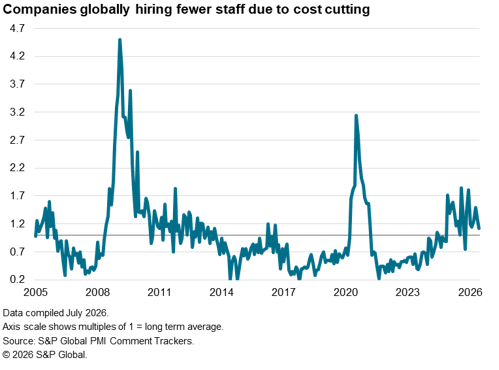

First, companies’ costs have risen sharply since the outbreak of the war in the Middle East, largely driven by higher energy prices, which have added to existing elevated cost burdens in many cases. We can see that the number of companies cutting headcounts in order to cut costs is running above its long-run trend, albeit less so in June than in prior months, suggesting additional factors are at play.

Low confidence

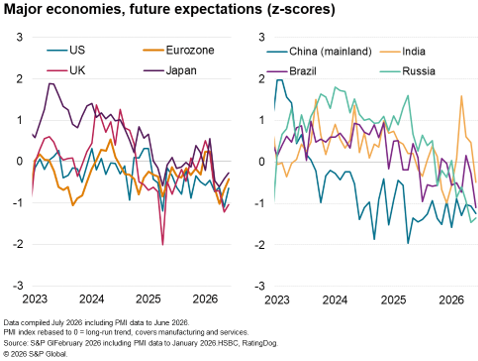

The second factor we can identify is a simple absence of confidence in the business outlook. In spite of June seeing markedly lower oil prices amid an easing of tensions in the Middle East, business output expectations rose only slightly to remain at one of the weakest levels seen in the history of the survey, yet still well off the lows seen during the pandemic. A global PMI Business Output Expectations Index above 60 is broadly needed to encourage hiring, and at 59.2 in June, it’s therefore no surprise to see headcounts being trimmed.

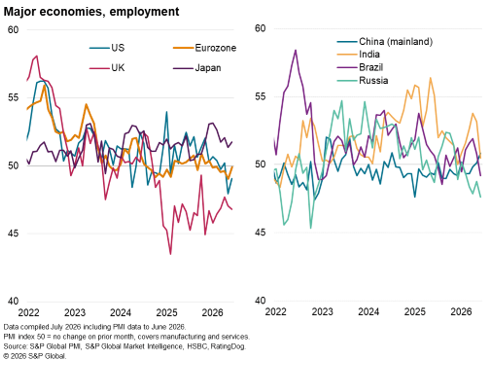

Japan and mainland China lead hiring trends

While growth expectations are below their long-run averages in all major advanced economies, optimism is the least subdued in Japan, which is consequently enjoying the strongest hiring trend. However, confidence in Japan has fallen from recent highs, dampening jobs growth over the second quarter as a whole.

Confidence is meanwhile especially weak in the UK, which is suffering the sharpest loss of jobs, followed by the US, where future growth expectations remain historically subdued despite picking up in June. Eurozone employment meanwhile stabilized as sentiment strengthened for a second successive month.

In the emerging markets, employment fell in Brazil and at an increased rate in Russia due to deepening concerns over the outlook, while India’s job creation trend also weakened thanks to reduced confidence.

Bucking the trend of weaker hiring as a result of poor confidence was mainland China. China’s employment increase was the second-largest for nearly two years, linked to rising backlogs of work.

Our take

The survey data suggest that, despite recent falls in oil prices and better news out of the Middle East, companies are lacking in confidence that the recent upturn in demand will be sustained to warrant additional headcounts. This is particularly evident in the manufacturing sector, where companies recognize that some of the recent upturn in orders reflected precautionary stock building by customers, which will fade in the coming months, and has in fact already showed signs of moderating in June. However, service providers also lack confidence, and companies across all major sectors often cite concerns over geopolitics, national government policy changes, high prices and the accompanying prospect of higher interest rates. A more stable business environment is therefore needed to translate higher output into jobs.

The adoption of AI is a complicating factor, and can be seen among survey contributors as likely causing a net loss of jobs over 2026, though the net impact is indicated to be only minor. See “The AI and labor landscape 2026: Increased investment, persistent productivity gains and a recalibrated employment outlook | S&P Global”.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings