ECONOMICS COMMENTARY — 01 Jul, 2026

Global PMI shows sustained manufacturing growth surge, but future optimism fades

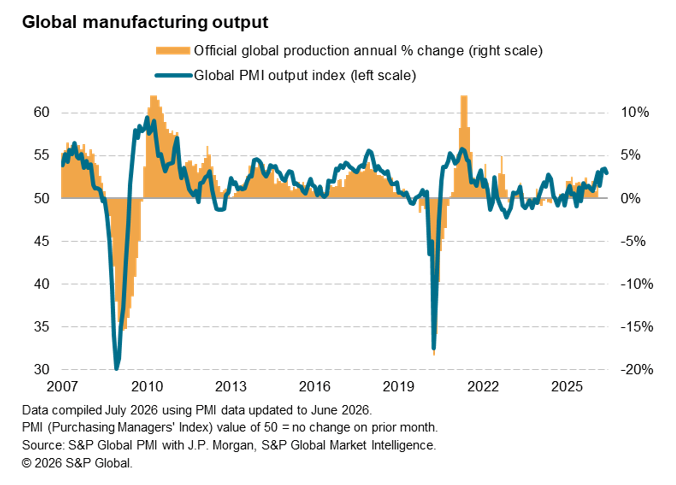

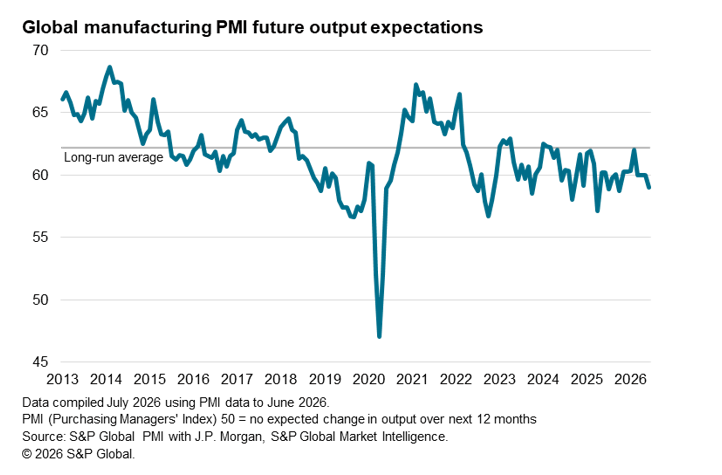

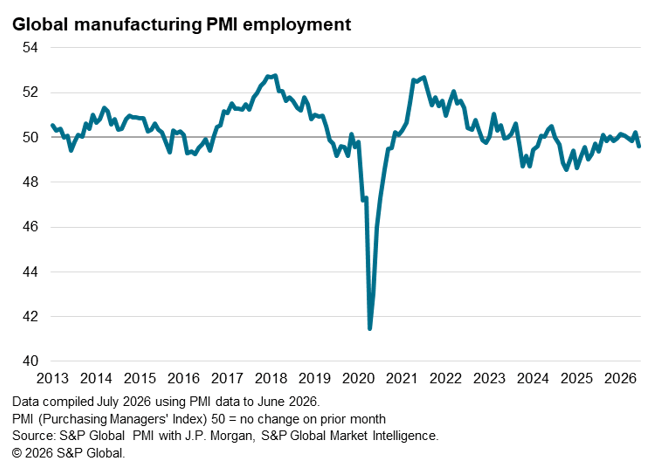

PMI® survey data indicated a further robust rise in worldwide factory output in June, rounding off the strongest quarter for global manufacturing since 2021. However, the outlook for the rest of the year has darkened. Despite June seeing an easing of tensions surrounding the Middle East, with oil prices falling sharply to help allay concerns over recession among survey participants, business optimism has fallen and factories reported lower employment.

Here we analyse anecdotal evidence provided by surveyed companies to assess the causes of weakened growth expectations.

June factory production gain rounds off best quarter since Q2 2021

The Global Manufacturing Purchasing Managers’ Index™ (PMI) survey, sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, recorded a further solid rise in worldwide factory production, sustaining the recent growth spurt which has seen output expand over the second quarter at a rate not seen for five years, though with a little loss of momentum evident in June.

Optimism fades despite reduced recession worries

Worryingly, despite the June data collection period spanning a period in which oil prices fell broadly back to pre-war levels as the news flow out of the Middle East improved, business expectations about future output deteriorated in June, slipping to its lowest since October of last year and descending further below its long-run average.

Factory employment also fell worldwide in June. Although only slight, the decline was the steepest for 11 months to add a further contrast to the upbeat picture signalled by the expansion of production during the month.

The worsening trends in business expectations and employment occurred despite reports of “recession” worries among survey contributors cooling to their lowest since January. Reports of business “uncertainty” similarly fell sharply, down to their lowest since just prior to the outbreak of the war in February.

We can, however, identify three other principal factors that have curbed business growth expectations.

Shifting inventory cycle

First, June brought signs of the inventory cycle starting to act as a drag on growth. Analysis of comments provided by surveyed companies explaining changes in order books and purchasing behaviour reveal that precautionary stock building has become widely reported since the outbreak of war. However, the incidence of order books being buoyed by customers building inventory has now fallen to its lowest since January. The number of manufacturers building safety stocks has meanwhile fallen to its lowest since February.

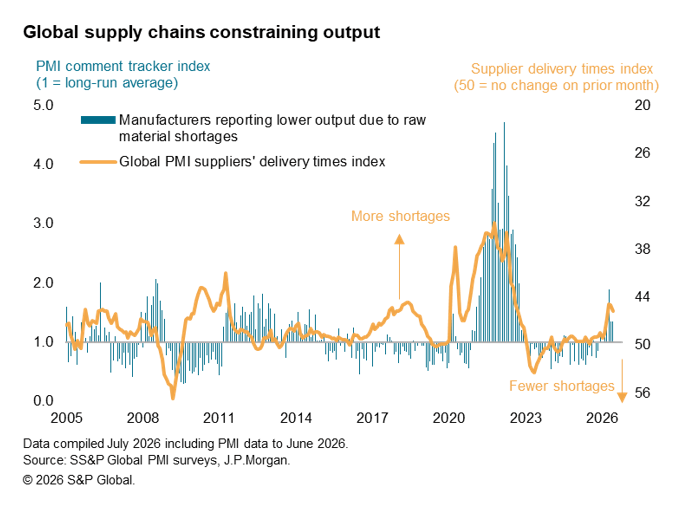

Supply constraints

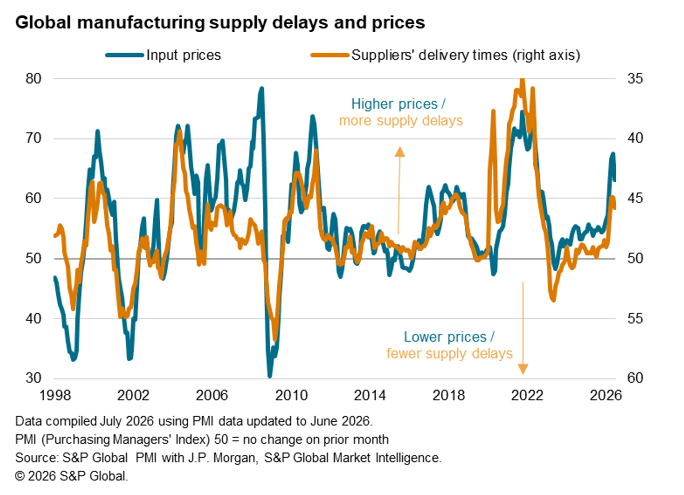

Second, although input cost inflation eased in June alongside a concomitant reduction in the reporting of supply chain delays, both producer price inflation and the overall incidence of supply delays nevertheless remained the third-highest since 2022.

Supply scarcities consequently continued to inhibit production in some cases, with the incidence of supply-constrained output running at the highest for over four years in recent months and into June.

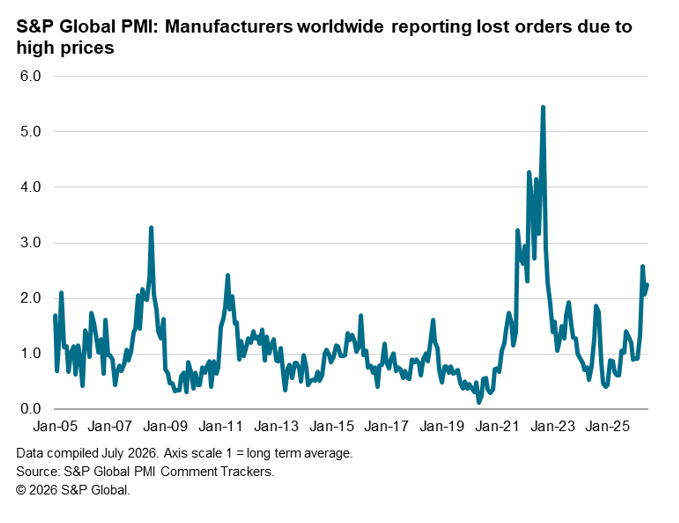

Push-back on higher prices

However, a third and bigger issue in terms of limiting sales and production growth was high prices. The pass-through of higher costs on to customers led to a further marked increase in factory selling prices in June, but the number of companies reporting that sales have been lost due to customer resistance to these higher prices continued to run at its highest since late-2022.

Outlook

Companies are therefore concerned that a surge in precautionary stock building, which helped boost demand in the second quarter, is starting to fade and will continue to do so in the coming months, while existing supply shortages will limit production in some instances. High prices are meanwhile a further major perceived drag on demand.

While the impact of the shifting inventory cycle will likely persist and potentially intensify as a drag on the sector in the third quarter, both the supply constraint and price factors could alleviate further in the coming months if the situation in the Middle East continues to improve.

Access the latest global PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings