ECONOMICS COMMENTARY — 29 May, 2026

Week Ahead Economic Preview: Week of 1 June 2026

The following is an extract from S&P Global Market Intelligence's latest Week Ahead Economic Preview. For the full report, please click on the 'Download Full Report' link.

Payrolls and PMI surveys

Central bank watchers will be eagerly awaiting US non-farm payroll data as well as flash eurozone inflation numbers for May. A broader picture of how the global economy has fared as the war in the Middle East rolls into its fourth month will be provided by the PMI surveys.

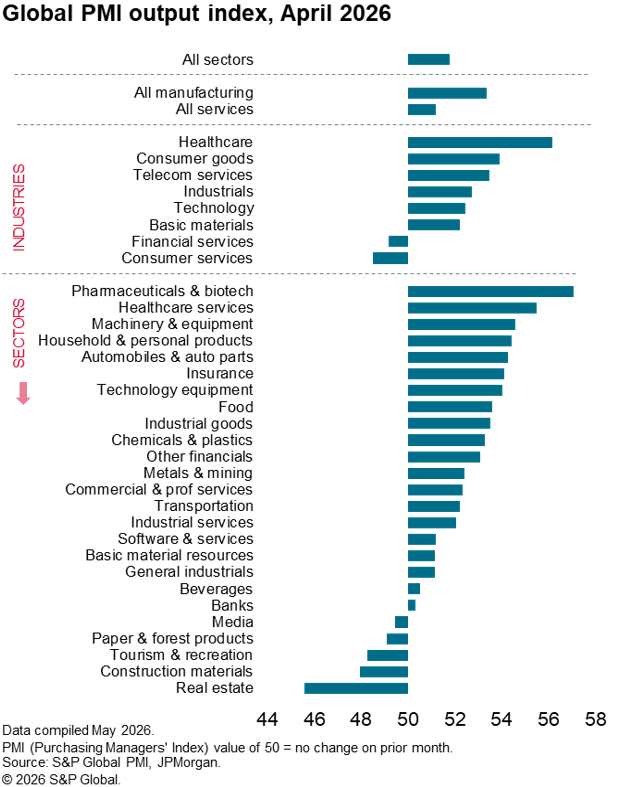

Worldwide PMI data for both manufacturing and services are updated for May in the coming week to reveal the impact of high energy prices and squeezed supply chains from the ongoing conflict in the Middle East. April’s data showed global economic growth having shifted down a gear since the onset of the war, albeit supported by stock building as companies grew increasingly concerned over rising prices and supply chain delays; the latter at their worst since 2022. Of particular concern was a slowdown in services activity in many of the world’s major economies, reflecting squeezed consumer spending power from rising energy prices, as well as disrupted tourism and travel (see chart).

Following the PMIs, Friday will reveal more clues as to what the US Federal Reserve might do next with interest rates via the monthly jobs report. While we are seeing clear signs of a near-term uplift in inflation from the impact of the war, higher interest rates would only likely be seen as appropriate if the rise in inflation looked stubborn, and if the Fed’s second mandate of maximum employment was not being compromised by the conflict.

Hence any ‘second round’ inflation effects via wage growth will be scrutinised, as will the non-farm payroll numbers. Although payrolls beat expectations in April, posting a 115,000 rise, and the unemployment rate was reassuringly low at 4.3%, both the participation rates and employment rates hit their lowest for over four years. Moreover, flash PMI data showed US jobs growth cooling in May as companies responded to rising costs and weakening demand, notably in the services economy. Earnings growth has meanwhile been relatively modest at 3.6%, albeit on the rise.

With the ECB meanwhile widely seen as poised to hike interest rates in June to combat war-related price pressures, the flash CPI inflation reading for May will come under scrutiny, especially in relation to core prices. This follows flash PMI data showing a strengthening of inflationary pressures in May.

Chart of the week: PMIs have signaled slower global growth since the outbreak of war, led by slumping demand for consumer services

S&P Global updates its detailed sector PMI numbers in the coming week, alongside the national survey results. Prior data showed consumer services activity having been hit especially hard by the war in the Middle East, but with real estate activity and construction suppliers also seeing especially sharp downturns.

Read more about recent worldwide PMI trends here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings