ECONOMICS COMMENTARY — 06 May, 2026

Global PMI rises in April as war-related supply and price worries boost manufacturing

April’s PMI surveys produced by S&P Global indicated an upturn in the rate of worldwide economic growth after the pace had slumped in March following the outbreak of war in the Middle East. However, the expansion remained one of the weakest seen over the past year amid a combination of supply chain delays, rising prices and a lack of business confidence stemming from a near-record level of uncertainty.

Global PMI rises in April

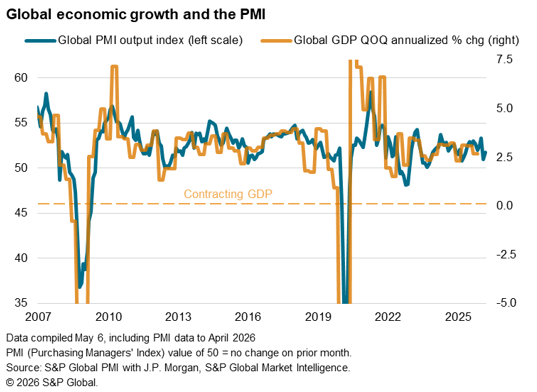

Survey data indicate that the war in the Middle East continued to dampen economic growth in April, albeit with the rate of growth lifting higher from March’s recent low. The J.P.Morgan Global Composite PMI Output Index rose from 51.0 in March to 51.8 in April. The upturn signals an acceleration of economic growth after March had seen the sharpest fall in the PMI since 2008, barring only the pandemic.

Despite the rise, the rate of growth remained the second-weakest seen over the past ten months, indicating that the economic expansion has moved down a gear since the US-Israeli attacks on Iran at the end of February.

The PMI readings are broadly indicative of global GDP growth running at an annualized rate of 2.0-2.5% over the past two months, down from around 3% at the start of the year.

Services hit hardest by war, but factories benefit from stockpiling

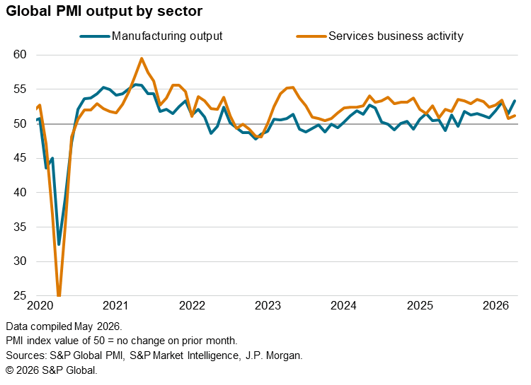

Key to the sluggish global expansion was the service sector, where growth edged up only slightly on that seen in March to remain the second-weakest seen over the past year – and one of the weakest seen for the past four years amid near-stalled inflows of new work.

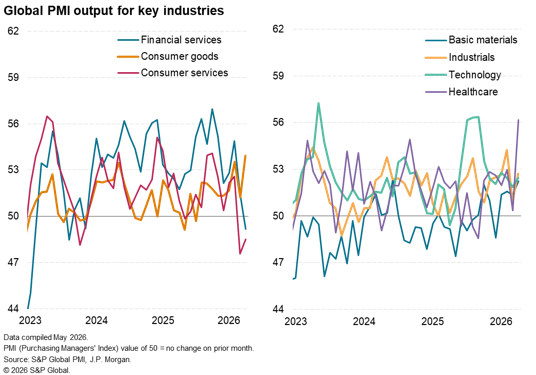

Strong healthcare growth was countered by a further contraction of consumer services activity amid ongoing travel disruptions and reduced demand for activities in areas such as tourism & recreation, often linked to high prices and uncertainty emanating from the war. Financial services activity likewise contracted, dropping for the first time since November 2023.

In contrast, manufacturing output growth accelerated globally to the fastest since July 2021, led by consumer goods producers, rebounding sharply from the war-related slowdown seen in March.

Stockbuilding

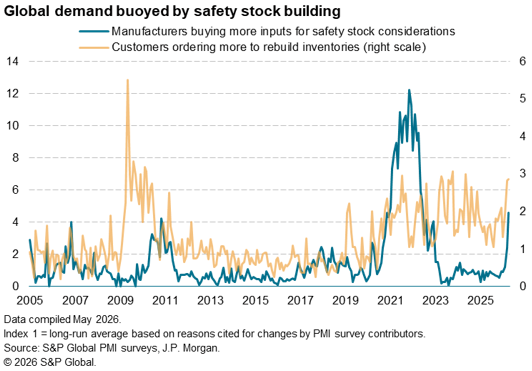

However, the performance of the manufacturing sector was buoyed by precautionary stockpiling as producers and their customers worried about supply availability and future price hikes, effectively providing a temporary front-loading of business activity and sales which will lead to slower growth later in the year.

The proportion of manufacturers worldwide reporting higher input buying due to the need to build safety stocks has risen to its highest since June 2022, and a level unprecedented outside of the pandemic.

The number of customers ordering more from factories and citing the need to build inventories has meanwhile risen to one of its highest levels seen over the past 15 years.

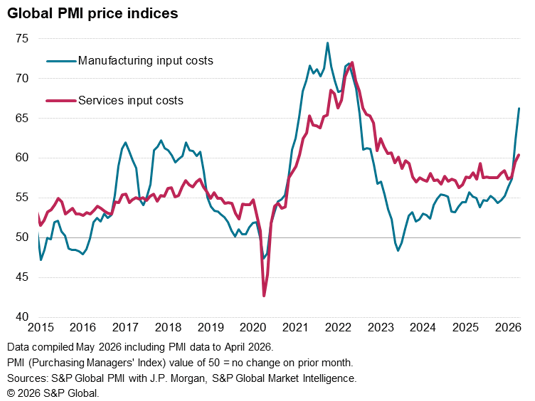

Price and supply woes

Supply fears reflected a lengthening of supplier delivery times in April to the greatest extent seen since August 2022, during the pandemic.

Combined with the impact of higher energy and shipping prices, the additional pricing power accorded to suppliers via the imbalance of supply and demand led to the sharpest spike in manufacturing input costs since June 2022. The rate of inflation accelerated sharply for a third successive month (since the outbreak of the war in the Middle East at the end of February, the PMI’s Input Prices Index has risen to its greatest extent since the start of 2010).

However, service sector input cost inflation also accelerated, largely linked to higher energy prices, to now sit at a three-year high.

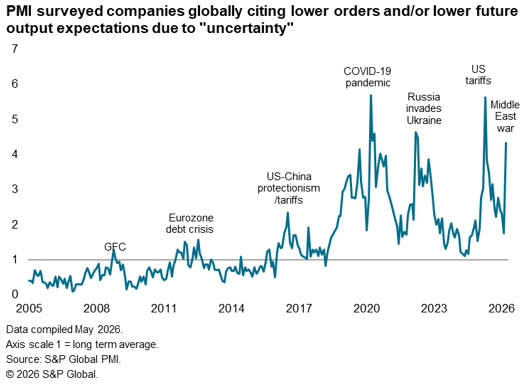

Business uncertainty spikes higher

Having fallen in March to their lowest since October 2022, output expectations for the year ahead were unchanged in April, holding steady in both manufacturing and services. However, with the exception of last year’s tariff announcements by the US, business optimism has not been lower than recorded over the past two months since the early months of the pandemic.

Key to the lack of optimism is uncertainty regarding the economic outlook, hinging on the war and its impact on supply chains, prices, affordability and caution with regard to spending.

Reports of ‘uncertainty’ having adversely affected business order books and growth expectations for the year ahead spiked higher still in April, rising in manufacturing to the highest seen over more than two decades of comparable survey history and at one of the highest levels recorded among service providers.

Access the full press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings