ECONOMICS COMMENTARY — 05 May, 2026

Global PMI shows prices rising sharply amid worsening supply chain delays

Supply chain disruptions look set to drive inflation higher around the world, according to PMI survey data, as a direct result of the war in the Middle East.

Supply chain delays are exerting additional upward pressure on prices as supply exceeds demand for many goods, exacerbating the impact of higher energy and shipping costs due to the war.

A surge in purchasing as companies build safety stocks is meanwhile boosting global production, but will inevitably fade in the months ahead. Whether price pressures likewise fade remains more uncertain.

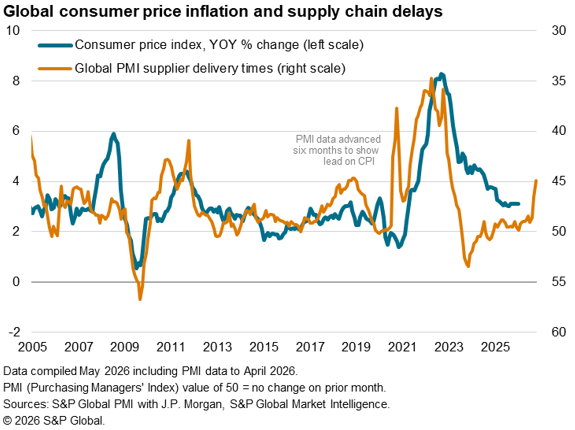

Supply chain delays add to energy and shipping cost pressures

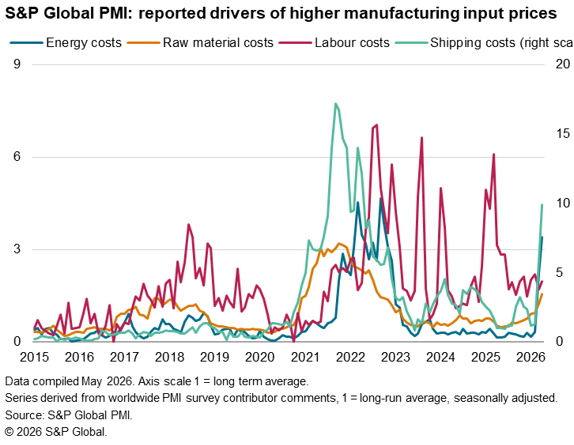

The Global Manufacturing Purchasing Managers’ Index (PMI) survey, sponsored by J.P. Morgan and compiled by S&P Global Market Intelligence, recorded the sharpest spike in producer input costs since June 2022 during April, the rate of inflation accelerating sharply for a third successive month.

Since the outbreak of the war in the Middle East at the end of February, the PMI’s Input Prices Index has risen to its greatest extent since the start of 2010.

Much of the acceleration of inflation has reflected higher energy prices resulting from the war. According to analysis of survey contributor commentary, energy costs exerted their strongest upward pressure on firms’ costs since October 2022.

Higher shipping costs, due largely to the closure of the Strait of Hormuz, have also put upward pressure on prices for a wide variety of goods and inputs used by factories around the world to a degree not seen for four years.

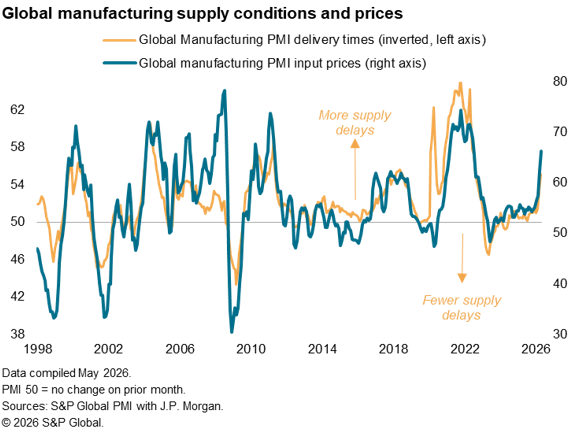

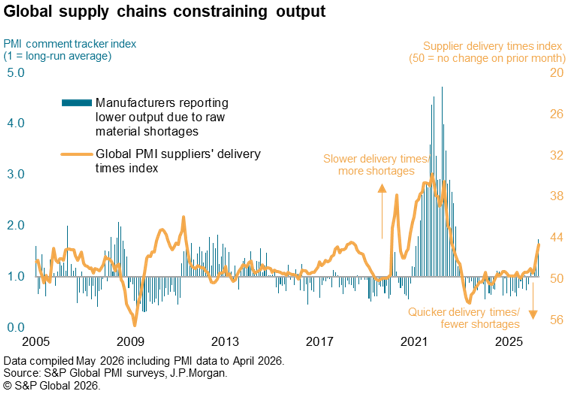

However, an additional impact from the war is evident through a growing number of supply chain delays. The PMI’s Supplier Delivery Times Index, which measures the time taken for suppliers to deliver inputs to factories, signalled the greatest lengthening of lead-times since August 2022 in April.

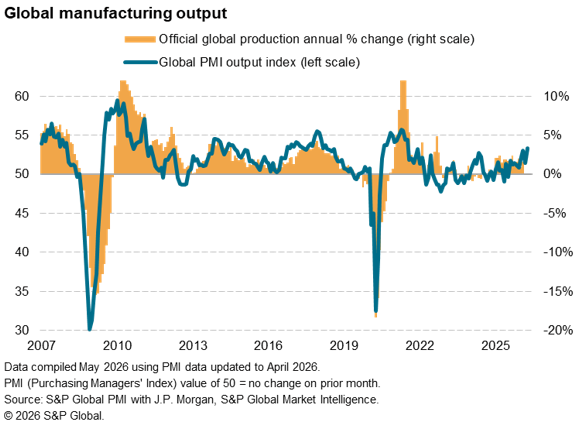

Factory output growth highest for nearly five years

A more encouraging signal from the April survey was an acceleration of manufacturing output growth globally to the fastest since July 2021. The PMI’s output index is broadly indicative of worldwide manufacturing production expanding at a 3.5% annual rate.

However, this upturn in production looks unsustainable, as it was in part a reflecting of widespread stock building as manufacturers and their customers grew increasingly worried about rising prices and supply scarcities during April.

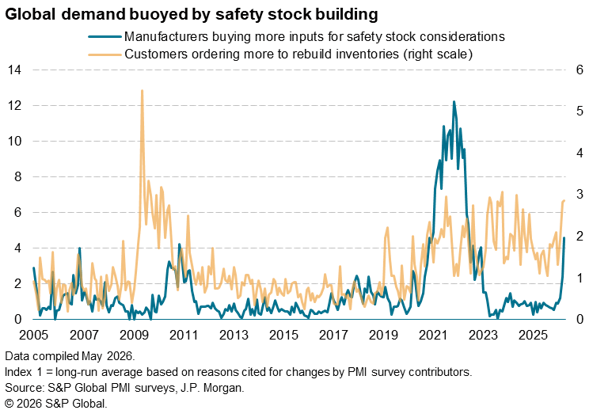

Stock building

The proportion of manufacturers worldwide reporting higher input buying due to the need to build safety stocks has risen to its highest since June 2022, and a level unprecedented outside of the pandemic. The number of customers ordering more from factories and citing the need to build safety stocks has meanwhile risen to one of its highest levels seen over the past 15 years.

The concern is that this stock building is providing only a temporary boost to manufacturing output, while simultaneously putting upward pressure on prices. The payback after this stock build in terms of lower output looks inevitable later this year, especially if output becomes more constrained by supply chain disruptions. Note that the PMI contributors already report that supply shortages are constraining output to a degree not seen since October 2022.

However, whether we see a commensurate drop in prices as the stock build fades remains more uncertain, and will depend on the duration of the conflict and its associated energy and supply chain disruptions. Importantly, with a lengthening of supply chains generally taking around six months to feed through to higher consumer prices inflation (see first chart), we can already expect a marked upturn in household inflation rates in the months ahead.

Access the latest global PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings