ECONOMICS COMMENTARY — 21 May, 2026

Flash US PMI signals subdued growth and job cuts in May amid price surge

The damaging economic impact from the war in the Middle East is becoming increasingly evident, according to the latest ‘flash’ PMI survey from S&P Global. May data recorded only modest growth of US business activity as demand was again squeezed by a further spike in prices while jobs were cut as firms worried over rising costs and the economic outlook.

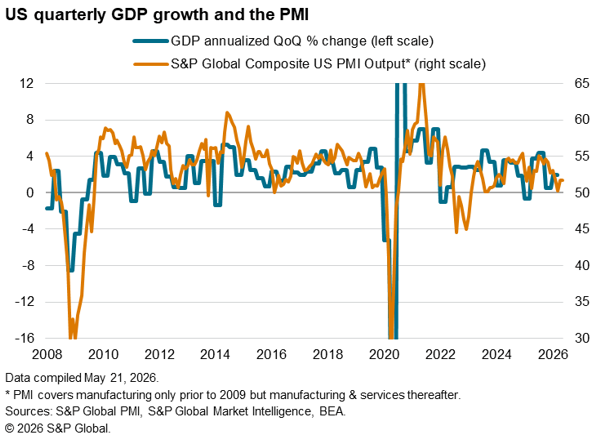

Coming on the heels of a subdued April reading, the May PMI indicates that the economy will struggle to manage annualized GDP growth of much more than 1% in the second quarter. However, sub-indices from the survey, analyzing inventories and order books suggest that even this subdued pace of growth may not last for long, setting the scene for potential mixed views among policymakers on the correct course for monetary policy.

Output growth has stepped down a gear

Business activity continued to grow in May but at a reduced rate compared to that seen earlier in the year. The headline ‘flash’ S&P Global US PMI Composite Output Index, covering both manufacturing and services, held steady at 51.7 in May. Growth over the past three months since the outbreak of war in the Middle East has been the weakest seen since the start of 2024.

Comparisons with official GDP data indicate that the recent readings of the PMI are broadly consistent with the economy growing at a mere 1%-1.2% annualized rate so far in the second quarter, representing a marked contrast to the robust growth signaled at the turn of the year.

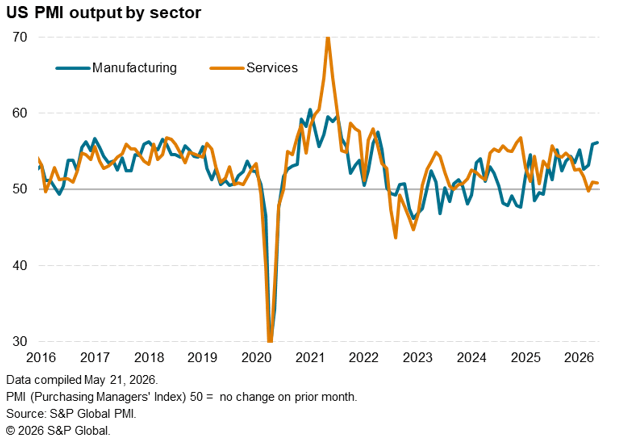

Sector divergences widen

Divergences persisted in terms of the impact of the war by sector. Services growth remained especially sluggish, on course for its weakest calendar quarter since late-2023 as new business inflows rose only modestly, albeit improving on the slight decline seen in April. Service providers reported demand to have often been subdued by rising prices and uncertainty, notably among consumer-facing businesses and for exports. Services exports fell at the sharpest rate for six years.

Manufacturing output meanwhile rose at the fastest rate for just over four years, with the rate of growth accelerating from the already-robust pace seen in April. However, an accompanying marked influx of new orders for goods in part again reflected precautionary stock building. Order book growth in manufacturing was notably purely domestically driven, with goods exports falling again in May.

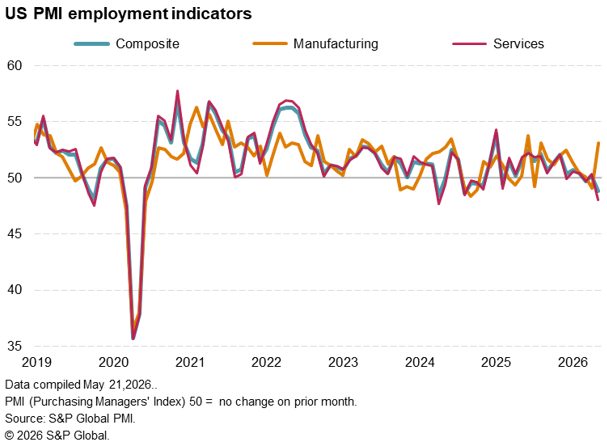

Job losses mount

Sector divergences were also evident in terms of the labor market. Measured overall, employment fell for the second time in the past three months in May. The rate of job losses hit the highest since August 2024 due to growing concerns over rising costs and deteriorating demand conditions.

However, whereas service sector jobs were culled at the second-fastest pace seen since the early months of the pandemic in 2020 (with only April 2024 having seen steeper job losses), manufacturing payrolls showed the largest rise for 11 months as factories raised headcounts to meet the recent upturn in orders.

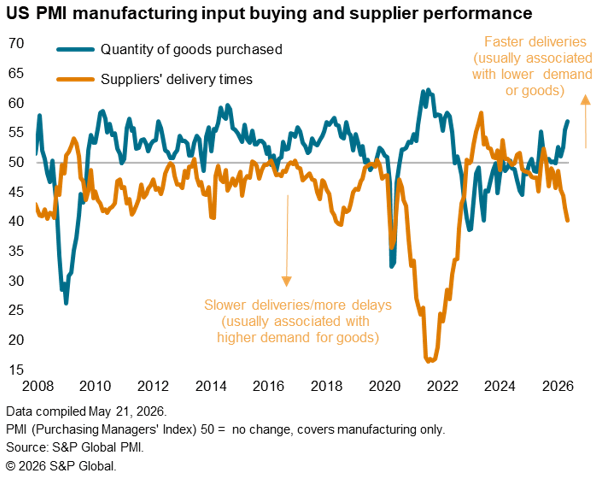

Supply chain delays

War-related issues meanwhile led to a further deterioration of supply chains. Factories reported the greatest lengthening of supplier delivery times since August 2022. Lead-times have now lengthened continually over the past nine months, with factories reporting that war-related shipping disruptions and stock piling have exacerbated existing tariff-related supply constraints.

The further stock piling trend was reflected in the amount of inputs bought by factories rising in May at its steepest rate since April 2022, driving inventories sharply higher. However, by its nature this stock build will not last forever, posing downside risks to output in the coming months once warehouses fill.

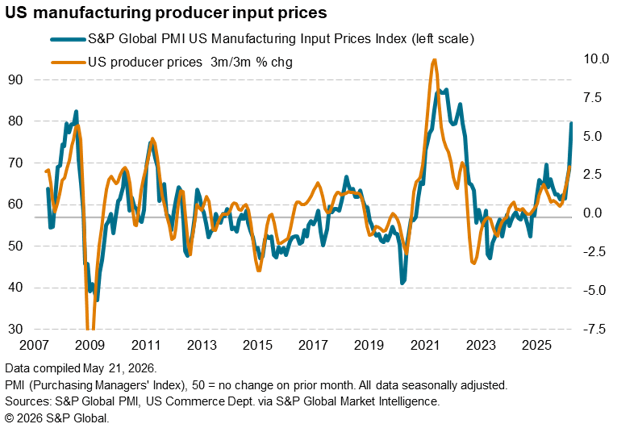

Price surge intensifies

Demand also looks set to cool further in response to rising prices. Firms’ costs have jumped higher at a pace not seen since the energy price shock of 2022 and are being passed on to customers in the form of sharply higher selling prices.

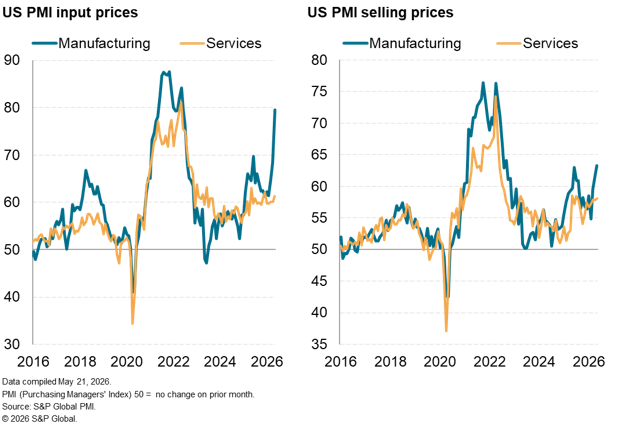

Input price inflation surged higher at a pace not seen since November 2022, in part due to supply constraints but also driven higher by increased energy prices. Manufacturing input costs registered the largest monthly increase since June 2022.

While the rise in services costs was more muted by comparison to that seen in manufacturing, it was nonetheless the steepest recorded for a year.

Average prices charged for goods and services in May rose at the fastest rate since August 2022 amid the growing supply scarcities and the jump in costs.

Goods prices showed a particularly marked rise, the rate of increase hitting the highest since September 2022, but service sector selling price inflation also accelerated to a ten-month high and one of the sharpest rates seen over the past four years.

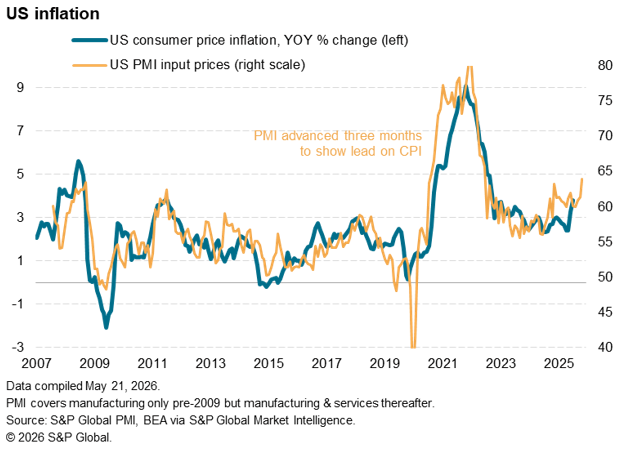

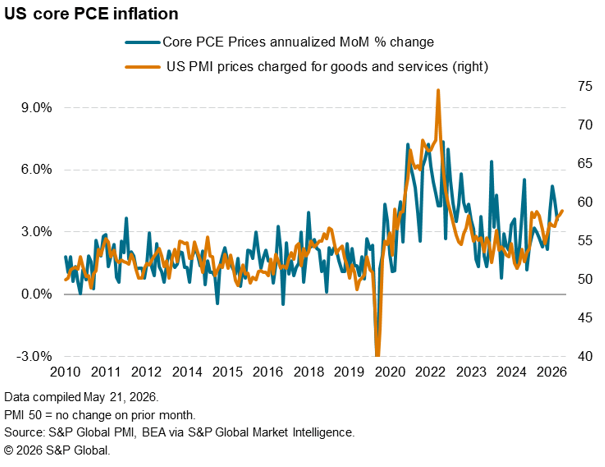

The PMI price indices not only point to a potentially marked increase in headline consumer price inflation in the US, but the data also hint at a further upturn in core PCE inflation, the Fed’s favored inflation gauge.

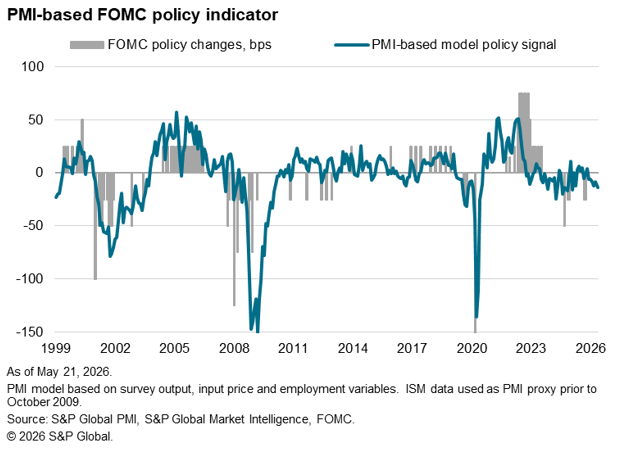

Fed policy

The survey price gauges therefore indicate that inflation looks set to rise further just as the economy cools. The rise in the inflation gauges will add to speculation regarding hikes to interest rates by the FOMC. However, with the survey’s output and employment gauges at historically low levels in May, a crude policy indicator derived from the various policy-sensitive PMI variables hints at an easing bias. Much will naturally depend on the extent to which the inflation indices remain elevated in the coming months, which in turn will be dictated to a large degree by the duration of the conflict in the Middle East and its impact on global supply chains.

Access the latest flash PMI press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings