ECONOMICS COMMENTARY — 21 May, 2026

Eurozone flash PMI signals deepening downturn as war drives prices higher

May’s flash PMI survey data show the eurozone economy taking an increasingly severe toll from the war in the Middle East. Output has now contracted for two successive months, job losses have become more widespread, and the region’s supply shock from the war is intensifying. Supply shortages threaten not only to constrain growth in the coming months but also have the potential to add further upward pressure to inflation, which the survey price gauges already hint at rising sharply in the coming months.

Combined with the growing signs of the region slipping into an economic downturn, the coming inflation spike creates a deepening dilemma for policymakers.

Output falls at fastest rate since October 2023

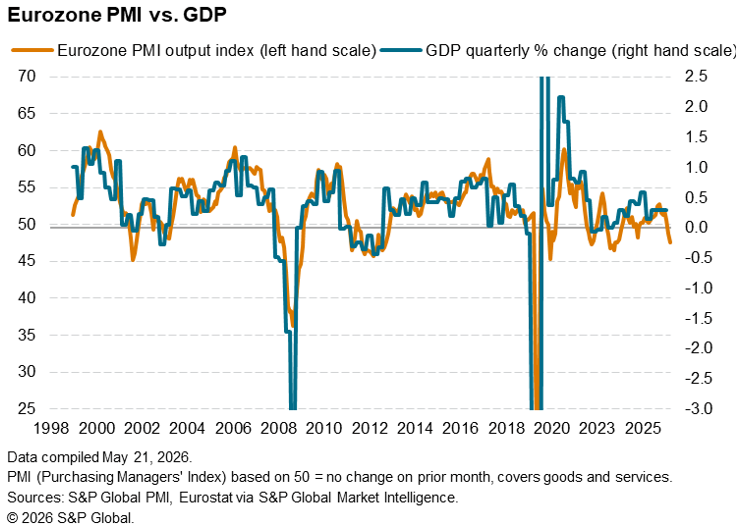

The Eurozone PMI, compiled by S&P Global, has moved deeper into contraction territory in May, according to the early ‘flash’ estimate. The PMI posted 47.5, down from 48.8 in April and below the 50.0 no-change mark for a second successive month. The latest reading signalled the sharpest downturn for just over two-and-a-half years, and indicates that the euro area economy looks set to contract by 0.2% in the second quarter.

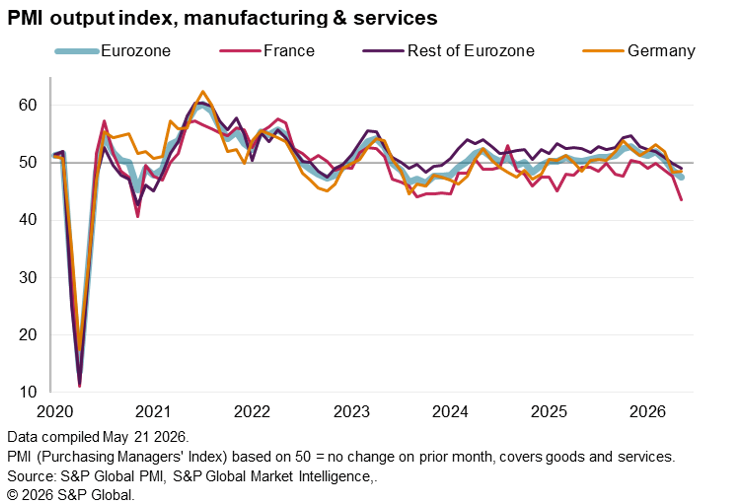

French firms signalled a particularly marked reduction in output during May, reporting the largest drop in output since November 2020, but business activity also decreased in Germany and across the rest of the eurozone as a whole.

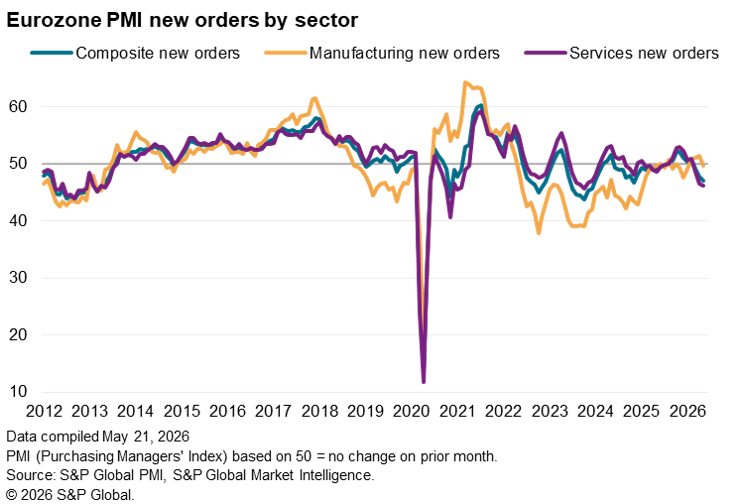

Service sector contracting at steepest rate since 2021

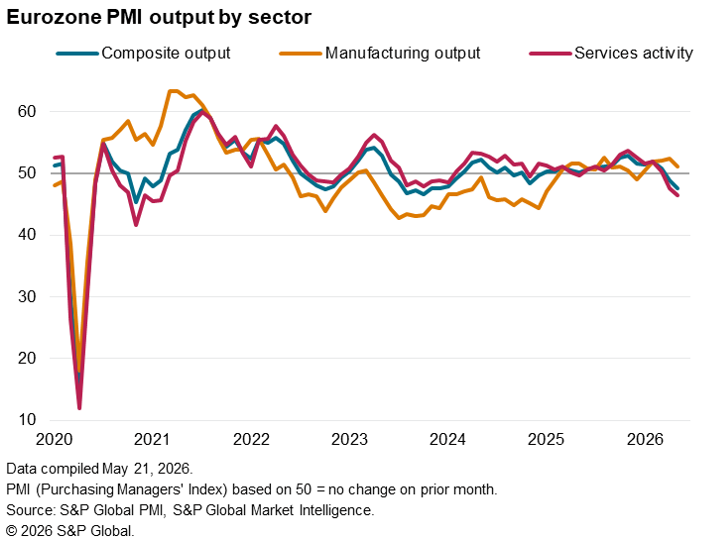

The service sector is being hit especially hard by the surge in the cost of living created by the war, notably via the demand-sapping impact of higher energy prices. However, consumer-oriented sectors such as travel and tourism are also being affected by the war, and financial services firms have noted the damaging impact of higher interest rate expectations. May consequently saw service sector activity decrease at the fastest pace since the COVID-19 disruptions in February 2021.

Manufacturing aided by stockpiling

On the other hand, manufacturing production continued to increase slightly in May, extending the current sequence of growth to five months. The rate of expansion was the slowest since January, however, as new orders ticked down despite ongoing widespread reports of inventory building ahead of further potential price hikes and supply shortages, as had been commonly reported in April.

The data suggest that, while there has been some support to manufacturing from precautionary stock building, this boost is starting to fade, with demand for both goods and services now in decline.

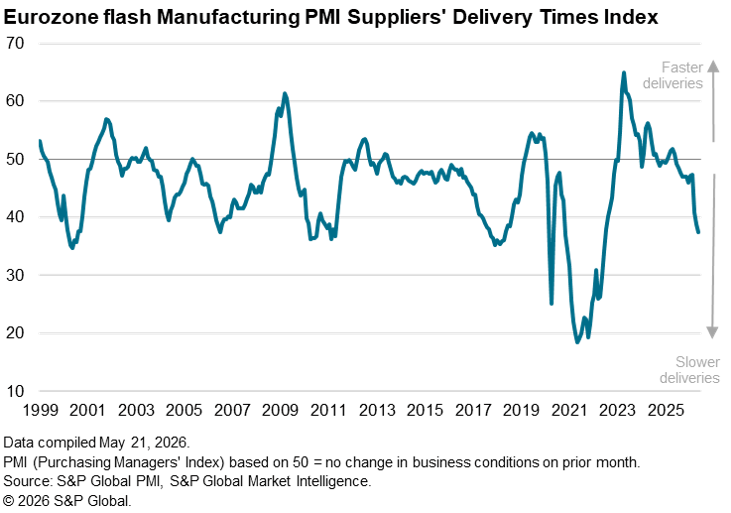

Intensifying supply shock

The region’s supply shock from the war is meanwhile intensifying, as indicated by increasingly widespread supply chain delays. Suppliers' delivery times lengthened markedly in May, and to the largest degree in just under four years. Alongside the direct impact of shipping delays due to the closure of the Strait of Hormuz, the scramble to secure supplies more generally has exacerbated shipping-related issues.

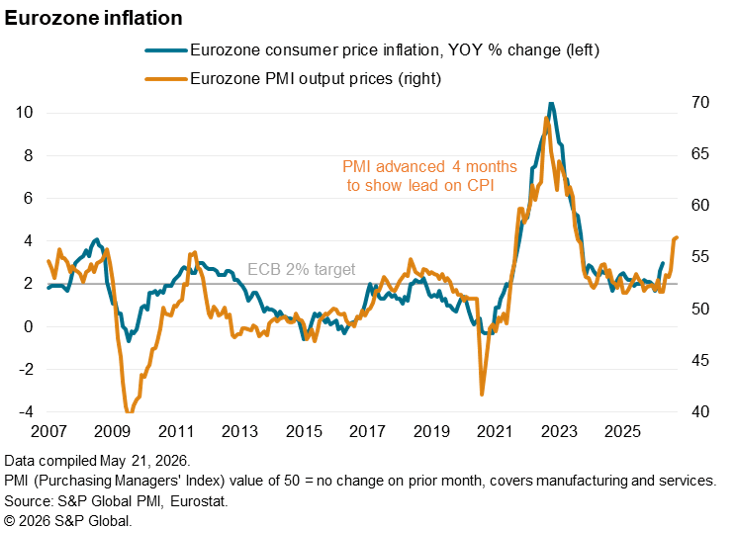

Price surge

Supply shortages threaten not only to constrain growth in the coming months but also have the potential to add further upward pressure to inflation.

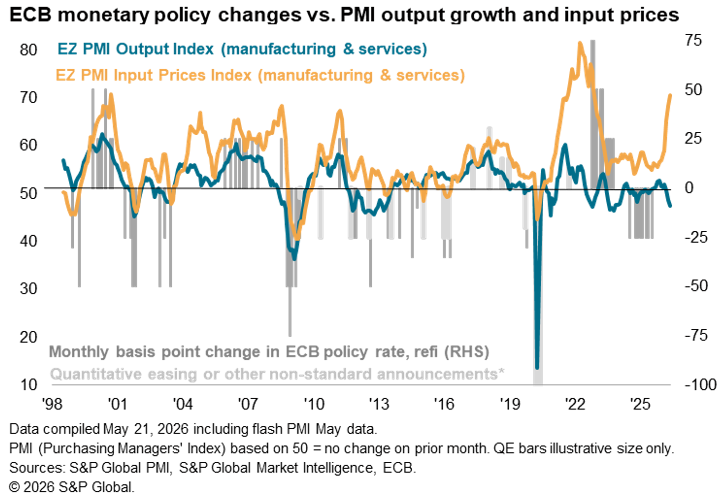

The rise in the survey’s price selling price gauge to a 38-month high already hints at inflation running close to 4% in the coming months which, combined with the growing signs of the region slipping into an economic downturn, creates a deepening dilemma for policymakers.

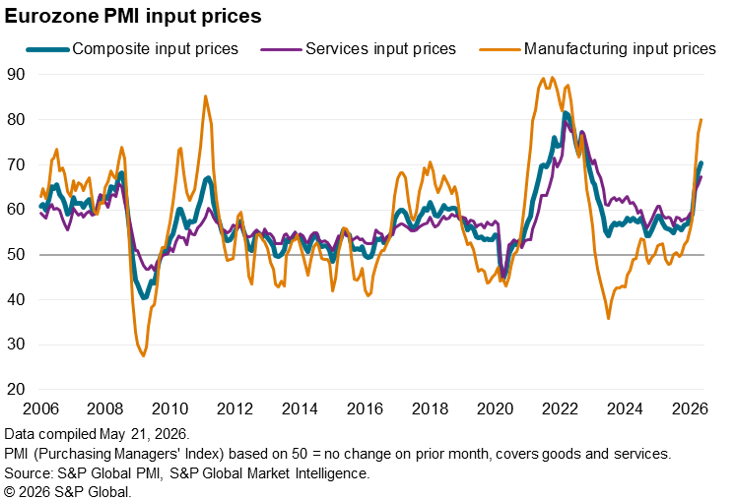

The rate of input cost inflation meanwhile quickened for the seventh consecutive month in May, hitting a four-year high. Steeper rises were seen across both the manufacturing and services sectors, which is likely to put further upward pressure on selling prices in the near-term.

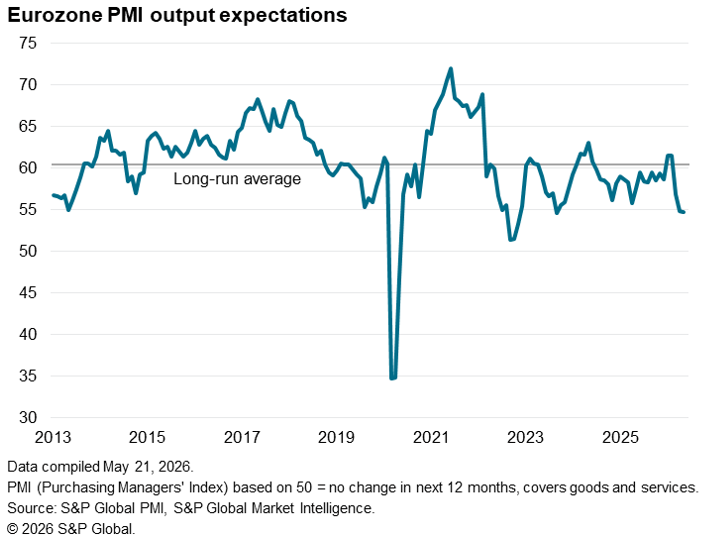

Darker outlook

Business gloom about the year ahead outlook intensified in this environment of falling sales and surging costs. Sentiment is down to its lowest since September 2023, and well below the survey’s long run average. That said, confidence did not slip markedly further compared to April, providing some good news to cling to.

Access the press release here.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings