Research — March 11, 2026

Synopsys poised for stronger growth as Ansys deal expands design reach

By Santosh Saha

US chip design software provider Synopsys Inc. (NASDAQ: SNPS) is poised for a sharp rise in revenue in fiscal 2026 as its $35 billion acquisition of engineering simulation specialist Ansys expands the company’s reach beyond traditional chip design tools and into system-level engineering software.

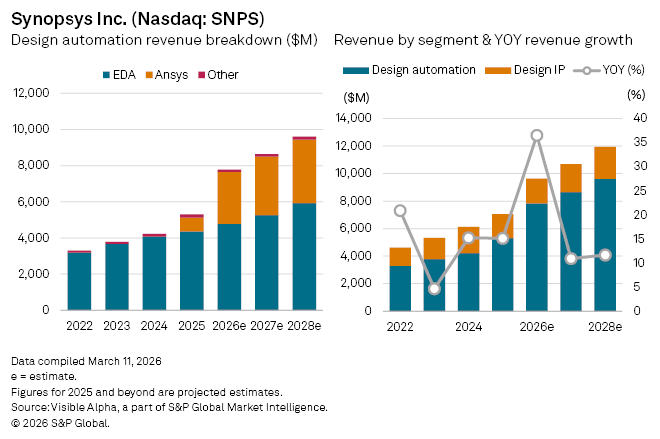

Visible Alpha consensus estimates forecast revenue of about $9.6 billion in fiscal 2026, a 37% year-on-year increase, reflecting the first full-year contribution from Ansys and continued demand for AI-enabled electronic design automation (EDA) tools used by semiconductor manufacturers and systems companies.

The broader Design Automation business, Synopsys’ core segment, is expected to benefit most directly from the acquisition. Analysts forecast segment revenue of around $7.8 billion in fiscal 2026, a 48% increase from last year.

Outside the core software business, Synopsys’ Design IP segment, which licenses pre-built chip components such as processor interfaces, is expected to return to modest growth. Revenue from the unit is projected to rise about 3% in fiscal 2026 after declining by 8% in 2025 amid cyclical weakness in licensing demand.

Profitability, however, is expected to be temporarily pressured by acquisition-related costs. Analysts project net income to fall 51% to roughly $648 million in fiscal 2026 as integration expenses and amortization of acquired assets weigh on earnings. Net income is then forecast to rebound sharply in fiscal 2027, rising 123% to about $1.4 billion as synergies begin to materialize.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment