Guide to P&C Insurance KPIs

This guide highlights the key performance indicators for the property and casualty (P&C) insurance industry and where investors should look to find an investment edge.

Industry Overview

The property and casualty (P&C) insurance industry is a key segment of the larger insurance industry. It includes companies whose primary business is to provide insurance coverage for property or other physical assets, and to provide casualty or legal liability coverage.

Key Property and Casualty Insurance Industry Metrics

Key performance indicators (KPIs) are the most important business metrics for a particular industry. When understanding market expectations for Property and Casualty Insurance, whether at a company or industry level, here are some of the P&C Insurance KPIs to consider:

- Net Earned Premium (NEP)

- Net Investment Income

- Policy-related Costs (aka Losses Incurred or Net Claims Incurred)

- Underwriting Margin

- Pre-tax Margin

- Retention Ratio or Reinsurance Retention Ratio

- Loss Ratio

- Combined Ratio

- Catastrophe Losses (CAT Loss)

- Premium-to-Surplus Ratio

- Annualized Investment Yield

- Return on Equity

- Book Value per Share

{kind=link}

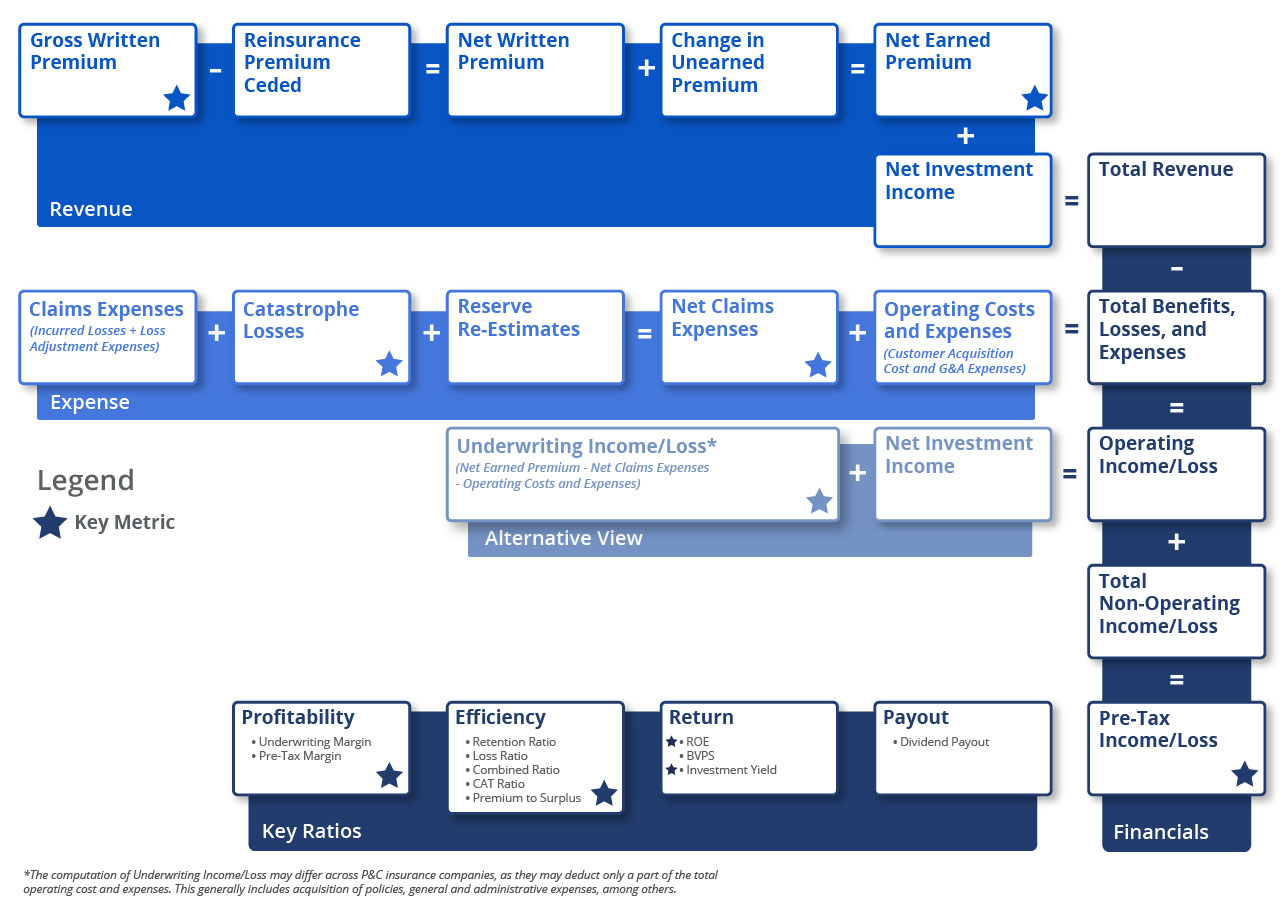

P&C Industry Business Model

-

Expenses

-

Revenue

-

Other Financial Statement Items

-

Ratios Used To Analyze P&C Insurance Stocks

Incurred losses can be in the form of either paid claims (the amount paid to the policyholders) or expenses associated with establishing a loss reserve to pay a claim in the future.

A loss reserve is a liability on an insurance company’s balance sheet. When a claim that has been reserved is paid, the loss reserve, as well as the cash, shrinks by that amount.

Along with the paid claims, an insurance company must also pay, or reserve for, loss adjustment expenses (LAE), which are reserves set aside for legal fees to investigate and settle insurance claims. Incurred losses along with loss adjustment expenses are recognized as total policy-related costs, which account for a major portion of the total costs and expenses of an insurance company and vary depending on the line of insurance business.

Policy-related costs may also include catastrophe losses and reserve re-estimates (change in reserves during a period).

Catastrophe losses arise from infrequent events that cause severe losses, injury, and/or property damage to a large population, as in the case of natural disasters. For P&C insurers, catastrophe losses can lead to large losses, impacting capitalization and requiring a distinct risk management approach. Catastrophe losses can create significant financial pressures for an insurance company, reducing earnings and statutory surpluses, possibly forcing asset liquidation to meet cash needs, and bearing the risk of a rating downgrade.

Reserve re-estimates are the changes in loss reserves. Loss reserves are typically the largest liability on a P&C insurance company’s balance sheet and are evaluated closely when analyzing the financial statements. Loss reserves are established for both claims that have been reported to the insurance company (case reserves) and for claims that are yet to be reported to the insurance company (incurred but not reported, or IBNR). When premiums increase for a P&C insurer, risk exposures also increase and the associated loss reserves expand.

The number of catastrophe losses and an increase/(decrease) in loss reserves (i.e. reserve re-estimates) have a direct impact on policy-related costs and simultaneously on operating incomes. An increase in catastrophe losses or reserves impacts policy-related costs positively and operating income negatively. The reserve level maintained by P&C insurance companies is highly subjective and could vary depending on the management’s decisions. In terms of disclosures, certain jurisdictions require insurance companies to disclose their annual P&C reserves in detail.

When an insurance company underwrites a policy, it charges a premium called the gross written premium (GWP). To manage the risk along with its capital needs, most insurance companies buy reinsurance by paying a ceding premium to a reinsurer. This premium is called the reinsurance premium ceded.

Net written premium (NWP) is what an insurance company is left with after paying the reinsurance premium; in other words, it is the gross premiums written by the insurance company minus the ceding premium, plus any reinsurance assumed.

The premium earned on the portion of an insurance contract that has expired is called net earned premium (NEP). These premiums are typically earned on a pro-rata basis over the life of a policy. Earned premiums are a major source of revenue for an insurance company. From an accounting and financial modeling perspective, the earned premium is calculated as NWP plus the net change in unearned premium.

An unearned premium is a premium collected by an insurance company, where the underlying portion of the insurance contract has not expired. In the case of premature termination of a contract, these premiums are returned to the policyholder.

Operating costs and expenses include expenses related to customer acquisitions and other general and administrative expenses.

When premium revenue is sufficient to cover both underwriting expenses and claims, an insurance company generates an underwriting income. On the contrary, when the premium revenue is insufficient, it generates an underwriting loss. The process of underwriting involves collecting premiums, paying for losses and paying underwriting expenses.

Net investment income is the second most important contributor to total revenue for most insurance companies, after earned premiums. Between collecting premiums and paying claims and expenses, there is an interval when an insurance company invests funds collected as premiums in various securities and investment vehicles. The interest and dividend income generated from these investments account for a bulk of the overall operating earnings for most insurers.

The earnings stability that P&C insurers are known for often comes from the predictable and highly recurring nature of their investment income. However, the returns earned and the long-term growth of their investments depend on the level of interest rates.

Other income/loss typically represents realized gains (or losses) generated from the sale of securities or credit impairments, which also contribute to the revenue of P&C insurers. Although realized gains generally flow through the income statement of a P&C insurer and are added to retained earnings, they are not considered while computing operating earnings.

Retention ratio (net written premium / gross written premium) measures the efficiency of a P&C insurance company. It exhibits the percentage of businesses covered by the insurance company which is not transferred to the reinsurance companies. Companies with efficient underwriting decisions have higher retention ratios, which in turn drives higher profitability. However, reinsurance through risk spreading increases the stability of the company.

Loss ratio (policy-related costs / net premium earned) measures the underlying efficiency of a P&C insurance company and its ability to manage claims. A higher loss ratio indicates a higher number of paid claims, which can be an indicator of financial distress.

The combined ratio (loss ratio + expense ratio) measures the overall underwriting efficiency of a company. A combined ratio of 100% means that an insurer is breaking even on its underwriting activities.

The catastrophe ratio (catastrophe losses / net earned premium) measures catastrophic losses as a percentage of net earned premium. A higher catastrophe ratio will hit the underwriting earnings of the company which in turn hits the profitability of the company.

Return on equity (ROE) (net income/(loss) / average stockholders’ equity) measures the return per dollar on equity investments. Profitability for all business activities is measured through ROE. A lower ROE indicates poor underwriting discipline or less than adequate returns on investments relative to the cost of capital. The metrics used in the diagram below are often used by analysts to break down the ROE based on the contributions from core insurance operations (i.e. operations which exhibit underwriting efficiency) and from investment operations (i.e. operations which depict investing efficiency) of the P&C insurance business.

Premium-to-surplus ratio (premium written, net / (total assets – total liabilities)), also known as underwriting leverage, measures the efficiency with which an insurance company uses its capital resources to generate business. A relatively low premium-to-surplus ratio indicates the underutilization of capital, which means the company has more room for growth without having to dilute existing shareholders’ resources. Less volatile insurance products (such as personal auto insurance) have higher underwriting leverage while high volatile insurance products (such as property catastrophe insurance) have lower underwriting leverage. Aggressive underwriting may lead to significant losses, especially in soft markets, which are characterized by stable or falling premium rates, relaxed underwriting conditions, and increased capacity of an insurer, among other things). This ratio also measures a company’s exposure to pricing errors in its current book of business. Net written premium indicates potential losses due to underpricing of policies, while policyholder surplus indicates the cushion available to absorb such losses.

Underwriting margin (underwriting profit/(loss) / premium earned, net) measures the profit that a P&C insurer derives from insurance operations only (i.e. excluding investments).

Investment yield (net investment income / investments) measures the profitability of investments and purports to reflect the ability to manage investments successfully.

Investment leverage is defined as invested assets divided by equity. Invested assets are largely the investment portfolio built up from the premiums collected by a P&C carrier. The average of the P&C industry’s investment leverage depends on the length of the tail or the claims payout period.

Book value per share is a popular ratio for P&C insurance business and is measured as total stockholders’ equity excluding minority interest & preferred shares / number of shares outstanding. P&C insurance business is a capital intensive or balance sheet-based business, where book value per share is an important metric used for valuation purposes. Additionally, most assets and liabilities of P&C companies are constantly valued at market prices.

Tangible book value per share is an enhancement to book value per share and is measured as total stockholders’ equity excluding minority interest & preferred share – intangible assets / number of shares outstanding.

Return on assets (ROA) (net income/(loss) / average assets) is an indicator of how well a company utilizes its assets, determined by how profitable a company is with respect to its total assets. ROA gives a manager, investor, or analyst an idea of how efficient a company’s management is at utilizing its assets to generate earnings.

Available Comp Tables - Consensus Estimates

Visible Alpha offers comp tables, comparing forecasts for key financial and operating metrics, to make it easy to quickly conduct relative analysis. Every pre-built, customizable comp table is based on region and/or key operating metrics.

Global Financial and Operating KPIs Company Examples:

Americas

- Chubb Ltd. (CB_US)

- Travelers Cos Inc. (TRV_US)

- Allstate Corp. (ALL)

- American International Group, Inc. (AIG)

- Progressive Corp. (PGR)

EMEA

- Direct Line Insurance Group Plc. (DLG_UK)

- Lancashire Holdings Ltd. (LRE_UK)

- Beazley Plc. (BEZ_UK)

- Aviva. (AV_UK)

- Allianz SE. (ALVG_DE)

APAC

- PICC Property & Casualty Co Ltd. (2328_CN)

- China Pacific Insurance (2601_CN)

- People’s Insurance Company (Group) of China Limited (1339_CN)

- Ping An Insurance (601318_CN)

- Samsung Fire & Marine (000810_KR)

Download Report

This guide highlights the key performance indicators for the P&C insurance industry and where investors should look to find an investment edge, including:

- Property and Casualty Insurance Industry Business Model & Diagram

- Key P&C insurance Metrics PLUS Visible Alpha’s Standardized Industry Metrics

- Available Comp Tables

- Industry KPI Terms & Definitions