Battery Metals Exploration Trends 2026

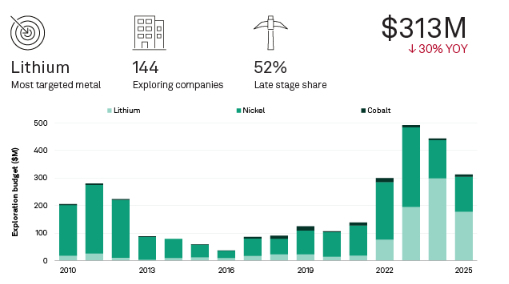

Global exploration budgets for lithium, nickel, and cobalt fell 43% year over year to $958M in 2025, marking the first major contraction since 2022 as oversupply, weak prices, and tighter financing reshaped priorities. Yet the pullback isn’t uniform. Canada has emerged as the top exploration hub across battery metals, supported by advanced assets and an expanding set of incentives and streamlined processes that are helping projects stay funded even as juniors tighten spend.

Gain strategic insights into:

- Key trends in global battery metals exploration for 2025

- Top regions leading exploration, including Canada and Australia

- Main factors influencing investment shifts

- Highlights of emerging exploration frontiers

- Insights on future supply chain impacts