Research — August 14, 2025

US coal markets remain quiet to open summer

By Steve Piper

US coal market prices held flat again in July despite supportive summer load and natural gas prices. Production and shipments remain elevated year over year, with gains slowing amid sufficient inventories.

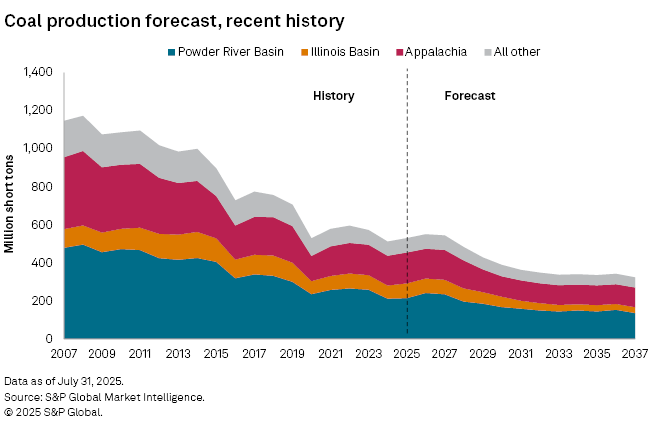

Through 2027, higher natural gas prices are expected to support increased coal generation, driving stable or growing coal production. After 2027, the US coal market is forecast to face pressure from the expansion of zero-carbon electricity, incentivized in part by the Inflation Reduction Act. Overall, the S&P Global Market Indicative Power Forecast projects 44.3 GW of coal plant retirements by 2035, while 808.4 GW of renewable capacity is forecast to come online. Coal plants are forecast for significantly reduced generation over this period as US electricity demand for coal declines 50.7%, and generation from coal plants accounts for just 7.0% of total generation.

However, a recent report by S&P Global Commodity Insights estimates that a full repeal of green energy tax credits could boost coal's 2035 generation share to 7.9%, compared to previous forecasts. While overall declines in coal demand remain likely, the enactment of the One Big Beautiful Bill Act, combined with recent increases in gas generation construction costs, could improve coal's generation share relative to current forecasts.

➤ US coal prices remained stable in June, with production and shipments showing year-over-year growth as coal plants prepare for strong summer demand.

➤ The S&P Global Market Indicative Power Forecast predicts 44.2 GW of coal plant retirements by 2035, with coal's share of electricity generation expected to decline significantly as renewable energy capacity increases, driven by the Inflation Reduction Act.

➤ Current coal shipments averaged 10.4 million short tons for the four weeks ending July 26, essentially the same as June and a 6% increase compared to the same period last year.

➤ The production outlook varies by region, with the Powder River Basin and Illinois Basin expecting stable production through 2027, while Appalachian coal production is forecast to decline due to reduced domestic demand and limited export growth.

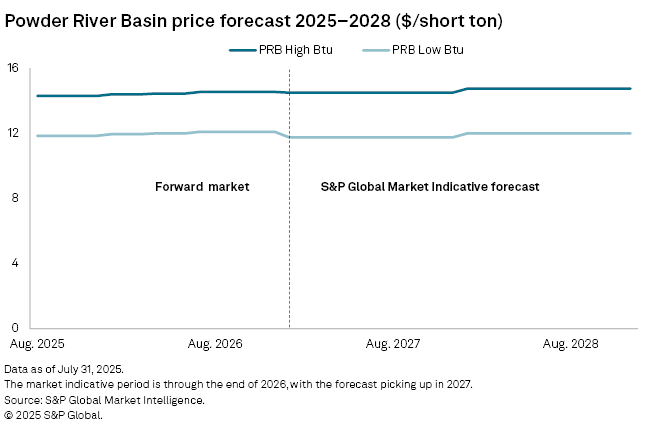

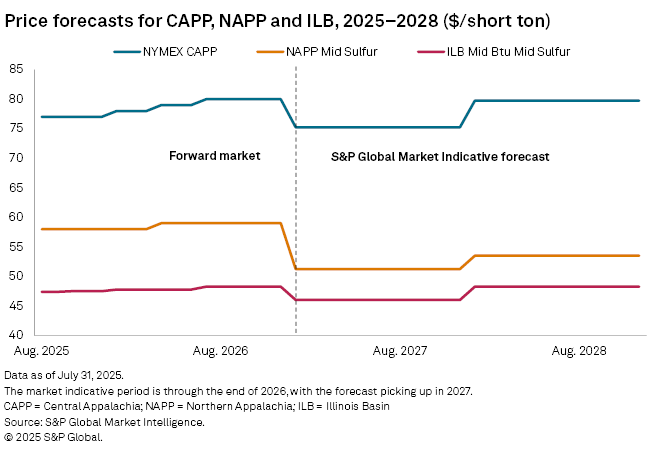

Coal prices were flat in July, unmoved by firmer electricity demand and natural gas prices. Benchmark export coal prices held, with CAPP region export benchmarks at $79.00/short ton, NYMEX CAPP at $77.00/short ton, and NAPP Pittsburgh Seam 13,000 Btu per pound at $58.00/short ton. Illinois Basin 11,500 mid-sulfur closed July at $47.75/short ton, while the NYMEX Powder River Basin benchmark held flat at $14.30/short ton.

Natural gas prices gained during July on warm weather in the first half of the month before easing by month's end. Henry Hub spot gas opened at $3.26/MMBtu and moved to a mid-month high of $3.52/MMBtu before easing to close the month at $2.98/MMBtu. Spot prices averaged $3.21/MMBtu for the month, continuing a trend of modest price growth into the summer. As in June, storage refill picked up to take advantage of the lull in prices in late July, with working gas at 3,123 Bcf as of July 25. This is 195 Bcf above the five-year average, and 123 Bcf below the same week of 2024.

Regional gas market discounts narrowed in July, driving an across-the-board rise in spot natural gas prices. Chicago Gate averaged $2.96/MMBtu, a $0.25/MMBtu discount to Henry Hub. TCO Pool's discount shrank to $0.38/MMBtu at $2.83/MMBtu, while TETCO M3's discount was $0.34/MMBtu at $2.87/MMBtu. SoCal Border's discount shrank to $0.16/MMBtu for an average monthly spot price of $3.05/MMBtu.

The US Energy Information Administration estimated April 2025 coal stockpiles at 116 million short tons, a 4 MMst increase from March. Steady coal prices in the past two months are partly attributable to these early spring inventory gains.

Current forward pricing for PRB coal has been stable, reflecting sufficient inventories at power plants and mining capacity to increase production as needed against firmer natural gas prices. After 2027, lower natural gas prices and declining coal demand are forecast to restrain price growth.

Bituminous coal price levels are primarily influenced by export markets, with today's price levels making domestic coal generation generally less competitive against Northeast natural gas. Firmer eastern natural gas prices have nevertheless boosted first-half 2025 demand, even as seaborne coal demand is expected to decline 6.7% year over year due to reduced demand from India and China.

Pricing benchmarks exceeding $65/short ton suggest sustainable returns for eastern bituminous coal. After declining last year, bituminous coal demand for electric generation is expected to remain stable through 2027 on higher electricity demand and more supportive natural gas prices. Declines in steam coal demand are expected to resume after 2027, and overall Eastern US coal demand is forecast to decline 78 MMst from 2025–2030.

Outlook for US coal production, demand

For the four weeks ending July 26, coal shipments averaged 10.4 MMst, 6% higher than this time last year. Lower year-over-year gains in shipments align with growing inventories and flat prices, despite favorable spreads to natural gas prices.

The chart below compares the current production forecast with recent history. We forecast increased coal demand against higher natural gas prices through 2027. Gas to coal switching reduced coal inventory surpluses from the end of 2024, setting up production growth this year. We now forecast coal production at 530 MMst, an increase of 18 MMst (3.5%) from 2024 levels. Coal generation is forecast to further gain market share from natural gas through 2027, until relative coal and gas pricing normalizes and expanding green energy again puts pressure on coal generation. The overall coal market, including domestic demand and exports, is forecast to decline by 172 MMst between 2025 and 2030.

Production outlook — Powder River Basin

First quarter 2025 production reports of the Mine Safety and Health Administration (MSHA) indicate quarter-end production at 54.9 MMst, an annualized rate of 219.4 MMst. Production is now forecast at 215 MMst in 2025, as demand more than offsets 2024 year-end inventory levels. With inventory levels normalized, production is forecast for modest growth through 2027 against higher natural gas prices. By 2030, Commodity Insights projects that coal generation retirements in the Midwest and a substantial expansion of wind generation in Powder River Basin's core markets will shrink coal demand to 164 MMst, further declining to 143 MMst through 2035.

Production outlook — Illinois Basin

First quarter 2025 production reports of the MSHA indicate quarter-end production at 18.8 MMst, or an annualized rate of 75.1 MMst. We forecast stable annual production through 2027, ranging between 76-77 MMst per year. After 2027, the expansion of wind generation incentivized by the Inflation Reduction Act and announced coal retirements are forecast to erode Illinois Basin coal demand. Coal production in the Illinois Basin is forecast to fall to 54 MMst by 2030, further declining to 33 MMst by 2035.

Production outlook — Appalachian basins

First quarter 2025 production reports of the MSHA indicate quarter-end production at 39.8 MMst, or an annualized rate of 159.2 MMst. Appalachian coal demand tends to be more sensitive to global seaborne markets than to domestic natural gas prices, compared to the Powder River Basin or the Illinois Basin. While the Illinois Basin and Powder River Basin are forecast for improved demand against natural gas generation, gains in Appalachian coal will therefore be more limited. We forecast production at 163 MMst, 3.8% higher than 2024. As remaining domestic demand erodes after 2027, with only modest offsets from export growth, Appalachian production is forecast to fall to 108 MMst by 2030.

Further information

Market indicative coal forecasts by Commodity Insights represent forward curves for spot-traded instruments analogous to a strip of contracts. The shorter tenors — current year and prompt year, plus additional years, if available — are driven by the observed/assessed market. The longer tenors — typically forecast years three to 20 for physically assessed markers — are driven by fundamental estimates of cash costs of production, accepted returns to capital, regional productive capacity, and forecast supply and demand. For the long-tenured portion of the curve, Commodity Insights forecasts prices for specific coal markers and defines the remaining markers via historical spreads.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Regulatory Research Associates is a group within S&P Global Commodity Insights.

S&P Global Commodity Insights produces content for distribution on S&P Capital IQ Pro.

For further details on coal prices, supply and demand, visit the S&P Coal Forecast Summary page.

Content Type

Theme

Location

Products & Offerings

Segment