ECONOMICS COMMENTARY — May 17, 2022

Global commodity price and supply indicators signal semiconductor shortage showing signs of peaking

By Jingyi Pan

The S&P Global PMI™ Commodity Price and Supply Indicators track the development of price pressures and supply shortages each month for at least 20 items using responses gathered from the S&P Global Manufacturing PMI survey. Amongst which, semiconductors saw the most severe upward price pressure in April. That said, there are hints of supply shortages and price increases peaking for semiconductors, even as the situation remain severe by historical standards.

Price increases and supply shortages remain at worrying levels in April

The latest data from the Global PMI Commodity Price & Supply Indicators by S&P Global indicated that manufacturers worldwide continued to see sustained price and supply pressures in April. In both cases, price increases and supply delays have risen in terms of rate of growth and incidence again in recent months, after showing some signs of easing in the second half of last year, amid the twin shocks of the Ukraine war and new COIVID-19 lockdowns in mainland China.

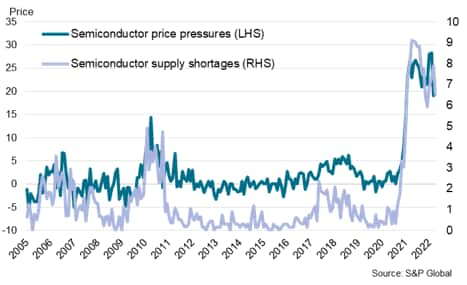

Global Commodity Price & Supply Pressures: All Items

The Global Supply Shortages Index - calculated from the number of times items have been listed to be in short supply each month, whereby an index value above 1.0 indicates that supply shortages are above the long-run average and the higher the figure, the greater the degree of shortages relative to the trend - was unchanged from March's four-month high.

Likewise, the price pressure index - calculated using a similar methodology of the number of purchasing managers reporting a specific item to have risen in price during a survey month less the number reporting that item to have fallen in price - also stayed unchanged from March. All of which pointed to persistent and elevated supply issues and inflationary pressures.

Of the items tracked, transport was reported to be facing the most severe shortage in supply, although it was semiconductors that continued to face the steepest price pressures in April.

April sees fewer reports of semiconductor price increases and short supply

That said, diverging from the worsening trend for all items, semiconductor price pressures and supply shortages either receded or stayed little changed in April. Shortages of semiconductors eased from around eight times the long-run average in March to under seven times the normal level, while price pressures were almost unchanged at around 20 times the normal level. Although these remained elevated at many times their long-run averages to indicate sustained pressures, they have clearly departed from the heights registered in mid-2021 and early-2022.

Global Commodity Price & Supply Pressures: Semi-conductors

Stabilising price and supply indicators hint at peaking chip cycle

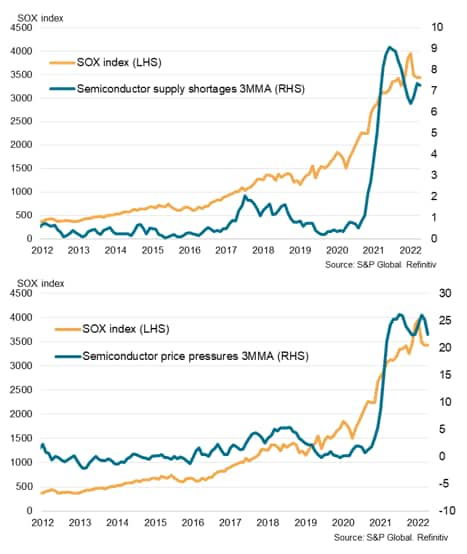

Examining the short supply and price pressure indicators alongside equity price movements, we look at how these PMI gauges correlate with the SOX index. The Philadelphia semiconductor index, known as SOX, is a market capitalization-weighted index comprising 30 companies that are primarily involved in the design, distribution, manufacture and sale of semiconductors. Funds based on the SOX include the likes of the iShares Semiconductor ETF (SOXX).

The SOX index was seen rising in tandem with the semiconductor price pressure index over 2020 and 2021 amid shortages and spiking demand. As mentioned above, the short supply and price pressure indicators for semiconductors reflected that some of these factors that led to the phenomenal rise in semiconductor-related company share prices appear to be stabilising into the start of Q2 2022.

The SOX index was seen peaking around January, with prices having since fallen 13% in the first quarter of 2022 and clocking further declines in April. While weak risk sentiment had a part to play, with investors concerned about monetary policy and geopolitics (according to the S&P Global Investment Manager Index), signs of the chip cycle peaking inject little confidence for prices to trend otherwise. As far as the trend is observed of semiconductor supply shortages, using a three-month moving average assessment of the PMI-based index, global manufacturers are not seeing the overall supply situation worsening when compared to 2021. Likewise is the case for price pressures.

Evidently uncertainty persists in the near to medium term, including how fast demand from China may bounce back from the current COVID-19 disruptions, but the shortage-driven boost for semiconductor prices may be running out of air according to the latest indications.

Global semiconductor supply shortages and price pressures vs. SOX index

Sign up to receive updated commentary in your inbox here.

Jingyi Pan, Economics Associate Director, S&P Global Market Intelligence

jingyi.pan@spglobal.com

© 2022, IHS Markit Inc. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI™) data are compiled by IHS Markit for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.