Research — June 9, 2026

Snowflake postQ: Outlook lifted as AI momentum drives Q1 beat

By Nitin Kansal

Snowflake Inc. (NYSE: SNOW) delivered a strong set of Q1 2027 results, surpassing Visible Alpha consensus expectations on both revenue and profitability as enterprise demand for data and AI workloads continued to accelerate. The upside was driven by robust product revenue growth, increasing traction in AI offerings, and ongoing expansion of its core data cloud platform. Management raised both near-term and full-year guidance, signaling confidence in sustained consumption trends and growing contributions from its AI portfolio, particularly the Cortex Code.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

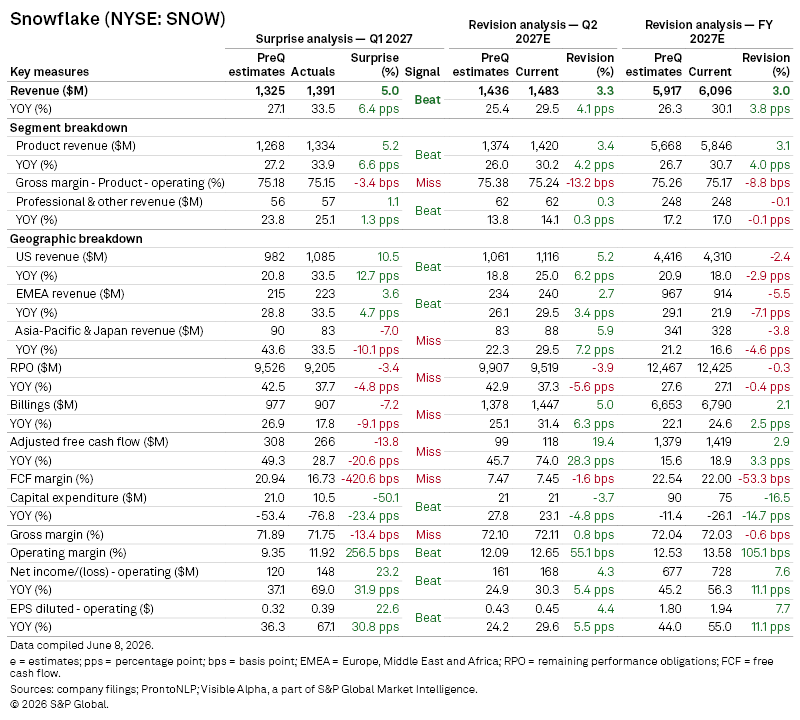

Q1 revenue rose 34% year-on-year to $1.39 billion, beating Visible Alpha consensus expectations by 5%, while product revenue, the company’s largest segment, increased 34% to $1.33 billion, exceeding expectations by 5.2%. Regionally, US remained a standout, with revenue rising 34% and beating consensus expectations by 10.5%, while EMEA delivered a modest beat. Asia-Pacific and Japan, however, lagged, coming in 7% below consensus.

Profitability was a clear highlight. Non-GAAP net income climbed 69% year-on-year to $148 million, surpassing expectations by 23.2%, while operating margin expanded to 11.9%, beating forecasts by 257 basis points. Non-GAAP diluted EPS of $0.39 was 22.6% ahead of consensus. Gross margin of 71.75% was broadly in line, missing expectations of 71.89%.

Some forward-looking indicators were softer. Remaining performance obligations (RPO) rose 38% year-on-year to $9.2 billion, but fell 3.4% short of expectations, while billings increased 17% to $907 million, missing by 7.2%. Adjusted free cash flow grew 29% to $266 million but came in 13.8% below consensus. Capital expenditure declined sharply, down 77% year-on-year to $10.5 million, reflecting a continued strategy of leveraging partner infrastructure rather than investing heavily in owned hardware.

Guidance

Management’s outlook reinforced the strength of underlying demand.

For Q2 2027:

- Product revenue is expected in the range of $1.415 billion –$1.420 billion, implying around 30% year-on-year growth and ahead of pre-quarter consensus of $1.374 billion.

- Non-GAAP operating margin is guided to approximately 12.5%, also above expectations.

For the full year:

- Snowflake raised product revenue guidance to $5.84 billion, implying roughly 31% growth and ahead of the $5.67 billion preQ consensus estimate.

- Product gross margin is expected to hold at around 75%, despite rising AI-related costs

- Operating margin guidance was lifted to 13.5% from 12.5%

- Adjusted free cash flow margin was reiterated at approximately 23%, modestly above consensus.

Management commentary

Cortex Code was highlighted as a major contributor to the upgraded outlook, accelerating customer migrations and data projects while driving incremental consumption across the platform. This dynamic is creating a “flywheel” effect, reinforcing long-term growth.

Management also pointed to improved sales productivity driven by AI-enabled workflows, alongside strong customer additions and broad-based execution across regions and industries. The company positioned its evolving AI stack, including Snowflake Intelligence and Cortex Code, as forming an “agentic control plane” for enterprise data, applications and workflows.

Snowflake argued that its integrated platform, governance capabilities and ecosystem partnerships differentiate it from standalone AI tools, particularly as enterprises seek secure, scalable deployment. As AI adoption expands, the company is also investing in cost-governance features to help customers manage spending across increasingly complex AI workloads.

Strategic positioning reinforced at Snowflake Summit

Snowflake positioned its Summit 2026 keynote around the “agentic enterprise” — a framework where AI agents operate across data, models and applications to automate workflows and support decision-making.

CEO Sridhar Ramaswamy outlined four required layers: governed enterprise data, AI models, enterprise applications and an agentic control plane to orchestrate them, emphasising Snowflake’s role as the coordination layer.

Key product introductions included Snowflake Intelligence, a natural-language work agent for querying data and triggering actions across apps, and Cortex Code (CoCo), an AI coding agent aimed at accelerating migrations, pipeline development and application buildouts.

The company also announced intent to acquire Noto, expanding MCP-based connectivity to enterprise tools including Gmail, Slack, Jira, GitHub, Microsoft 365 and Zoom, further extending Snowflake’s governed access layer across enterprise systems.

A core message was that enterprise data, not AI models, is the key competitive advantage, with Snowflake positioning itself as the governance and orchestration layer for AI at scale. Customer examples from Canva, Nestlé, Accenture and Sanofi highlighted real-world adoption in data unification, automation and AI deployment.

Share price reaction

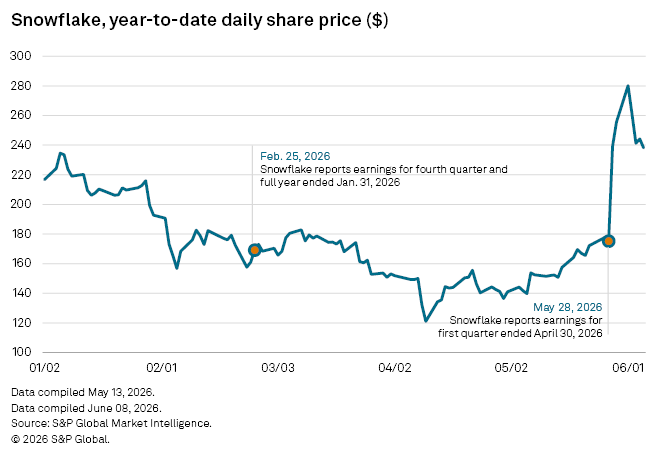

Shares moved sharply higher following the earnings release, supported by the earnings beat, raised guidance and continued evidence of strong AI-driven demand. Investor sentiment was further buoyed by a newly announced five-year, $6 bn commitment with Amazon Web Services, reinforcing confidence in long-term consumption growth.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment