Research — June 3, 2026

Salesforce postQ: Strong earnings overshadowed by cautious outlook

By Santosh Saha

Salesforce Inc. (NYSE: CRM) delivered a solid Q1 2027 earnings, with revenue modestly ahead of expectations and a more pronounced upside in margins and earnings. Operating leverage, disciplined cost control and early benefits from AI-led productivity helped drive a stronger-than-expected bottom line, even as softer bookings and renewal trends tempered the near-term growth outlook.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

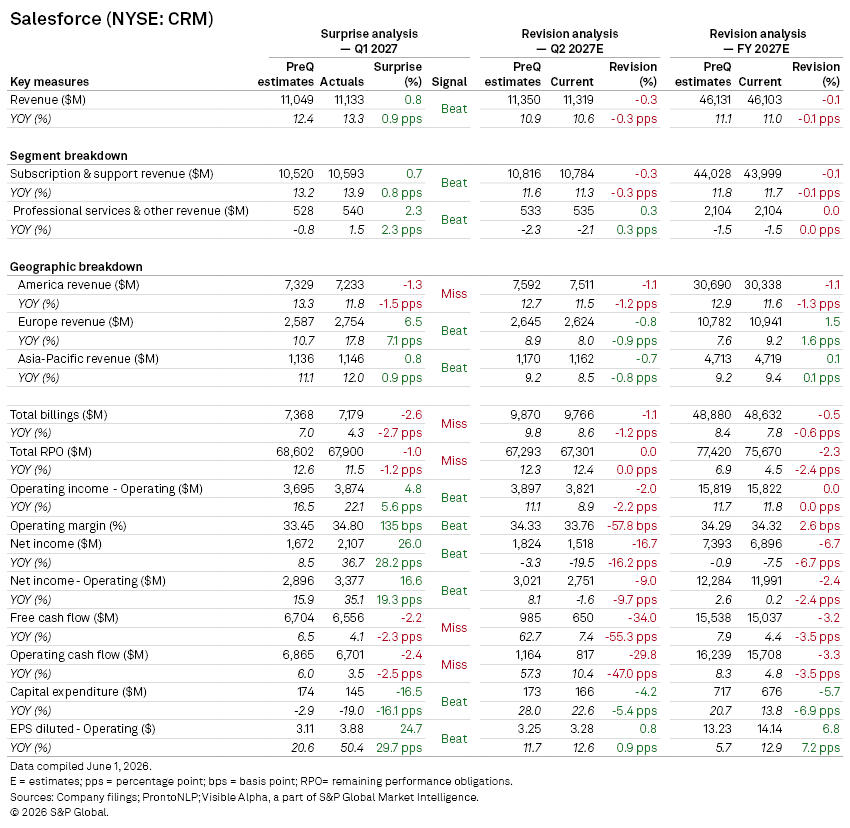

Q1 revenue rose 13.3% year-on-year to $11.1 billion, modestly ahead of Visible Apha consensus expectations, supported by resilient subscription demand, early contributions from Informatica and continued enterprise adoption of AI-driven tools. Subscription and support revenue, the company’s largest revenue segment, grew 13.9% to $10.6 billion, while professional services revenue of $540 million also came in ahead of expectations.

Geographically, the performance was mixed. Revenue from the Americas grew 11.8% to $7.2 billion but fell slightly short of consensus expectations, while Europe provided a clear upside surprise, rising 17.8% to $2.8 billion. Asia-Pacific revenue increased 12.0% to $1.1 billion, modestly beating expectations.

Profitability remained standout. Operating margin expanded to 34.8%, around 135 basis points ahead of consensus, driving a 22.1% increase in operating income to $3.9 billion. Non-GAAP diluted EPS of $3.88 exceeded expectations by nearly 25%.

Billings rose just 4.3% to $7.2 billion, missing expectations, while remaining performance obligations (RPO) grew 11.5% to $67.9 billion but also came in slightly light.

Cash flow generation remained strong despite financing-related headwinds. Operating cash flow increased 3.5% year-on-year to $6.7 billion, while free cash flow reached $6.6 billion, both coming in below expectations due to debt issuance linked to the company’s $25 billion accelerated share repurchase program. Capital expenditure declined 19% to $145 million, reflecting continued infrastructure efficiency.

Guidance

For Q2 2027, Salesforce guided revenue of $11.27 billion–$11.35 billion, implying 10–11% growth, broadly in line with consensus, with just over four percentage points of contribution from Informatica. Non-GAAP EPS guidance of $3.25–$3.27 was also in line with preQ consensus expectations of $3.25.

For the full year, management raised revenue guidance to $45.9 billion–$46.2 billion (around 11% growth), again broadly matching consensus, while significantly lifting non-GAAP EPS guidance to $14.06–$14.12, well ahead of expectations. Free cash flow growth is now expected at 4–5%, reflecting the impact of debt-funded shareholder returns.

Subscription and support revenue growth guidance was maintained at just under 12%, with non-GAAP operating margin guidance reiterated at 34.3%.

Analyst Q&A highlights

Management struck a confident tone on second-half acceleration, citing improving deal sizes, lower attrition and stronger Informatica momentum. AI remains central to the story: premium AI-related bookings grew nearly 60% year-on-year in Q1, while offerings such as Agentforce and Flex Credits are gaining traction across large enterprise customers.

At the same time, legacy headwinds persist. Weakness in Tableau, Commerce Cloud and Marketing Cloud continues to weigh on bookings and renewals, highlighting an uneven transition as AI reshapes enterprise software spending priorities.

Encouragingly, management noted that AI workloads are not materially pressuring gross margins, suggesting that incremental demand is being absorbed efficiently within existing infrastructure. Slack is also emerging as a key interface for agentic workflows, reinforcing Salesforce’s platform strategy.

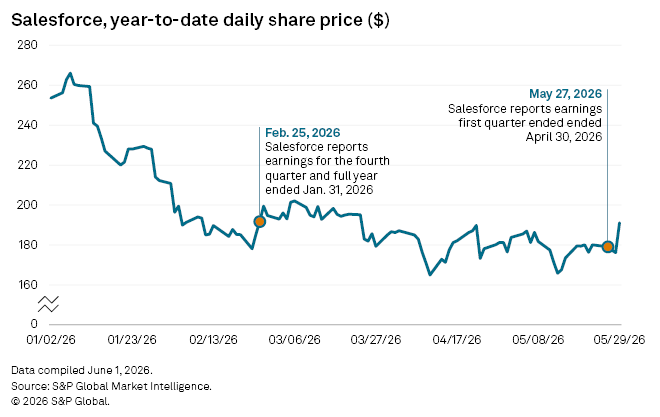

Share price reaction

Shares saw a muted to negative reaction post-results, as strong earnings beat and improving AI monetization trends were offset by investor concerns around AI-driven disruption and slowing growth across parts of the traditional SaaS business.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment