Research — June 3, 2026

Nebius surges on AI demand as revenues set to multiply

By Sourav Kataria

Nebius Group NV (NASDAQ: NBIS) has started the year with rapid growth, highlighting strong demand for AI infrastructure. The company reported strong Q1 earnings with revenues of $399 million, up from $51 million in Q1 2025, as the company benefits from the rapid build-out of AI capacity. The stock has rallied sharply in tandem with the broader AI trade, with Nebius shares up more than 190% year-to-date.

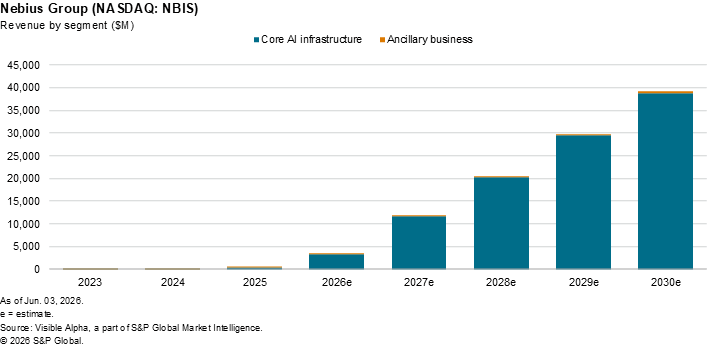

Analysts expect this momentum to continue. Visible Alpha estimates show revenues climbing 589% year-on-year to $3.4 billion in 2026, driven almost entirely by its core AI infrastructure unit, where sales are expected to reach $3.3 billion.

The projected revenue ramp is primarily driven by three key factors. First, Nebius has secured more than $45 billion in long-term AI cloud agreements, including a headline five-year deal with Meta Platforms worth up to $27 billion, alongside commitments from Microsoft.

Second, the group is racing to expand capacity to meet this demand. It has lifted its contracted power target to more than 4 gigawatts by the end of 2026, supported by large-scale “AI factory” campuses under development in Missouri and Pennsylvania.

Finally, with an industry-wide shortage of dedicated AI data centers, Nebius operates in a highly advantageous demand-surplus environment. This allows the company to lock in long-term commitments and customer prepayments.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment