Research — June 30, 2026

Micron postQ: AI-driven demand and pricing strength drive record results

By Ehteesham Ansari and Kanika Garg

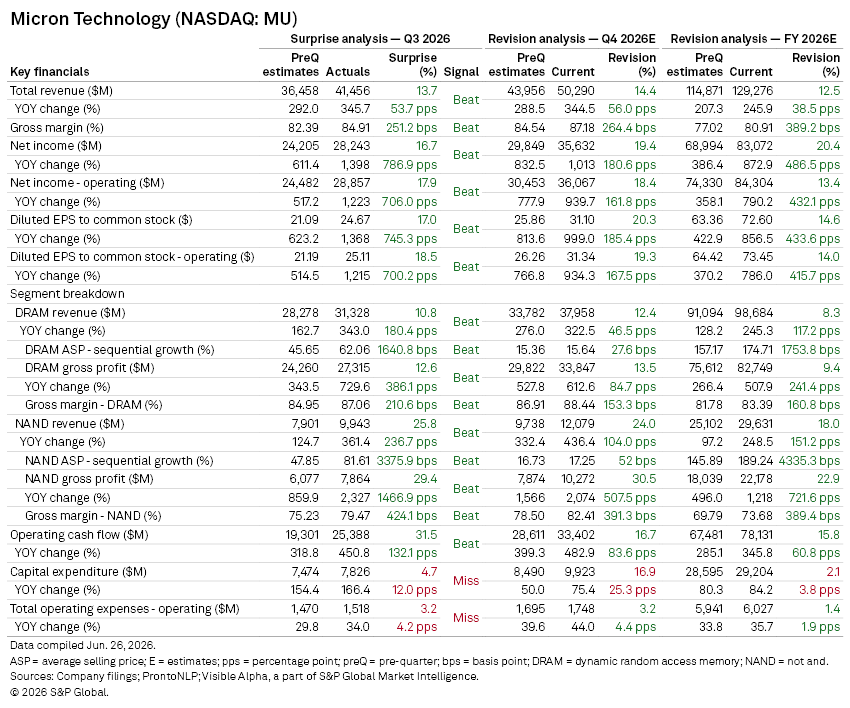

Micron Technology Inc. (NASDAQ: MU) delivered strong fiscal Q3 performance, materially ahead of Visible Alpha consensus expectations, driven by the accelerating impact of AI-driven memory demand and tightening supply conditions across DRAM and NAND markets. Results comfortably exceeded pre-quarter consensus expectations, with both top-line and profitability metrics reaching record levels.

According to earnings summaries compiled using S&P Global’s Pronto NLP alongside Visible Alpha consensus data, Micron’s quarter was defined by exceptional pricing strength, rapid adoption of high-bandwidth memory (HBM), and significant operating leverage across its core product segments.

Key takeaways

Q3 revenues surged to $41.5 billion, up 346% year-on-year and 13.7% above consensus. GAAP EPS of $24.67 and non-GAAP EPS of $25.11 exceeded expectations by 17% and 18.5%, respectively, reflecting both stronger-than-expected demand and a sharply improved pricing environment across memory categories.

DRAM remained the primary growth engine, with revenue rising 343% year-on-year to $31.3 billion, beating consensus by 10.8%. Sequential ASP gains in the low-60% range materially outpaced expectations, highlighting sustained pricing momentum in a supply-constrained environment.

Profitability in DRAM expanded sharply, with gross profit increasing 729% year-on-year to $27.3 billion. The outperformance was driven by a richer mix skewed toward HBM and advanced DRAM nodes, alongside improving contractual pricing dynamics with hyperscale customers.

NAND also significantly outperformed expectations, with revenue rising 361% year-on-year to $9.9 billion, beating consensus by 25.8%. Sequential ASPs increased around 80%, well ahead of expectations, reflecting a pronounced recovery in flash pricing.

Gross profit in NAND rose more than 2,300% year-on-year to $7.9 billion. The segment benefited from both stronger-than-expected demand recovery and improved product mix, particularly in enterprise and AI-related storage applications.

Company-wide gross margin expanded to 84.9%, ahead of consensus by 251bps, while GAAP net income rose 1,398% year-on-year to $28.2 billion. Non-GAAP net income reached $28.9 billion, reflecting the powerful operating leverage from higher memory pricing.

Cash generation remained strong, with operating cash flow increasing 451% year-on-year to $25.4 billion, well above expectations. Capital expenditure rose to $7.8 billion, 4.7% above consensus, as Micron continues to invest aggressively in expanding advanced DRAM, NAND, and HBM capacity to support AI-driven demand growth.

Guidance

For Q4 FY2026 management guided:

- Revenue of approximately $50 billion (±$1 billion), significantly ahead of the $44 billion consensus expected prior to the Q3 earnings.

- Gross margins expected at ~86%, also ahead of estimates

- Capex is projected at ~$10 billion, exceeding preQ expectation of $8.5 billion

- Operating expenses expected at ~$1.65 billion, slightly below consensus

For the full year:

- Capex guidance of ~$27 billion came in modestly below expectations, suggesting a more disciplined pacing of investment even as near-term demand remains robust.

Analyst Q&A highlights: Visibility and long-term contracts in focus

Analyst focus on the earnings call centered on long-term supply agreements and customer commitments. Management clarified that the disclosed $100 billion in agreements represents minimum contractually enforceable revenue, with potential upside above that floor. The associated $22 billion in customer financial commitments includes ~$18 billion in cash deposits and ~$4 billion in letters of credit, with deposits described as unrestricted and tied to take-or-pay structures.

On technology, management highlighted rapid adoption of HBM4 12-high, noting it is ramping at roughly twice the speed of HBM3E 12-high, with cumulative HBM4 revenue already exceeding $1 billion.

More broadly, management reiterated a constructive structural outlook, expecting memory markets to remain supply-constrained beyond 2027, driven by sustained AI infrastructure buildout and the increasing strategic importance of high-performance memory.

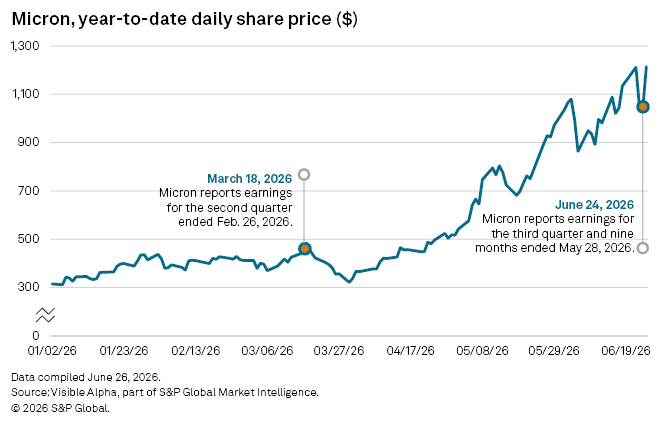

Share price reaction

Shares of Micron rallied following the release, as investors responded to the scale of the earnings beat, strengthening pricing environment, and clearer evidence that AI-driven demand is extending the memory cycle well beyond prior expectations.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Theme

Products & Offerings

Segment