Research — June 15, 2026

Micron: A look at Memory ahead of earnings

By Melissa Otto, CFA

Micron Technology Inc. (NASDAQ: MU) is going to report their FY Q3 earnings on June 24, 2026. Here is a look at the key drivers for Micron’s outlook and the Memory space.

One of the most dramatic market moves around the AI story has been the recent move of Memory stocks. Memory, especially High Bandwidth Memory (HBM), plays an important role in ensuring AI workloads run efficiently and fast, reducing latency. The strength of HBM is that it increases performance by stacking traditional Dynamic Random Access Memory (DRAM) layers vertically, while decreasing the amount of power consumed. As investment in data centers for AI has exploded, demand for memory has become a critical component of AI accelerators, like NVIDIA's Blackwell GB200/B200. As a result of the surge in demand, memory prices have increased significantly, causing upward revisions to the potential earnings growth expectations for the space.

At J.P. Morgan’s 54th Annual Global Technology, Media & Communications Conference on May 20, 2026, Manish Bhatia, EVP, Global Operations for Micron shared his updates on the state of Memory.

- Financial momentum has strengthened materially since the March earnings call. Fiscal Q3 FY2026 guidance stands at approximately $33.5 billion in revenue, 81% gross margin, and more than $19 EPS, with both pricing and volumes tracking ahead of prior expectations.

- Demand continues to outpace supply across HBM, DRAM, and NAND, with industry supply constraints expected to persist well beyond calendar 2026.

Bhatia’s key HBM updates:

- Shipments of HBM4 for NVIDIA's Vera Rubin platform began in March 2026 and are ramping at roughly twice the pace of HBM3E 12-high, with yield improvements ahead of expectations.

- HBM supply remains fully allocated. Micron completed calendar 2026 allocations during Q4 2025, covering both HBM3E and HBM4 products.

- Structural HBM supply constraints continue to intensify. HBM requires more than three times the wafer capacity per bit compared with conventional DRAM, with this ratio increasing across successive generations.

- HBM4E is scheduled to ramp in calendar 2027 on the 1-gamma node. The initial product will follow JEDEC standards, with customized variants expected afterward. Management indicated customers are willing to pay a premium for these customized solutions.

At GTC Taipei 2026 on May 31, 2026, Jensen Huang, CEO for Nvidia shared his updates on Agentic AI and where Memory fits in.

- Agentic AI was the keynote's central theme, with Jensen Huang declaring that "useful AI has arrived" and that "AI is now a profit generator" and "AI is now a GDP generator." He argued that AI agents capable of reasoning, planning, memory management and tool use represent a new computing paradigm that is driving a surge in demand for AI infrastructure and compute capacity. Huang repeatedly emphasized that "compute is revenue" and that every token generated by AI models is now a monetizable unit of output.

- NVIDIA unveiled Vera CPU, a processor designed specifically for agentic AI workloads. Huang positioned the product as a major future growth driver, highlighting its focus on low latency, high single-thread performance, memory bandwidth and energy efficiency for agent orchestration, tool usage, databases and AI memory systems. He also suggested Vera could become one of the most successful product launches in NVIDIA's history.

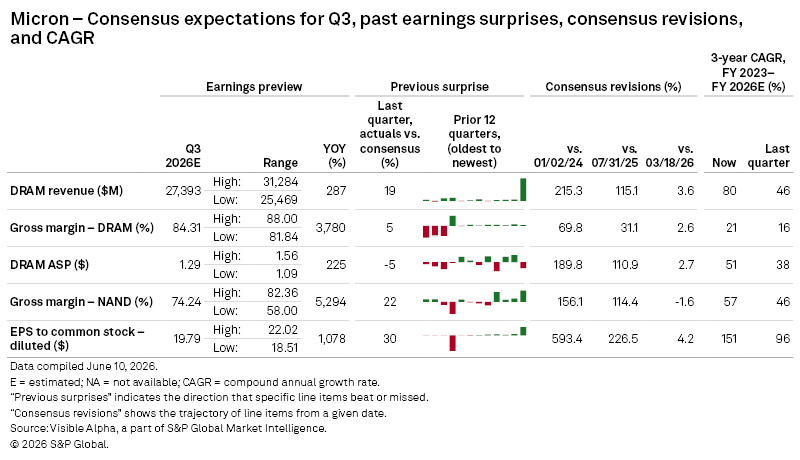

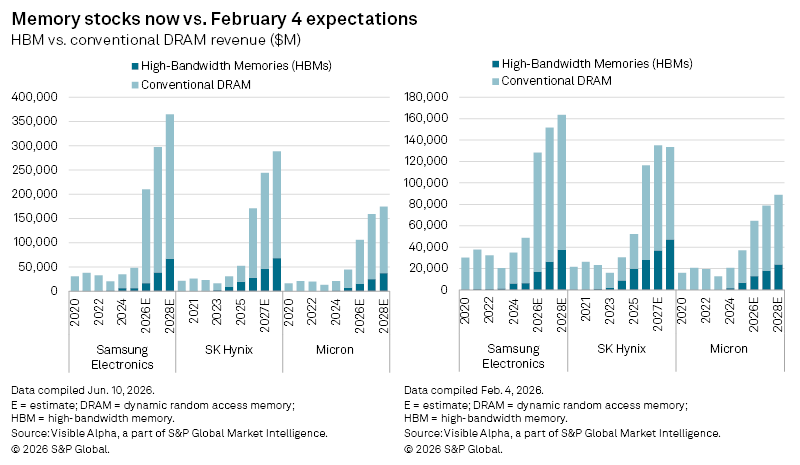

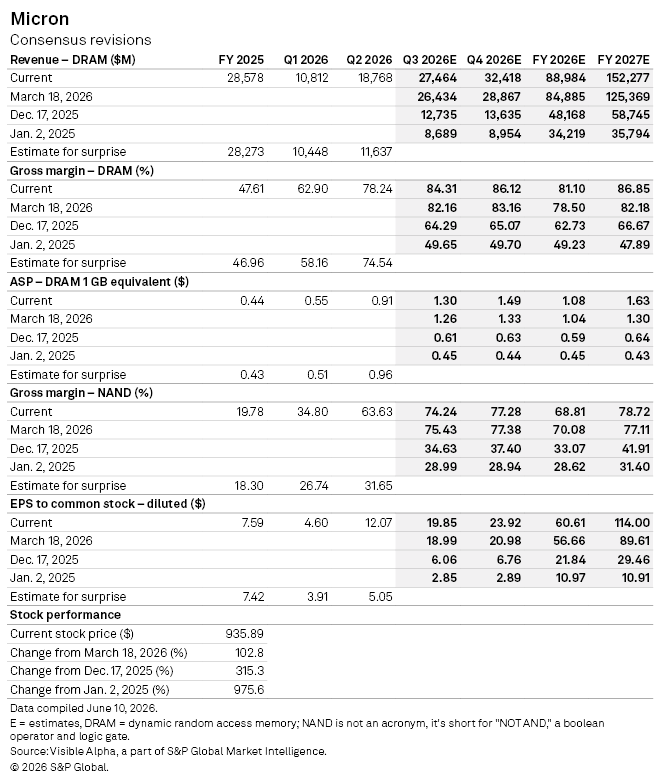

Micron’s quarterly estimates for both DRAM and NAND memory sales and gross profit have increased substantially since last quarter, more than tripling since last year. Consenus projects $27.4 billion this quarter. More importantly, DRAM estimates are expected to generate $32.3 billion next quarter, up 12% since March. Micron’s guidance this quarter will be a potentially important signal to the markets about the trajectory for Memory.

Micron’s DRAM revenues continue to grind higher for FY 2026 and FY 2027. Gross profit consensus for DRAM has jumped 300bps this year and 500bps for next year, capturing the higher prices and driving FY 2027 EPS to now $112/share, up sharply from $90/share in March or a P/E of 8.3x.

The pace of these upward revisions feels reminiscent of the massive upward revisions we observed in 2023 for Nvidia’s Data Center revenue forecasts for 2024 and 2025. These estimates kept going higher on the back of extraordinary demand by the hyperscalers. With the hyperscalers continuing to increase their CapEx guidance, will Memory demand and prices exceed expectations?

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment