Research — June 3, 2026

Dell postQ: AI infrastructure demand drives outsized beat and guidance reset

By Ria Shrivastava

Dell Technologies Inc. (NYSE: DELL) delivered a decisive beat in Q1 FY2027, driven by accelerating demand for AI-optimized infrastructure and continued strength in traditional server markets. Management raised both quarterly and full-year guidance, pointing to record AI server orders, a rapidly expanding backlog, and sustained enterprise and hyperscaler spending despite ongoing component constraints.

Looking at earnings summaries compiled by S&P Global Pronto NLP, along with Visible Alpha pre-quarter consensus expectations and revised outlook, here are some key takeaways.

Key takeaways

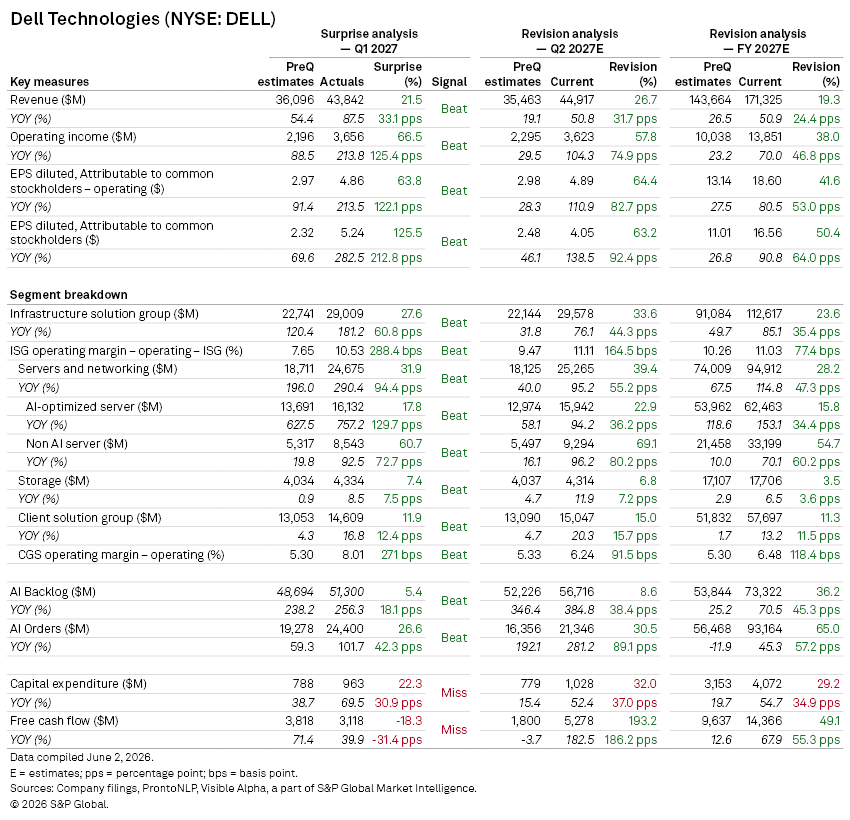

Q1 revenue rose to $43.8 billion, exceeding Visible Alpha consensus expectations by 21.5%, while non-GAAP diluted EPS of $4.86 beat by 63.8%. Operating income reached $3.7 billion, 66.5% ahead of consensus expectations, reflecting meaningful operating leverage as high-value AI systems scale.

The Infrastructure Solutions Group (ISG) was the primary growth engine. ISG revenue surged 181% year-on-year to $29 billion, beating expectations by 27.6%, driven by strong enterprise and hyperscaler investment in AI infrastructure. Within this, servers and networking revenue climbed 290% to $24.7 billion, as data center buildouts and AI cluster deployments accelerated.

AI-optimized servers continued to dominate performance, with revenue rising 757% year-on-year to $16.1 billion, ahead of the $13.7 billion that consensus expected. AI orders reached $24.3 billion, while backlog expanded to $51.3 billion, highlighting strong forward visibility.

Importantly, growth extended beyond AI-specific workloads. Non-AI server revenue rose 92% to $8.5 billion vs. consensus expectations of $5.3 billion.

Storage revenue grew 8% to $4.3 billion, modestly ahead of expectations, supported by demand for data management solutions underpinning AI deployments.

The Client Solutions Group (CSG) delivered revenue of $14.6 billion, up 17% year-on-year and ahead of consensus by 11.9%. Strength was driven by resilient commercial PC demand and early signs of an enterprise refresh cycle.

Margins expanded across both segments. ISG operating margin reached 10.5%, while CSG margin came in at 8.0%, both ahead of expectations. The improvement reflects a richer mix of AI systems, pricing discipline, and operational efficiency gains.

Free cash flow increased 39.9% to $3.1 billion but fell short of expectations, as capital expenditure rose 70% year-on-year to $963 million, 22.3% above expectations, as Dell continued to expand capacity and infrastructure to support sustained AI-driven demand.

Guidance

For Q2 FY2027, Dell guided to:

- Revenue: $44–$45 billion, ahead of preQ consensus of $35 billion

- Adjusted EPS: $4.80 ± $0.10, also materially ahead of prior expectations

- ISG revenue: Expected to grow roughly 75%, supported by ~$15.5 billion in AI server revenue

- CSG revenue: Projected to grow around 20%.

For the full year:

- Revenue: Guidance raised to $165–$169 billion, ahead of preQ consensus of $144 billion

- Adjusted EPS: $17.90 ± $0.25, above consensus expectations of $13.14

- ISG revenue: Expected to grow ~80%, driven by ~$60 billion in AI server revenue (~2.4x year-on-year)

- Traditional servers and CSG are also expected to deliver solid growth.

- Operating income is projected to grow more than 55%, with operating expenses rising at a high-single-digit pace.

Analyst Q&A highlights

Management highlighted a combination of demand pull-forward and structural refresh cycles, driven by ageing infrastructure, Windows 11 upgrades, and AI adoption.

Traditional server growth remains volume-led, with expanding pipelines tied to enterprise modernization and emerging agentic AI workloads. Demand is also being supported by Tier 2 cloud providers.

Supply constraints, particularly in memory, processors, and storage, are expected to persist into the second half, though management remains confident in securing incremental supply.

Architecturally, Dell is seeing increased adoption of ARM-based AI deployments in large-scale liquid-cooled systems, while maintaining a balanced approach across x86 and ARM platforms.

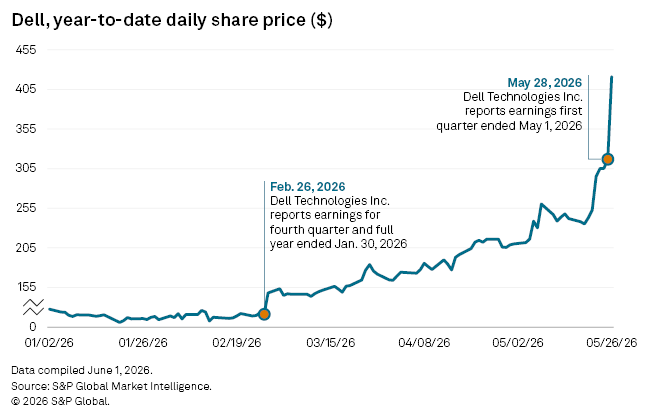

Share price reaction

Shares rallied post-results, supported by the scale of the earnings beat, a sharp uplift in guidance, and growing confidence in the durability of the AI infrastructure cycle.

This article was published by Visible Alpha, part of S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Content Type

Products & Offerings

Segment