ECONOMICS COMMENTARY — 10 Jun, 2026

Consumer service providers suffer sharpest hit of all business sectors since outbreak of war

Providers of consumer services such as tourism and recreation have so far reported the sharpest hit to their business activity levels since the outbreak of war in the Middle East, according to detailed sector PMI data from S&P Global, with financial services providers also taking an above-average hit. Manufacturers have been benefitting from stock piling, but this is likely to only provide a temporary support to growth.

Global PMI signals diverging sector trends

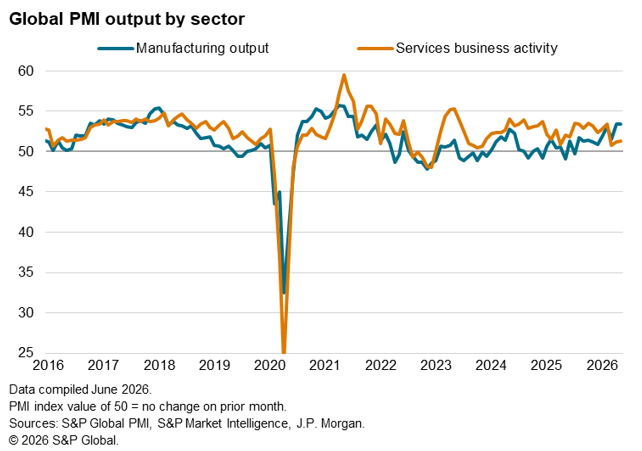

While overall business growth held steady worldwide in May, a marked divergence has opened up since the outbreak of the war in the Middle East. On one hand the global economy has been buoyed by strong manufacturing growth in recent months, but on the other it has been subdued by weakness in the services economy, according to PMI survey data from S&P Global, compiled on behalf of J.P. Morgan.

Worldwide services growth remained among the weakest seen over the past two years in May, but manufacturing output growth accelerated to the fastest since July 2021, outperforming the services economy for the third month in a row. Such faster manufacturing growth relative to services is unusual by recent standards.

Manufacturing performances beat services in all major economies bar India, mainland China and Brazil, albeit in some cases merely representing slower rates of decline.

Both sectors reported cooling demand amid rising price pressures and squeezed spending among customers, and also reported that heightened geopolitical uncertainty again dented growth.

However, the manufacturing sector reported a further boost from precautionary stock-building in May, which has been evident since the outbreak of the war, with factories and customers bringing forward purchases due to concerns over supply availability and price hikes.

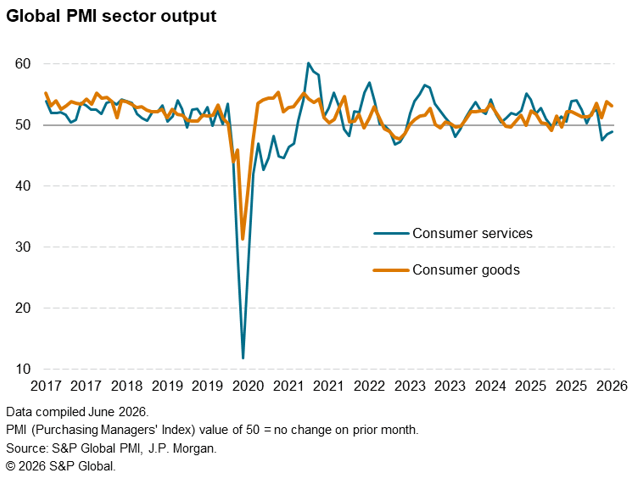

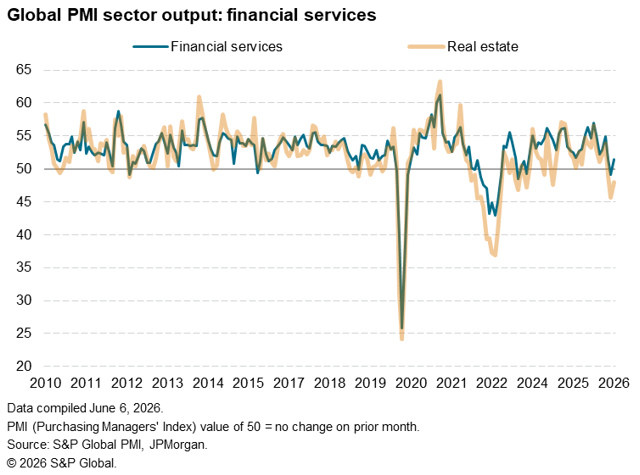

Consumer services and real estate report hardest hits from war impact

Drilling down further into industrial trends, consumer services were again the hardest hit from the war globally in May, having seen the sharpest downturn since 2022 over the past three months. In marked contrast, consumer goods producers have enjoyed some of the strongest gains since 2024 in recent months, underscoring how stock building has led to a divergence in sectoral trends.

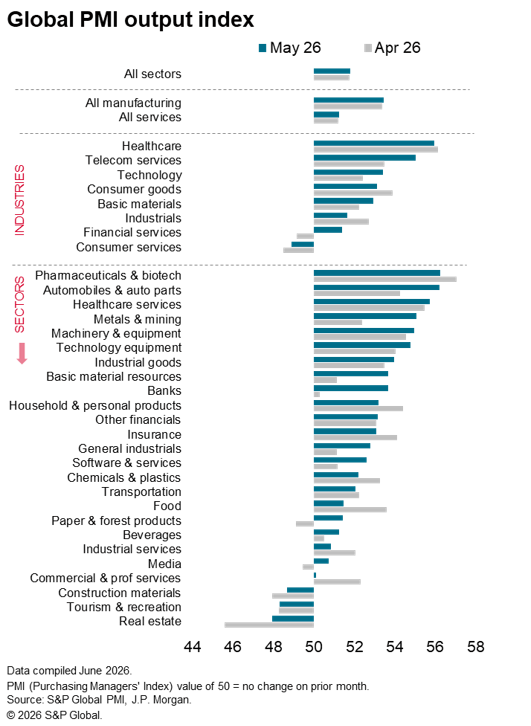

Financial service providers have meanwhile again reported an especially weak performance in May, linked in part to the impact of higher interest rates. By contrast, healthcare has enjoyed a surge in activity.

Best performing sub-sectors have been pharma and autos, with metals & mining, machinery & equipment and tech equipment also all doing well but buoyed by stock building.

Worst performing has been real estate followed by tourism & recreation and construction materials, the latter hinting at reduced building investment.

Supply scarcities to guide outlook

May’s survey data therefore indicates how sluggish or falling demand for services in many economies, often linked to squeezed spending power amid high prices, contrasts with a general upturn in demand for manufactured goods.

However, it’s clear from the evidence provided by survey contributors that precautionary stock building due to concerns over rising prices and supply scarcities, linked to the war, has continued into May. This provides a temporary boost to the performance of the goods-producing sector, which is likely to unwind in coming months as stock building is either completed or supply availability acts as an increased constraint. April and May data have already shown supply constraints acting as a dampener on growth in some economies.

The development of these scarcities will play a key role in future growth of the global economy and will of course in turn depend on the duration of the conflict in the Middle east and related shipping disruptions. In the meantime, we suggest that the services economy provides a more accurate insight into the underlying health of the global economy, as such stock building is not blurring the demand picture for these industries.

© 2026, S&P Global. All rights reserved. Reproduction in whole or in part without permission is prohibited.

Purchasing Managers' Index™ (PMI®) data are compiled by S&P Global for more than 40 economies worldwide. The monthly data are derived from surveys of senior executives at private sector companies, and are available only via subscription. The PMI dataset features a headline number, which indicates the overall health of an economy, and sub-indices, which provide insights into other key economic drivers such as GDP, inflation, exports, capacity utilization, employment and inventories. The PMI data are used by financial and corporate professionals to better understand where economies and markets are headed, and to uncover opportunities.

Read our latest PMI commentary here.

This article was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global.

Theme

Location

Products & Offerings